dottedhippo

Introduction

Saturn Oil & Gas Inc. (OTCQX:OILSF)(TSX:SOIL:CA) is another example of a Canadian junior oil operator trading at levels significantly below any normal valuation metric. The Canadian market is somewhat bifurcated, with oil mining giants like Canadian Natural Resources (CNQ) fetching EV multiples near 8, and tiny companies like Saturn commanding a small fraction at 2 or 3X EV/EBITDA.

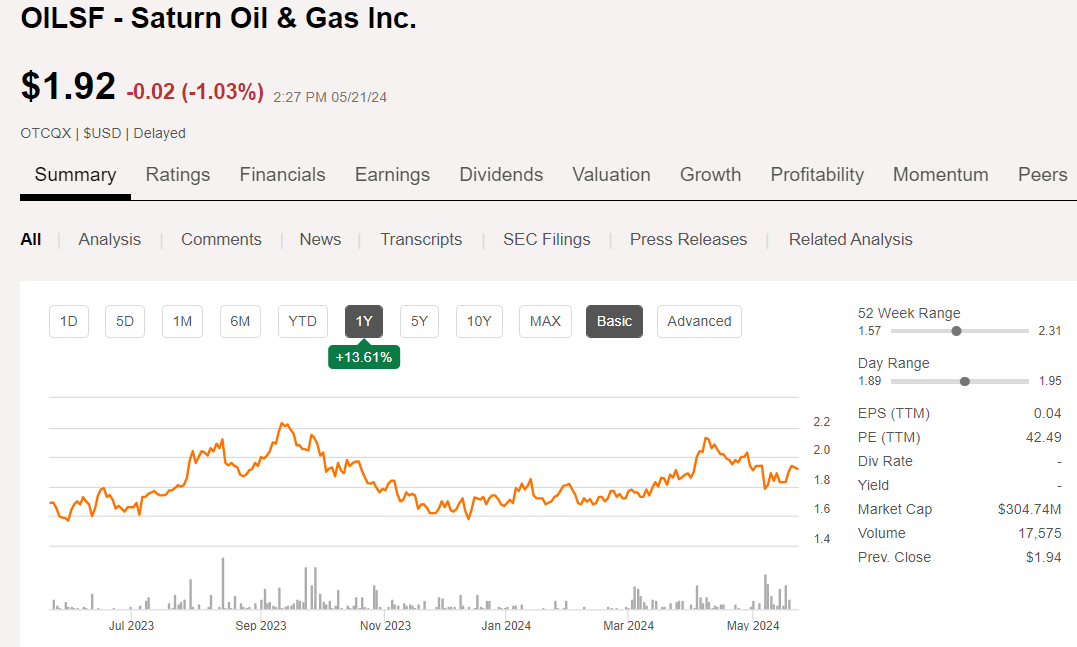

OILSF price chart (Seeking Alpha)

