Andreus

Investment Thesis

Company Overview

Spire Global, Inc. (NYSE:SPIR), founded in 2012 (changed name to “Spire Global” in 2014) and headquarters in Vienna, Virginia, is a satellite-based aircraft tracking and ship monitoring data provider with insights and predictive analytics for optimal decision-making and cost-effective applications.

Strengths and Weaknesses

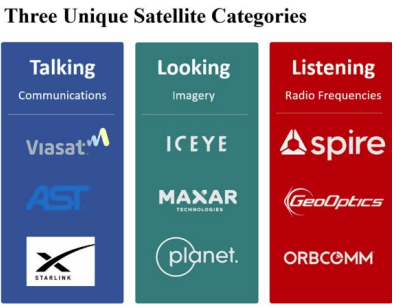

As nascent as the satellite data industry is, there are three refined categories based on their application and specialties. One is for communication, such as StarlinkX, one is for imagery, such as ICEYE, and Spire belongs to the category that focuses on radio frequency surveillance, or listening.

Spire Global: Three Unique Satellite Categories (Company 10K)

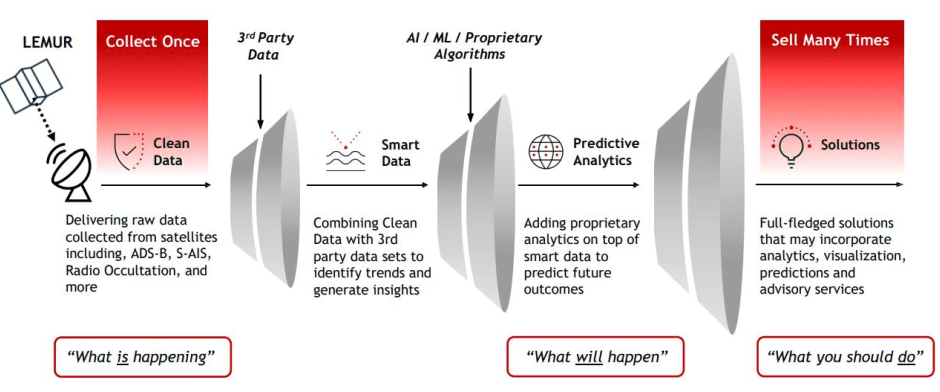

The biggest asset of Spire Global is obviously its satellite constellations in the lower-orbit, called “LEMUR nanosatellites”. But how the company makes them into one of the largest multi-purpose “listening” network is closely relying on the ground station network infrastructure. Its multi-receiver satellites obtain Automatic Identification Systems (“AIS”) data from vessels, Automatic Dependent Surveillance–Broadcast (“ADS– B”) data from aircraft and radio occultation (“RO”) data utilizing Global Navigation Satellite Systems (“GNSS”) satellites. This space-to-earth correspondence covers the earth more than 200 times per day on average, which makes its data effectively real-time or near real-time. The value of a unified view with robustness and multi-functional access points has been integrated with both a SaaS platform and cloud-based data analytics, essentially making its wide range of data many times scalable for sale as clean and predictive data solution to solve specific business problems.

Spire Global: Business Operation Outline (Company 10K)

The largest industries Spire sells to are maritime, aviation, and governments, as directly applicable customers. But it also grows a range of current and target industries such as agriculture, logistics, financial services, insurance, aerospace, energy, fishing, academia, and real estate, etc.

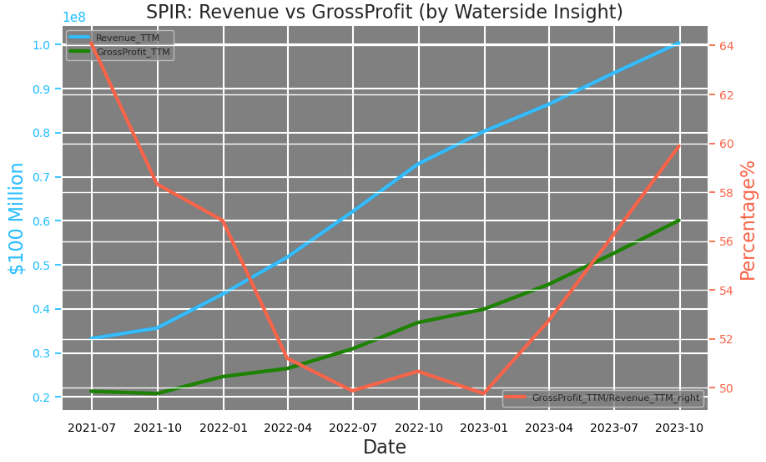

Since its IPO, the company’s revenue has grown from $35 million to now $100 million quarterly, more than 3x of where it was three and a half years ago.

