wavemovies

Investment Thesis

Wix.com Ltd. (NASDAQ:WIX) delivered yet another set of results that support the bull case for its stock. Wix reiterates its goals to reach more than the Rule of 40 in 2025. Meanwhile, for 2024, Wix guides for approximately 14% CAGR on the topline.

According to my estimates, this business, with a strong balance sheet with more than $400 million of net cash, is likely to be printing approximately $570 million of free cash flow in 2025.

As far as tech businesses go, paying approximately 13x next year’s free cash flows strikes me as a compelling entry point.

Rapid Recap,

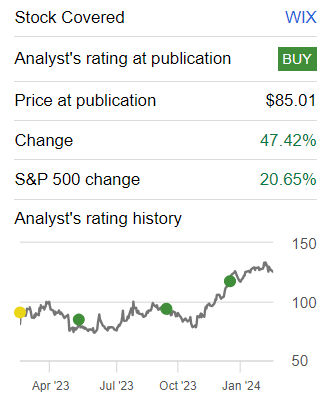

In my previous bullish analysis, back in December, I said,

Author’s work on WIX Author’s work on WIX

As you can see above, I’ve been bullish on Wix for some time, with the stock nicely outperforming the S&P 500 (SP500) in the same period. Furthermore, as we look ahead, I continue to reaffirm that this is a compelling stock.

Wix’s Near-Term Prospects

Wix helps people and businesses create their own websites. It provides easy-to-use tools and templates, allowing users to design and customize their websites without needing advanced technical skills. Wix offers a range of features, including drag-and-drop design, the ability to add apps and plugins, and options for online commerce. Essentially, it’s a user-friendly way for anyone to build and manage their own website, whether it’s for personal use, a blog, or an online business.

Wix’s near-term prospects are marked by meaningful product development and strategic initiatives to empower its users. Wix has incorporated GenAI models and capabilities, enabling all Wix employees to contribute seamlessly to the development of AI-driven features. Its focus on efficiency allows Wix to deliver high-quality tools more rapidly. The introduction of a GenAI-based platform dedicated to conversational assistance further highlights Wix’s strive for innovation.

Moreover, Wix is actively maximizing partner success through a refreshed revenue share program. Just launched last month, this program is part of the Wix Partner Program, emphasizing engagement with professionals and agencies. The updates offer eligible partners an increased revenue share on new Studio premium sites created in 2024, with Legends, its highest-tier partners, enjoying more benefits.

The expanded program encompasses revenue share on additional non-website package products, reinforcing Wix’s dedication to cultivating mutual growth opportunities within its ecosystem.

Also, its partnership with Global-E enhances Wix’s near-term outlook by expanding commerce capabilities. This collaboration empowers Wix merchants to target global markets with advanced cross-border e-commerce solutions, localized checkout, and streamlined international logistics.

Given this context, let’s now turn to discuss Wix’s fundamentals.