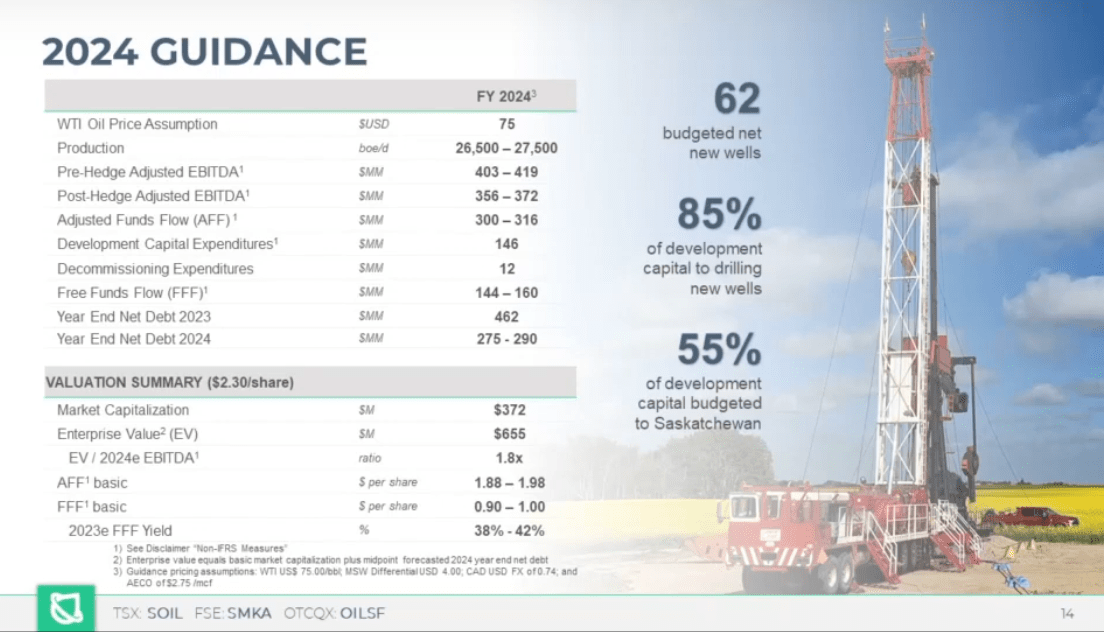

Free cash yield is another metric being glossed over by many investors. In the case of Saturn, investors are looking past this metric. Which is surprising if you take their current free cash per share of $0.18 delivers a 9.5% yield at current prices. Not too shabby, but not exhilarating-this was a down quarter! On TTM basis, this yield ran between 38-42%, as shown in the slide below. Do I have your attention now?

OILSF 2024 guidance (OILSF)

The company is undercovered due to its small size, but is unanimously regarded as a buy by the four (4) analysts covering it. The price targets range from $4.00 to $5.80. The median is $4.47. Any one of those figures represents a substantial upside from its current price. OILSF shanked the first quarter, missing EPS by almost 50% at -0.42. The company noted brutal weather shut-ins and a larger than normal price gap during the quarter for WC-MSB, thanks to some U.S. refinery maintenance and export constraints. The seagulls have raised expectations for Q-2, putting the EPS target at $0.19.

Saturn has been growing through bolt-on acquisitions, taking on debt, and diluting current shareholders with new-issue stock to pay for them. This hasn’t been helpful to shares of Saturn in the short term, but the new assets are transformative for the company and extend its future glide path and bring additive production and additional drilling inventory. That’s likely what the buy side analysts are keying on, as will we.

First, we will take a snapshot of the moving pieces affecting the oil market, the current vicissitudes of which help explain the doldrums oil stocks of all classifications are stuck in at present.

A quick snapshot of the oil market

It’s a bit murky right now, honestly. Competing priorities are holding prices in the mid-to upper $70’s, with occasional forays into the mid-$80’s when things heat up in the Middle East. I have cautioned my readership in the past about getting too worked up about the “war-premium.” It’s based on a notion that there will/may be an attack on tankers, infrastructure or oilfields, that will impact supply or distribution. It hasn’t played out since the First Gulf War. (For you younger folks, that’s when Iraq invaded Kuwait, and left the Kuwaiti oilfields blazing when it was driven out by the U.S. coalition.) The reason probably is that it’s a step too far and would invite a massive retaliatory response. Once fears abate about supply, prices begin a slow deflation awaiting a new buy signal. That’s largely where we are now, at least for U.S. producers.

As I have noted previously, the next waypoints for crude will come from demand-led draws on crude inventory, and or some signs liquids production is beginning a long expected descent from drilling that doesn’t replace legacy production declines. Until then, the doldrums are likely to remain.

Conversely, the Canadian companies have ~600K BOPD of new demand to fill thanks to the TMX pipeline startup. Hence, our interest in Canadian micro-caps.

