VanderWolf-Images

Introduction

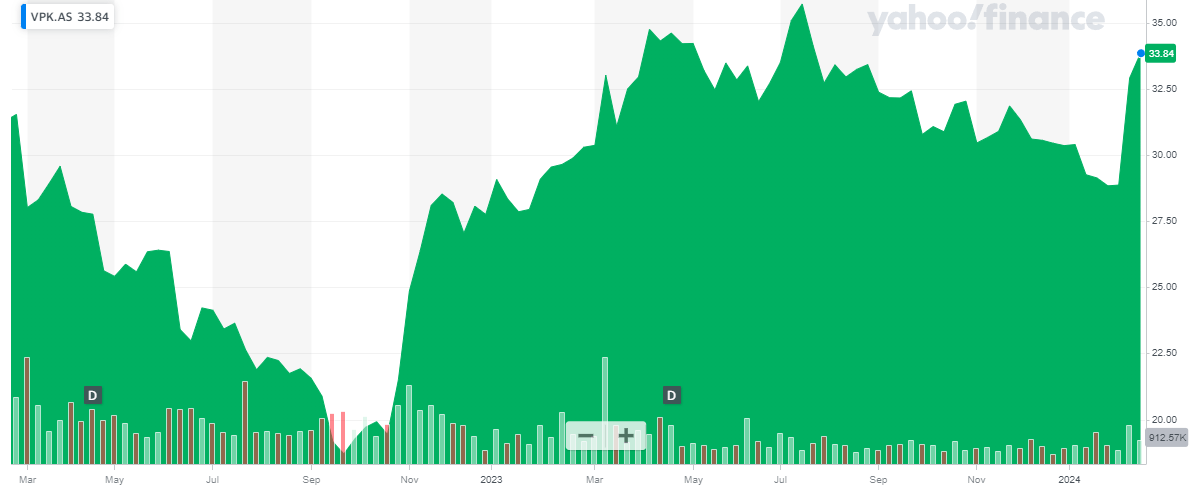

I have been tracking Vopak (OTCPK:VOPKF) for several years now and in the summer of 2022 I thought the company had become too cheap and I liked the stock for its 5.5% dividend yield, which was pretty good for an infrastructure company back in the day. Since that article in August 2022, the share price has increased by approximately 50% while the company has also paid out a 1.30 EUR dividend.

Yahoo Finance

Vopak is a Dutch company and its listing on Euronext Amsterdam is a better option than its US listing. The ticker symbol in Amsterdam is VPK, and with an average daily volume of approximately 160,000 shares, the Amsterdam listing clearly is the most liquid. As Vopak also reports its financial results in Euro, I will use the EUR as base currency throughout this article, unless indicated otherwise. The company currently has 125.1M shares outstanding.

This article is meant as a follow-up article on Vopak. For a better understanding of the company’s business model and plans, I’d like to refer you to my older articles.