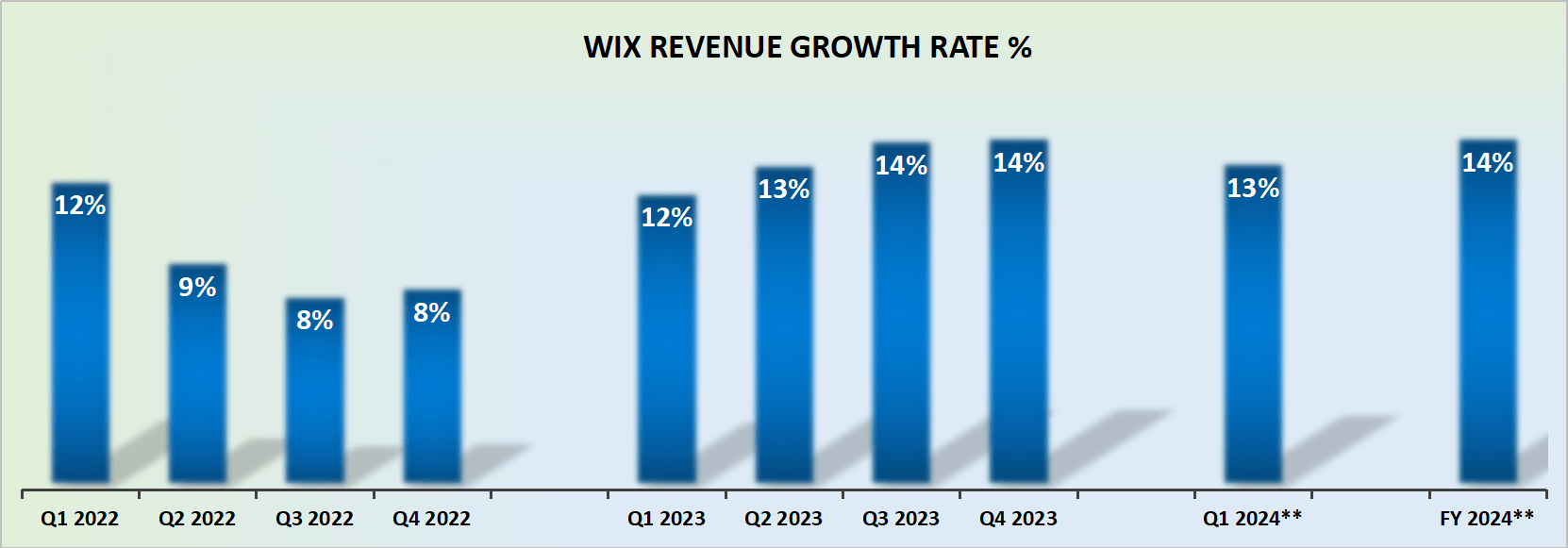

2024 Outlook Points to 14% CAGR

WIX revenue growth rates

Wix guides for 13% revenue growth rates for 2024 at the high end of its range. Accordingly, given that we are still early in 2024, together with management inevitably being prudent with its guidance, I believe that a 14% CAGR appears reasonable.

This is ever-so-slightly higher than what analysts were expecting, in any case. But given that Wix had already delivered resounding revenue growth in 2023, it only makes sense that its growth rates for 2024 are pointing towards the mid-teens.

That being said, that’s not where the bull case for Wix is found. That’s what we discuss next.