The thesis for Saturn

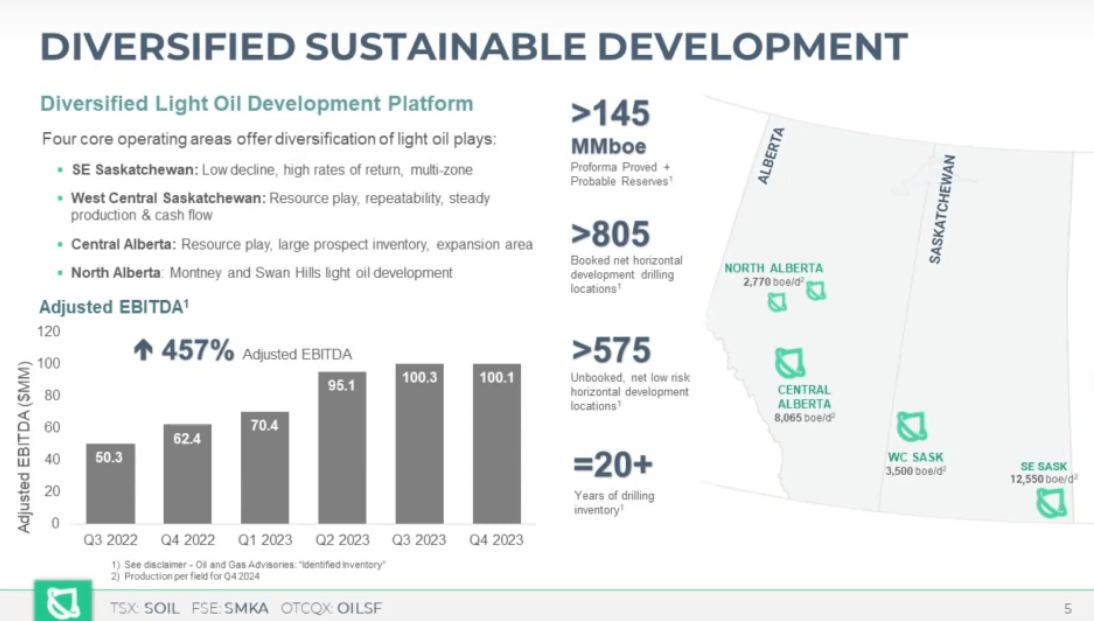

The company divides its efforts between Alberta and Saskatchewan provinces, as the slide below indicates. Most of these assets are low decline, light oil weighted above 85%. In the last year or so, it’s made some significant acquisitions- Ridgeback Energy in 2023, and a Saskatchewan Asset Acquisition just announced in the Q-1 that will bring another 13K BOPD of mostly oil-96%, weighted production with it. The company claims ~20 years of Tier I inventory at projected development rates. Costs have declined 23% from 2021, which yielded solid netbacks in the mid-$40’s in 2023. The company has hedges in place for ~60% of its 2024 production.

The company appears to be heavily discounted in terms of P-2 booked reserves. Conservative loose math then suggests an NPV for Saturn of about $1.1 bn, or $7.24 per share using SA figures. The company is targeting a 2-2024 exit production rate of ~40K BOPD of mostly oil-weighted production. Using less conservative math, the same numbers could arrive at a $10 per share valuation, but when we are having fun with numbers, it’s best to stay conservative.

OILSF Footprint (OILSF)

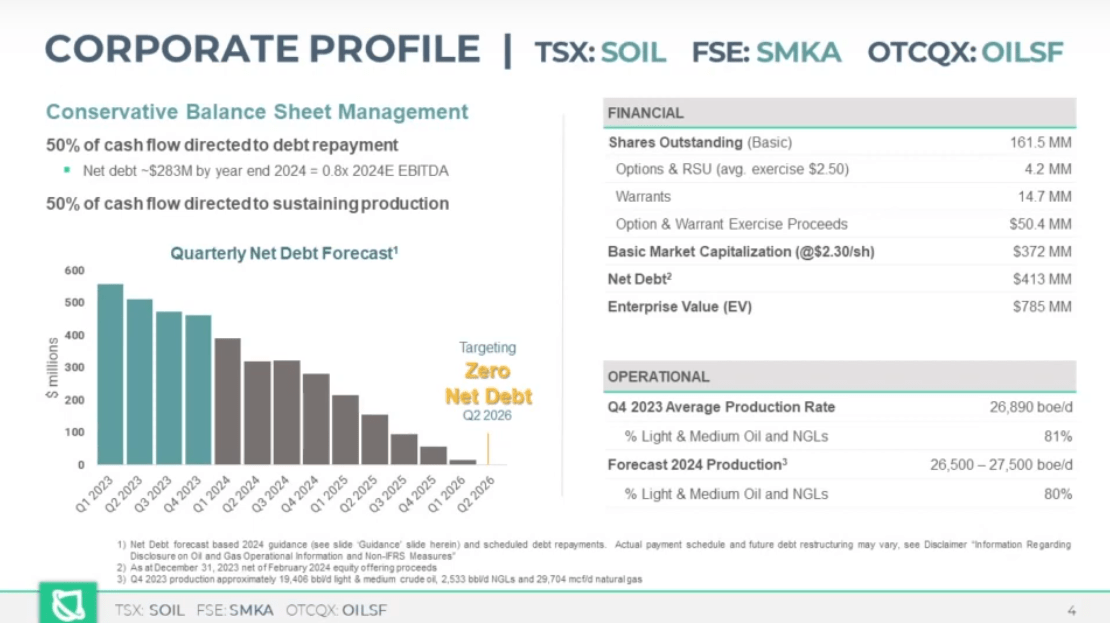

The company has taken on a good bit of debt in these transactions, but seems committed to reducing it as a matter of priority. Net debt is expected to be CAD$792 million or 1.2x next 12 months EBITDA, decreasing substantially over the next 12 months, targeting approximately $600 million, resulting in 0.9 to 1.0 debt to EBITDA on a trailing 12-month basis. The transaction is expected to close on June 14, with an effective date of January 1, 2024. With this mindset and the cash flow to support it, I think I would note the company’s incremental progress, as noted by CFO Scott Sanborn during the call:

In total, Saturn repaid $76 million of debt, resulting in net debt quarter end of $386 million or 1.4x on an annualized basis.