It’s all about the cash flow – and Vopak posted a strong result in 2023

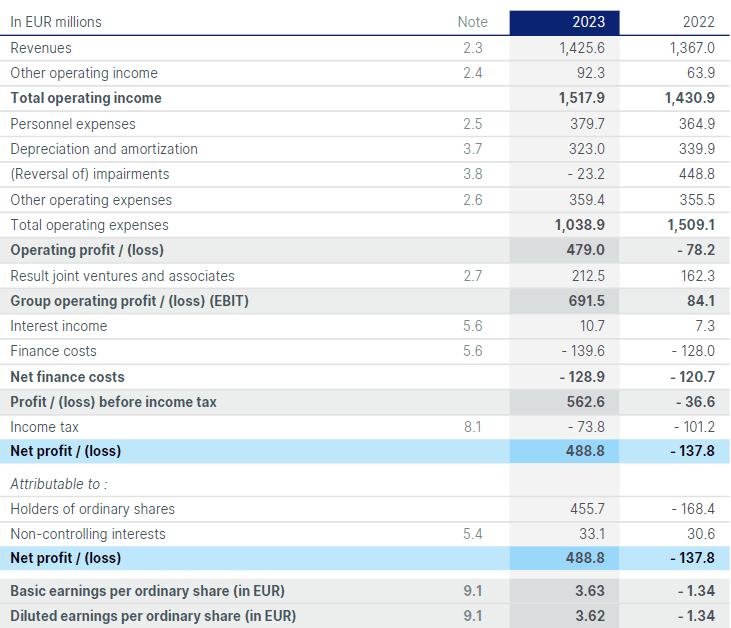

2023 definitely didn’t disappoint. The company reported a total revenue of 1.43B EUR and a 92M EUR “other” operating income which was related to the management fees of a joint venture and the gain on the sale of assets resulting in a total operating income/revenue of 1.52B EUR. The operating profit was approximately 479M EUR which is substantially better than the operating loss of 78M EUR in 2022, but keep in mind the 2022 result was negatively impacted by a 449M EUR impairment charge while Vopak was able to report a net impairment reversal of 23M EUR in 2023.

Vopak Investor Relations

Additionally, the result of the company’s joint venture and investments increased sharply, resulting in a reported EBIT of 692M EUR. Quite a bit higher than the 84M EUR in 2022. But if we would exclude the impairment charges, the adjusted EBIT in 2023 would have been approximately 668M EUR vs. 533M EUR in 2022. So even on an underlying basis, the EBIT showed a very strong improvement. The net income was approximately 489M EUR of which 456M EUR was attributable to the shareholders of Vopak. This resulted in an EPS of 3.63 EUR, a very nice result.

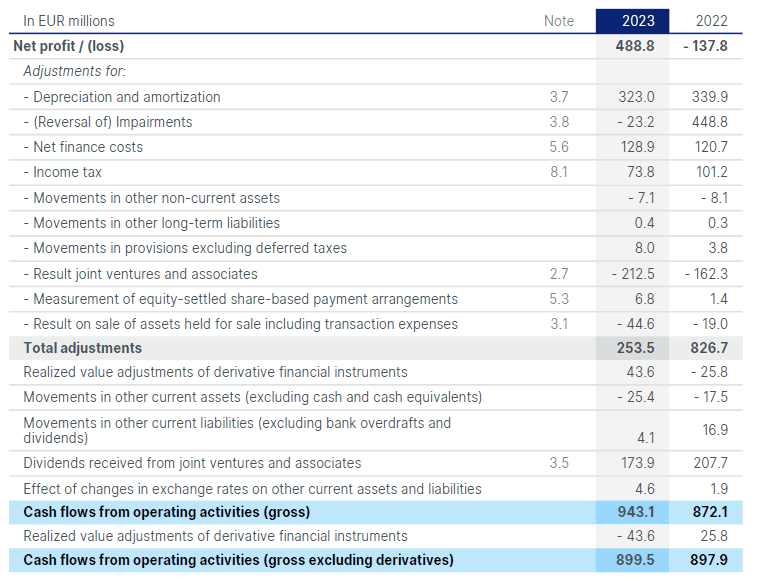

In all my previous articles, I based my investment thesis on the cash flow performance of the company, and I will do the exact same thing now. As you can see below, Vopak reported an operating cash flow of 866M EUR, but the starting point was the 943M EUR “cash flow from operating activities.” The footnote provides more clarity, as the cash flow from operating activities includes the 174M EUR dividend income from the associates and joint ventures. That’s approximately 40M EUR lower than the reported attributable net income.

Vopak Investor Relations

Additionally, the cash flow statement below shows an 85M EUR cash tax payment although Vopak only owed 74M EUR based on the income statement. Additionally, there were some changes in the working capital position, and the taxes and working capital changes pretty much zeroed each other out.

