Andriy Onufriyenko/Moment via Getty Images

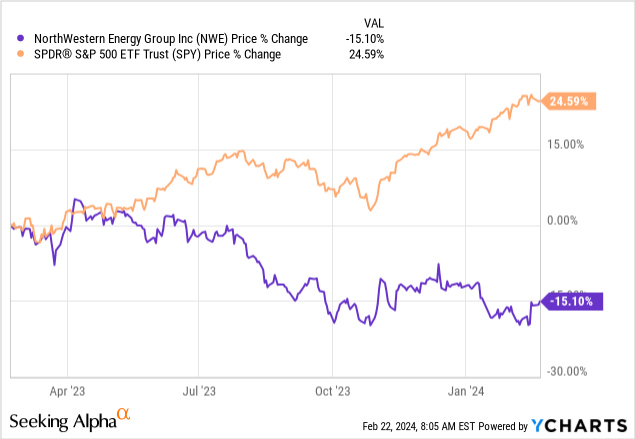

It has been about ten months since I last updated my views on the utility company NorthWestern Energy (NASDAQ:NWE), a relatively small gas and electric utility that primarily serves Montana and South Dakota, although with a presence in Nebraska as well. My view back in May 2023 was that investors should be wary of the company’s capex spending needs (which are significant), as it was clear that the company would need to both take on additional debt with interest rates elevated, and raise additional equity. While it has been a reliable dividend payer, yielding around 4.35% at the time, I did not see any special basis to recommend it. That particular analysis was written very near the 52-week-high point for the shares, which are now down around 12% on a total return basis.

With full year 2023 earnings just released and some contours provided for 2024 guidance, I believe it is a good time to revisit the investment thesis here and evaluate the direction things are headed.

2023 In Review

Before jumping into the 2023 numbers, I have two notes to point out that are not directly pertaining to the financial results. First, NorthWestern Energy initiated an organizational restructuring in 2023, separating out into the holding company of “NorthWestern Energy Group” and ultimately two subsidiaries that are the operating entities, one for Montana, and a second for South Dakota and Nebraska. That process is now complete, and while the impact on shareholders should be minimal, it will likely impact how the company raises debt going forward and limit what assets can be encumbered. Secondly, like any other regulated utility, NorthWestern has to receive permission from assorted state boards to increase the rates they can charge customers, and NorthWestern did receive the necessary approvals from Montana and South Dakota to raise rates, though not always by as much as the company had requested.

In terms of 2023 results, starting with the income statement, revenue for the year saw a decline compared to 2022, coming in at $1.42 billion versus $1.48 billion the year prior. However, the largest expense – fuel and transmission expenses – declined by ~$72 million, helping boost operating income from $263 million to $300 million in spite of the lower revenue, and likewise net income also rose 6%, to $194 million. The per-share earnings declined somewhat as the share count has been rising, falling from $3.25 to $3.22 in 2023.

Turning to the balance sheet and cash flow statement, investors have known from management to expect fairly hefty spending on capital expenditures as NorthWestern is building more capacity in order to rely less on bringing in energy from elsewhere. Specifically, that guidance has been for ~$500 million per year as part of a $2.5 billion investment plan over multiple years. This is clearly showing up on the balance sheet, with greater net property and plant assets of $382 million carried at 12/31/23, though $566 million of cash was used in investing activity per the cash flow statement. This investment was supported through the combination of strong operating cash flow for the year of $489 million, $300 million in long-term debt, and $74 million in common stock issuance. The new debt contributed to net additional long-term debt at year-end of $210 million, sitting at a total $2.7 billion; and as expected, interest expense went from $100 million in 2022 to $115 million in 2023.

The $300 million in new debt is worth taking a brief look at just to have an idea of what sort of cost of capital NorthWestern has access to. Per the 2023 10-K (emphasis added):

we issued and sold $239.0 million aggregate principal amount of Montana First Mortgage Bonds (the bonds) at a fixed interest rate of 5.57 percent maturing on March 30, 2033. On this same day, we issued and sold $31.0 million aggregate principal amount of South Dakota First Mortgage Bonds at a fixed interest rate of 5.57 percent maturing on March 30, 2033. On May 1, 2023, we issued and sold an additional $30 million aggregate principal amount of South Dakota First Mortgage Bonds at a fixed interest rate of 5.42 percent maturing on May 1, 2033.

Issuing 10-year maturities for ~5.50% is to be expected in the current rate environment. I find the rates to be on par with those being paid by another utility, American Electric Power (AEP), for example, and the rate is about 25 basis points higher than the dividend yield. While these rates are at the very top end of the scale of NorthWestern Energy’s debt, it can be managed. In comparison to some of the company’s other large debt obligations, the $450 million issue that matures in 2044 is fixed at 4.176%, and its $250 million issue maturing in 2047 is set at 4.03%. Many of NorthWestern’s other smaller issues have lower coupon rates than these even, and the two operating entities have investment-grade A- ratings for secured debt, as recently reaffirmed by Fitch.

Operating cash flow was definitely a highlight for 2023, as it jumped 60% over the prior year, and 122% over 2021’s results. The net income for those periods hasn’t changed anywhere near that much, nor has depreciation and amortization add-backs, and has been the result of some solid working capital management, combined with a net benefit from changes in regulatory assets and liabilities of $145 million for 2023.