OILSF Corporate Profile (OILSF)

Risks

By this time, the operational thesis for the company’s low decline production is well understood, as many companies we cover have similar profiles. The risk is primarily oil prices, WCS discounts to WTI, and, of course, export access via the TMX line. With the vacuum created by the intake demands of the TMX export access shouldn’t be a problem.

There is also a risk associated with the company’s ambitious growth plans. A miss in delivering this production-for any reason could be a reason for the shares not to re-rate higher as the analysts expect.

Your takeaway

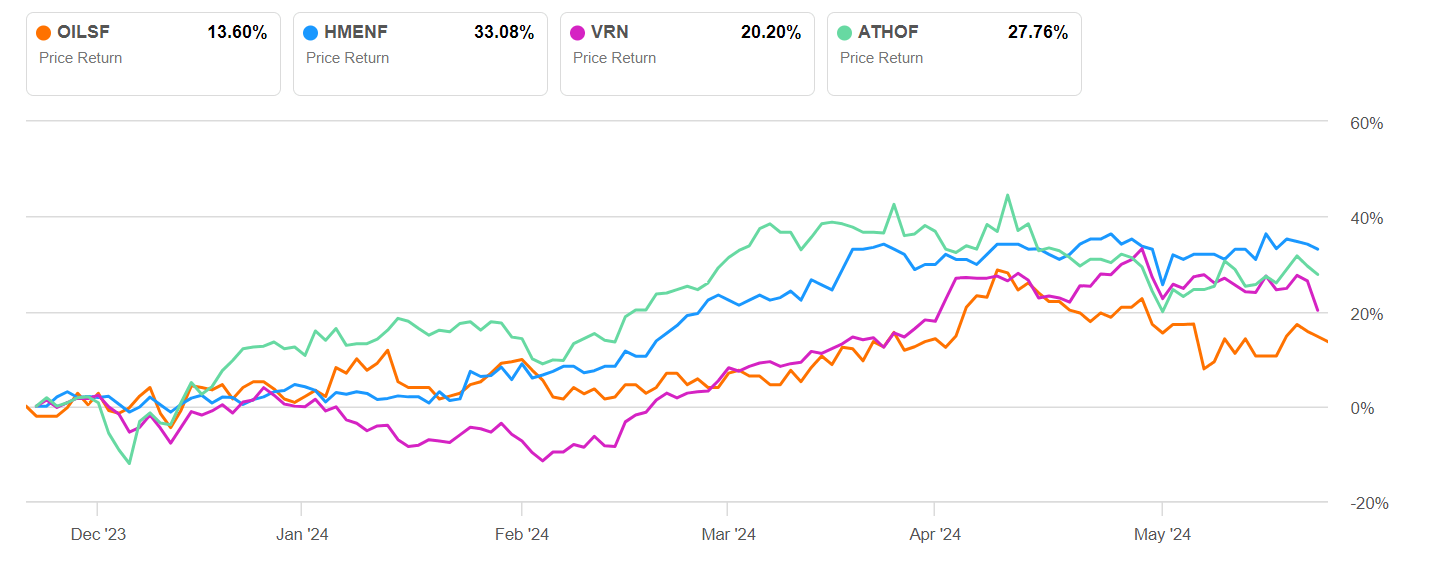

OILSF is trading at ~2X EV/EBITDA and $27,500K per barrel, using their forward YE 2024 exit production rate of 40K BOPD. These are very attractive metrics. Measured against a potential cohort group, we can see that OILSF has performed poorly in the marketplace, rising over the past six months just 13.8%. That is explainable by the acquisitions, debt assumption, and stock dilution. That can be potentially offset by management’s commitment to reduce debt, and right size the balance sheet.

OILSF Cohort group (Seeking Alpha)

The carrot here is that once debt is paid down, cash flow will be available for the usual shareholder returns. If, as previously noted, if the company meets or exceeds Q-2 estimates, shares could pop higher. That, with the orderly pay down of debt and increasing stockholder equity, shares could rally toward analysts’ estimates. I’ll let the analyst’s figures stand here as to what the high side might be. At the same time, I note that discerning and patient investors might want to take a position in Saturn Oil & Gas Inc. stock given the substantial discount to NAV.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.