Vopak Investor Relations

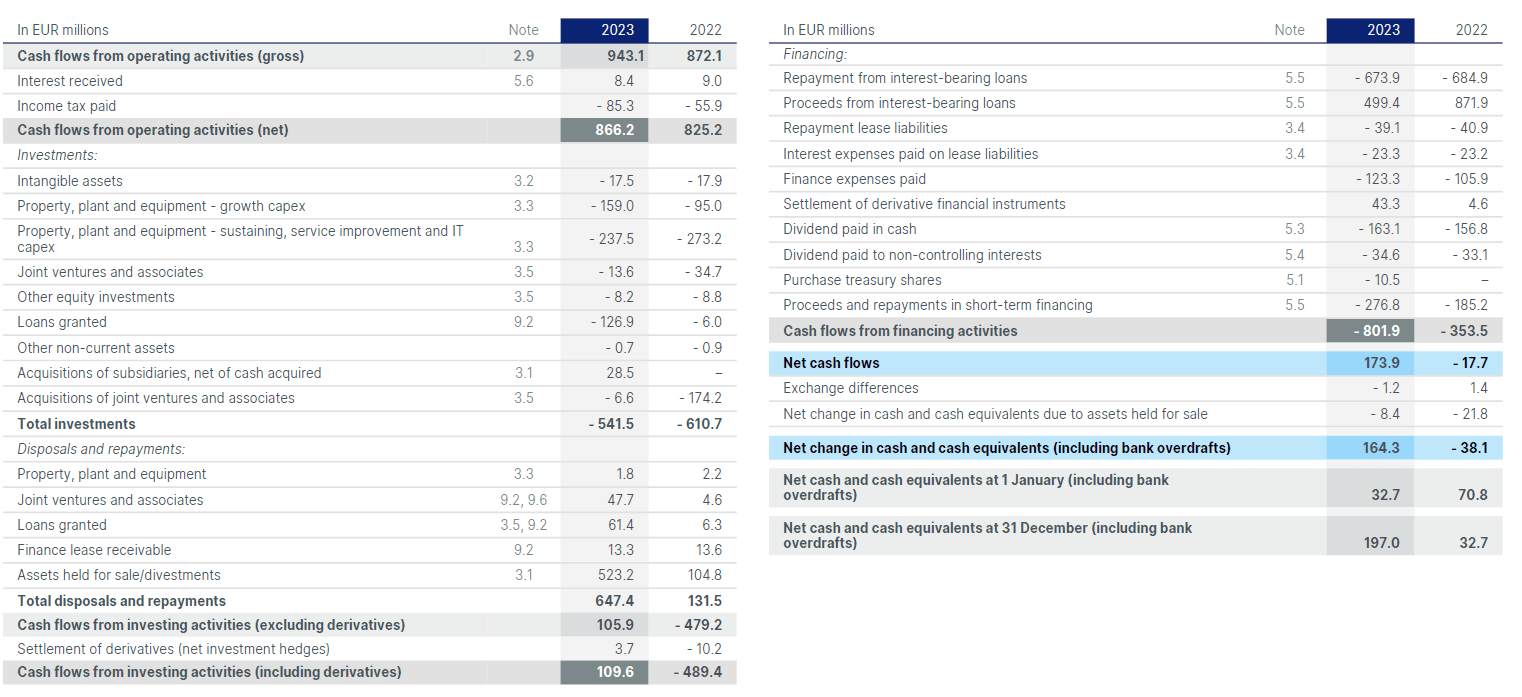

As such, the 866M EUR in operating cash flow above is a fair assessment. That being said, we still have to deduct the 39M EUR in lease payments, the 35M EUR in dividends to non-controlling interests and the 146M EUR in interest payments on leases and financial debt.. This means the underlying operating cash flow was approximately 646M EUR.

The total capex was approximately 414M EUR, but Vopak makes a clear distinction between growth capex and sustaining capex. The sustaining capex was just 237.5M EUR which would result in a net underlying free cash flow of 408.5M EUR.

That’s approximately 47M EUR lower than the attributable net profit, and that difference is almost entirely related to the difference between the net income from joint ventures and associates versus the cash dividends Vopak received from those investees.

Based on the current share count, the net free cash flow was 3.26 EUR per share which means the stock is still trading at a free cash flow yield of approximately 10%. Vopak has declared a dividend of 1.50 EUR per share, which is a 15% increase compared to the 1.30 EUR it paid out based on the 2022 results.

Looking forward to 2024

Vopak also has already released its outlook for 2024. During the current financial year, the company expects its proportional EBITDA to increase by approximately 5%-10% while the consolidated EBITDA will come in slightly higher than the 2023 result.

Vopak Investor Relations

The EBITDA outlook includes the impact of the recent divestments. Vopak also has already provided a capex guidance for this year. It expects to spend another 300M EUR on growth while the sustaining capex will come in approximately 230M EUR.