Spire Global: Revenue vs Gross Profit (Calculated and Charted by Waterside Insight with data from company)

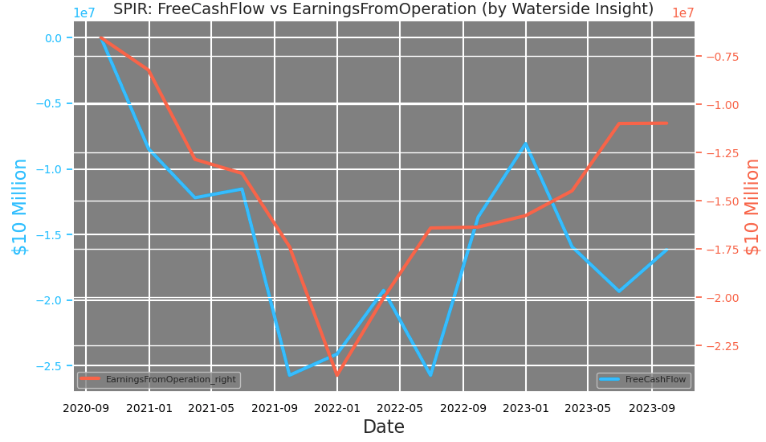

But both its free cash flow and operating earnings are solidly in the negative. They currently both have pulled back up from the lowest in Q3 of ’21, but still trailing the levels where they started with near zero.

Spire Global: Free Cash Flow vs Earnings From Operation (Calculated and Charted by Waterside Insight with data from company)

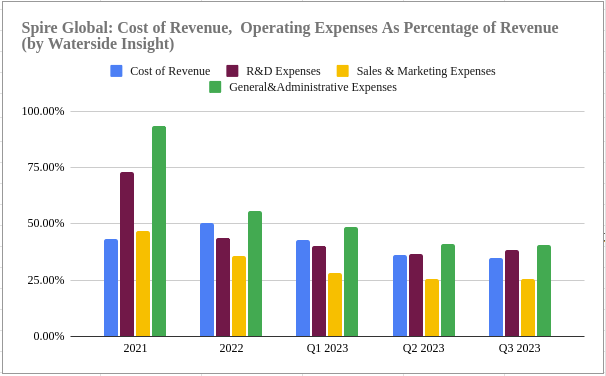

Spire Global expects the year 2024 will be the year to finally start to become profitable, including positive operating cash flow, free cash flow, and positive adjusted EBITDA. These would be an exciting prospect for investors and we want to examine these expectations. The largest factor it needs to overcome to become profitable is the cost and expenses in relation to its revenue. It has a fixed cost structure that needs to be spent on, such as satellite launching and ground station expansion and maintenance. The most significant reduction with respect to revenue growth is the G&A expenses. It went from over 90% in ’21 to 40% in Q3 ’23. S&A expenses came down from 47% to 25%, while R&D expenses went from 73% to 38%. All have been cut down by half. In the meantime, the cost of revenue has only gone from 43% in ’21 to 35% lately. This was going exactly how it stated in its 2022 10K that both the cost of revenue and operating expenses will go up in absolute value, but op. expenses can be expected to decline as a percentage of revenue. A simple extrapolation could show that with revenue growing at nearly 40% a year and operating expenses declining incrementally on top of that, the results are cutting the percentages by half annually. With its net margin at about negative 60% currently, it could cut down to negative 30%. It will need to either grow the top line by at least 80% in one year or pull in additional cuts of expenses more aggressively. We think it would be tough for it to achieve positive profitability and earnings.