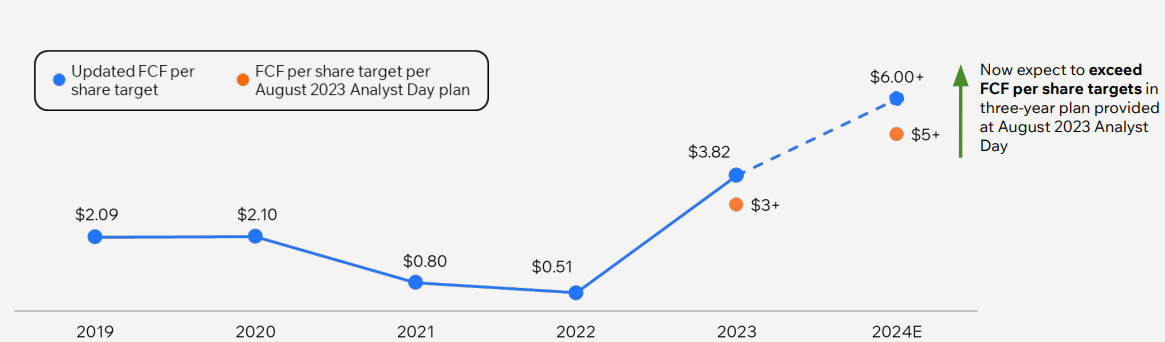

Wix Stock Valuation — 13x 2025 Free Cash Flows

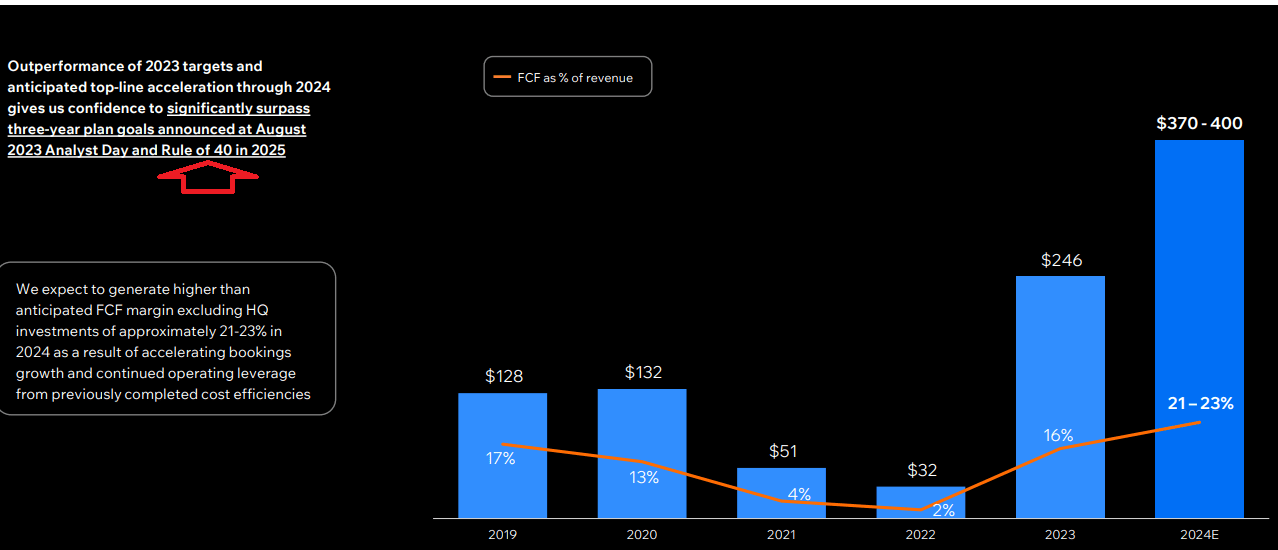

Wix ended 2023 with $246 million of free cash flow, while its guidance for 2024 points to approximately $400 million, a 62% jump in free cash flows this year.

What’s more, looking slightly further ahead to 2025, Wix reiterates the message that we’ve all become accustomed to seeing, that Wix’s will ”significantly surpass the Rule of 40 in 2025.’.

WIX Q4 2023

Given that Wix’s underlying free cash flow margins are expected to expand by approximately 700 basis points in the twelve-month period from 2023 to 2024, it only appears logical that there’s still more room for the company to expand by a further 300 to 400 basis points in fiscal 2025.

Therefore, I believe that looking out to fiscal 2025, Wix could see about $580 million of free cash flow. This puts Wix priced at 13x its 2025 free cash flows.

Furthermore, given that Wix’s balance sheet holds about $430 million of net cash, and the business is evidently producing significant free cash flows, this has allowed Wix to be aggressive in repurchasing its shares.

WIX Q4 2023

Indeed, one negative consideration that often surfaces about Wix is that it has too much stock-based compensation for its employees. However, at some point in 2024, Wix will reach clean GAAP profitability. Therefore, the business at that juncture will be self-sufficient. In sum, there’s a lot to like about Wix.

The Bottom Line

In conclusion, Wix’s recent performance and outlook present a compelling case. The company’s near-term prospects showcase a commitment to innovation.

Looking ahead, the 2024 outlook suggests a robust 14% CAGR in revenue growth rates, demonstrating Wix’s continued momentum. The stock’s valuation at 13 times its projected 2025 free cash flows appears reasonable, especially considering the company’s strong balance sheet with over $400 million in cash. While concerns about stock-based compensation have been raised, the anticipation of reaching clean GAAP profitability in 2024 reinforces the potential self-sufficiency of the business.

All in all, Wix.com Ltd. presents a compelling investment opportunity, supported by its solid financials, and optimistic growth trajectory.