Vopak Investor Relations

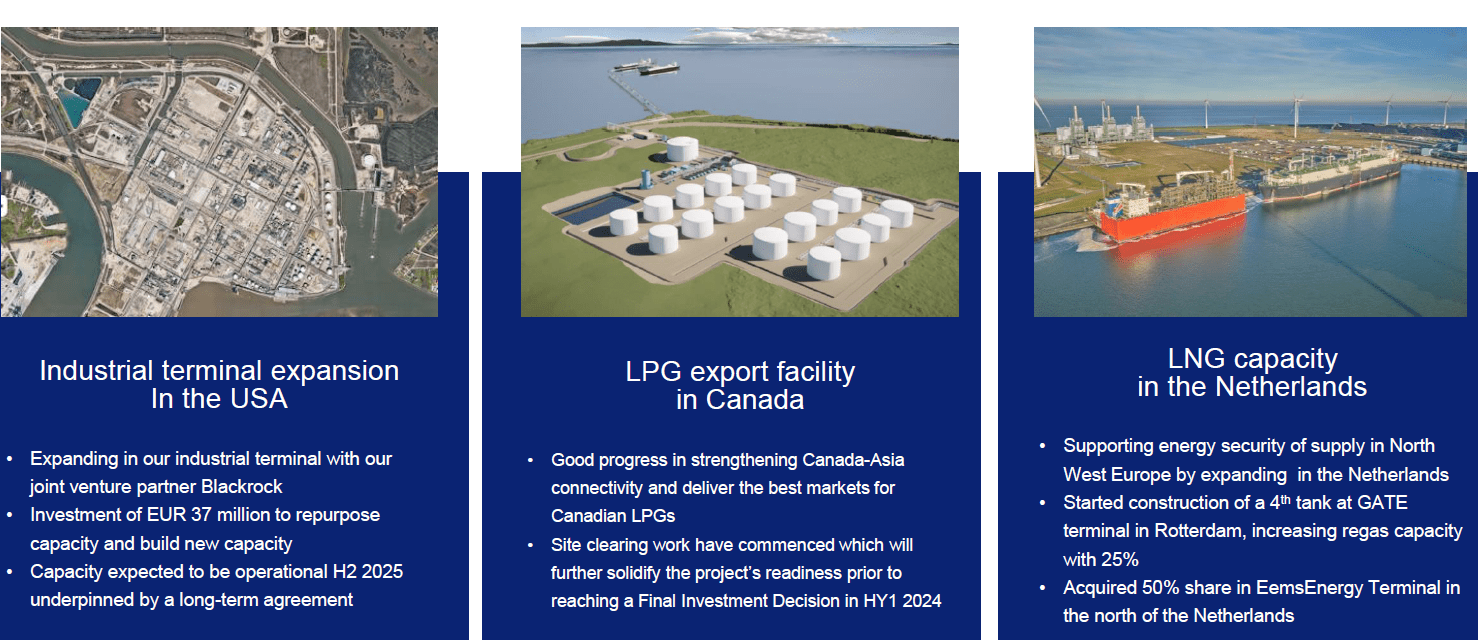

The growth capex is in line with the company’s previously disclosed plans to invest 2B EUR of which 1B EUR will be invested in industrial and gas terminals by 2030 while the other 1B EUR will be invested in new energies and sustainable feedstocks. The terminal plans are ramping up as the company has highlighted three projects it will continue to invest in.

Vopak Investor Relations

Some of the other investments aren’t growth per se, but also include the repurposing of existing assets.

Vopak Investor Relations

The company also has confirmed its plans to continue a progressive dividend policy. Given the current payout ratio which is less than 50% of the 2023 profit, that shouldn’t be a hard task. Vopak also reconfirmed its leverage target of 2.5-3 times EBITDA. As the company ended the year with a debt ratio of just under 2 times the EBITDA, Vopak could actually take on additional debt to fund its expansion programs without too many repercussions. During the Q4 conference call, the Vopak management indicated it expects to end this year with a leverage ratio of 2.3-2.5 times EBITDA.

Investment thesis

I currently have no position in Vopak as I exited all exposure after the 50% share price increase within the first six months after the August 2022 article was published. That being said, I’m pleasantly surprised by the company’s strong results in the third quarter and the small EBITDA increase (on a reported basis) indicates Vopak should be able to keep its EPS above 3.25 EUR per share barring any unforeseen circumstances. While the EBITDA remains strong, I expect the interest expenses to increase as well as Vopak’s net debt will likely increase as part of its expansion program.

I missed the recent dip in January bit seeing how strong Vopak’s results are and considering the company’s performance will remain strong in the foreseeable future, I may be looking to re-initiate a long position in Vopak. Perhaps I will write some (out of the money) put options.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.