Spire Global: Cost of Revenue, Operating Expense (Calculated and Charted by Waterside Insight with data from company)

We think focusing on the scalability of its top-line growth is the better way to achieve positive profits. Spire’s proprietary radio occultation data was able to predict Hurricane Otis‘s intensity better than other models, which missed its rapid intensification and leaving those impacted unprepared. Such data added with its emerging microwave sounders are part of its global weather forecasting models. Weather data is critical for aerospace industry, or vessels, cargo and cruise in shipping in selecting the safest and most fuel-efficient route in its navigation. It was also rewarded a $2.8 million, 12-month contract with NOAA to integrate its wind speed data into studies. With its capacity of predict weather events, such as polar vortex shifts and/or sudden stratospheric warming, with up to 2 week in advance, commodity traders are keen to take advantage of the trading edge it provides. There are also insurance companies, academia and government entities that are interested in digging into not only the real time but the trove of historical data. The cloud data platform and AI integrated advising analytics enable the resale of data at scale without substantially increasing the marginal cost. After building out the critical infrastructure and the modeling capacity with cost of revenue, the scaling is what could bring down the expenses as proportion to improve the margin. And since it is global data, to expand on an international basis is part of equation as well.

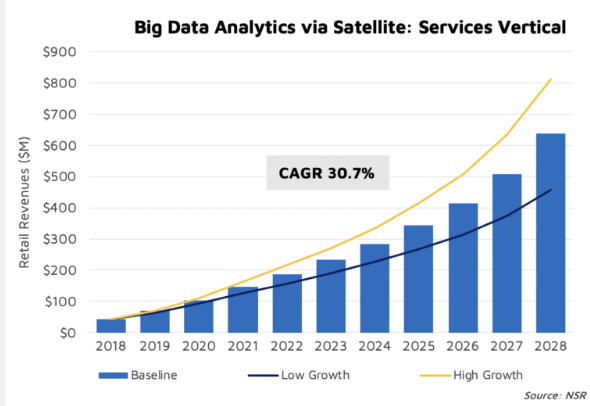

According to NSR, a satellite & space market consulting service provider now part of Analysys Mason, the big data analytics via satellite can see CAGR of as high as 30% through 2028. Many industries are in need of better and more accurate data, the questions are how the customers figure out the usage and how do Spire Global scale to meet the demand accordingly.

Big Data Analytics via Satellite (NSR.com)

Financial Overview & Valuation

Spire Global: Financial Overview (Calculated and Charted by Waterside Insight with data from company)

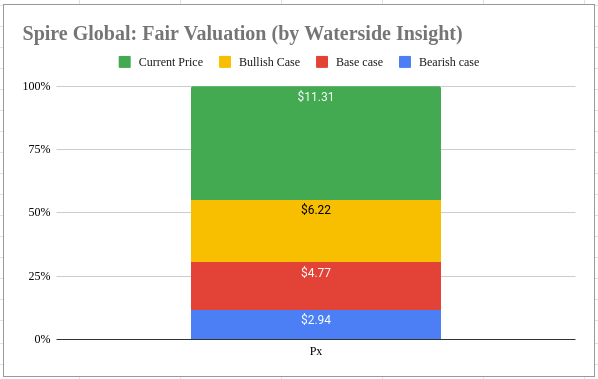

We assess the fair value of Spire Global with our proprietary models. We assumed a cost of equity of 9.12% and a WACC of 12.89%. In our most bullish case, the company was able to barely achieve profitability and free cash flow positive this year, but with faster expansion due to its scale in 5 to 7 years from now; it was valued at $6.22. In our base case though, it was still falling short of becoming earnings and cash flow positive although the gap was substantially shrunk, with faster growth later on, it was valued at $4.77. In the bearish case, its rapid growth comes later than expected due to both the macro environment and customer adaptation, it was priced at $2.94.

Spire Global: Fair Valuation (Calculated and Charted by Waterside Insight with data from company)

The current market value of the stock is overly optimistic about its future cash flow and growth. Spire Global will need to grow its revenue by more than 50% every single year for the next ten years to have the chance to match this valuation. We think such premium is too rich.

For the upcoming earnings release, we expect its EPS to be -$0.50, better than the average of consensus of -$0.57. Revenue is also a beat of $30.02 million compared to $29.19 million estimate.

Conclusion

Spire Global generated a system of proprietary data that is both unique and critically important. But utilizing satellite data is still an emerging application that many industries learning to adopt, although at increasingly rapid pace. We are optimistic on the company’s growth based on the industrial trends and its own margin growth strategy. But the expectation the market priced in is too lofty. We recommend a hold at this point.