Valuation Thoughts

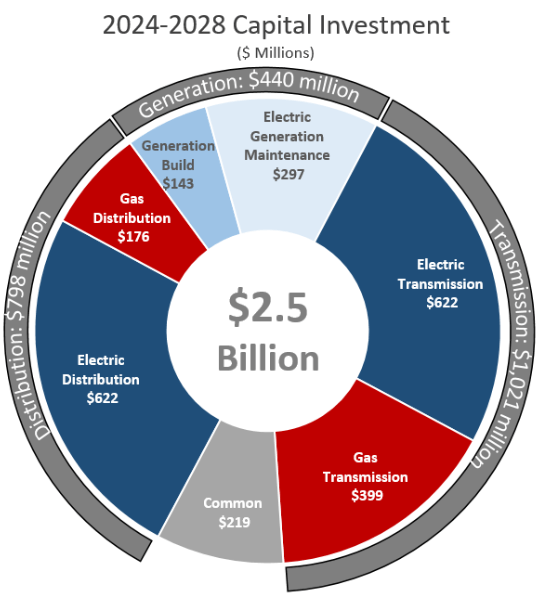

The big fundamental issue facing NorthWestern Energy is that it does not have the capacity to generate all the energy internally that its customer base requires, either for the present, much less factoring in any future growth. As a result, the company has been spending and continues to invest heavily in building or acquiring additional capacity for the long term. It is no small figure; over the 5-year period 2019 – 2023, NorthWestern invested $2.3 billion, and the ongoing 5-year outlook is to need $2.5 billion available for building out and maintaining its power generating and transmitting base.

Northwestern Energy Group, Capex Plan 2024-2028 (2023 Earning Presentation, Slide 15 (https://www.northwesternenergy.com/about-us/investors/financials/earnings#))

The capital for this investment has to come from somewhere – some combination of being borrowed, raising additional equity, and from the excess cash flows the business generates. In the meantime, it has to import energy from other places to deliver to its customers whenever there is a shortfall.

They have made some smart and timely choices in the recent past to help bridge their way as they go. For example, they are acquiring an additional 222 MW capacity from a coal-fired plant at Colstrip; this transaction costs nothing upfront to NorthWestern, and the company will be taking over the additional operating costs from Avista (AVA) essentially in January 2026. This is doubling NorthWestern’s allocated energy production from this particular site without adding a massive debt burden to build new capacity from scratch. While it can be argued that there is not necessarily a long-term desirability for coal-burning generation, in the short term it will ease the transition for NorthWestern and provide breathing room while they work to fund other additions to their portfolio of assets. In another case, in Q3 of 2021, the company opted not to move forward with a project in Aberdeen, South Dakota. Coming through Covid-19, inflation had driven expenses that spiraled beyond what made sense, and they were willing to halt the project once it was evident the return on investment was not there. However, that sort of decision also shuffles around how the company ultimately plans to bring online all the capacity it wants to have available.

The base plan as outlined by management for funding the $2.5 billion is premised on debt and internal capacity to fund it from cash. Management was quite clear that for this particular plan as outlined, they do not anticipate raising additional equity. Any need of additional equity would be done only to pursue incidental opportunities beyond the scope of what they are planning to do. In the words of the CFO Crystal Lail on the recent earnings call:

With regard to 2024 financing plans, we’ve talked about no equity in our plan. So a significant capital plan here to invest and deliver to our customers supported by debt issuances, which will include a bit of refinancing and then a very manageable overall financing plan to support that capital structure and leave us where we need to be, and importantly, in a balance sheet and a position of strength as we move forward.

That approach should accrue to the benefit of the shareholders, depending of course on the actual debt funding and terms. With the rate increases approved in Montana and South Dakota, projections are for around an additional $100 million in revenue per year, with consensus expectations for $1.66 billion for 2024 (though based on just two analysts’ figures); I think a range of $1.55 billion to $1.65 billion is a fair starting point; I’ll assume the mid-point of $1.60 billion for simplicity. Based on the four-year historic average (2020 – 2023), NorthWestern’s typical EBITDA margin was 34% (ranging between 32% and 37%), which estimating would put forward EBITDA for 2024 at ~$545 million. Current enterprise value is $5.67 billion, but for 2024, the capital investment plan is guiding to add net debt on the order of $175 million; all else equal, EV would edge up to $5.85 billion. The result is a forward multiple on EV / EBITDA of 10.73x, pretty well directly in-line with the sector median of 10.69x (according to Seeking Alpha). From this vantage point, I conclude that NorthWestern is fairly valued.

While the EV/EBITDA multiple is nothing special, what does stand out as potentially attractive at these levels is the dividend yield. NorthWestern just raised the dividend very modestly to an annual payout of $2.60 per share, which comes to over a 5.0% yield at the current levels. This level is well over its own 5-year average yield of 4.12%, and similarly well above the sector median close to 4.0%. Between the signal given from the raise and the payout metrics (~80% payout relative to earnings, and ~38% payout relative to free cash flow), I believe the dividend to be on the safe side of the spectrum. Here is an opportunity to lock in a pretty safe 5% yield, with modest potential for attractive gains coming from slow but steady EPS growth in the 4% – 6% range (greater than any likely growth in dividends), and further boosting likely as interest rates eventually start to decline. I do not expect to see much in the way of dividend growth over the next several years, as they prioritize using cash to fund the needed capital investments.

Concluding Thoughts

For the moment, I continue to see NorthWestern Energy as a hold, though income-oriented investors looking to add to or start a position here for the long term should do fine. The shares are in an appropriate fair value range for today, and can serve as a stable and defensive position in a portfolio. The 5.2% yield might be an attractive reason to wait, but the total return potential is likely to be bounded by slower growth and the heavy investment required in building out the energy infrastructure needs for large areas across the plains. Management has generally made sound decisions for their shareholders, and is working as best it can to navigate the challenges of being a regulated industry while also trying to fund affordable new capacity and move more towards carbon-neutral fuels. It is undoubtedly a complicated maze of interests and priorities, but I believe they are making sufficient progress to satisfy shareholders over the long term who are looking more for income than growth.