HENRY NICHOLLS/AFP via Getty Images

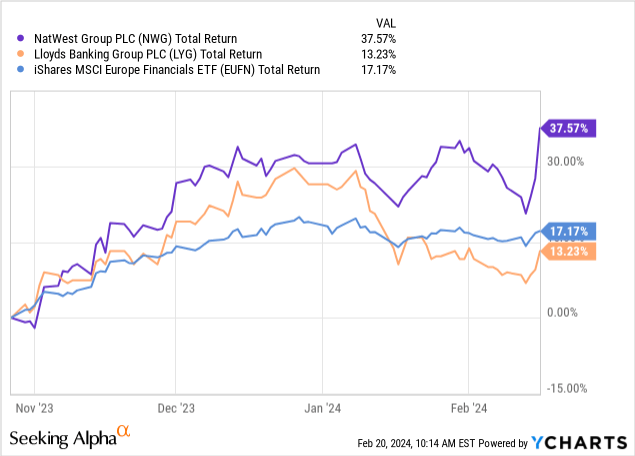

NatWest (NYSE:NWG) stock has regained some lost ground since I upgraded it to ‘Strong Buy’ in my last update in October. Shares of the British bank have returned around 37% in that time in USD terms, mapping to around 24ppt of outperformance versus its closest peer Lloyds (NYSE:LYG) and around 20ppt compared to the broader European financials (EUFN) group.

Better than expected Q4 2023 results explain a chunk of that move, sending the shares up over 7% on the day (Friday, 16th Feb) despite management also delivering reduced medium-term financial goals. That the market wasn’t moved by the latter tells you what you need to know, with analysts’ consensus and indeed the stock’s valuation already reflecting lower-than-guided future profitability in any case.

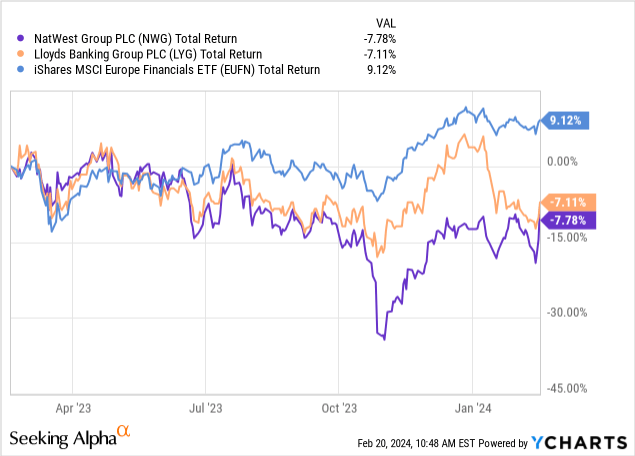

Having fallen sharply before my last update, the recent 40% move still leaves the ADSs down over the past year on a total returns basis. Looking back a little further, NatWest’s ADSs still trade around the same level they were three years ago. That is despite the bank reporting both growth in tangible book value per share (“TBVPS”) and much improved returns on tangible equity (“ROTE”) in that time.

This has basically formed the crux of my investment case here, and I don’t think much has changed given the current quote still represents a decent discount to TBVPS. The shares are slightly more expensive than they were in my post-Q3 update, but with investors still enjoying a decent margin of safety here I am only downgrading one notch to ‘Buy’.

Investment Case Recap

NatWest is one of the largest players in the U.K. banking market, controlling around GBP 700 billion (~$885 billion) in total assets and sporting a double-digit share of U.K. current accounts (~15%) and mortgages (~13%). Just to quickly recap, my overall investment case here rested on two broad points:

- Cheap current and instant access savings accounts fund around half of the bank’s assets, while net interest income (“NII”) accounts for a large share (~75%) of revenue. This combination can lead to a relatively attractive ROTE in a non-zero interest rate environment, which the U.K. moved into following the raising of interest rates in late 2021.

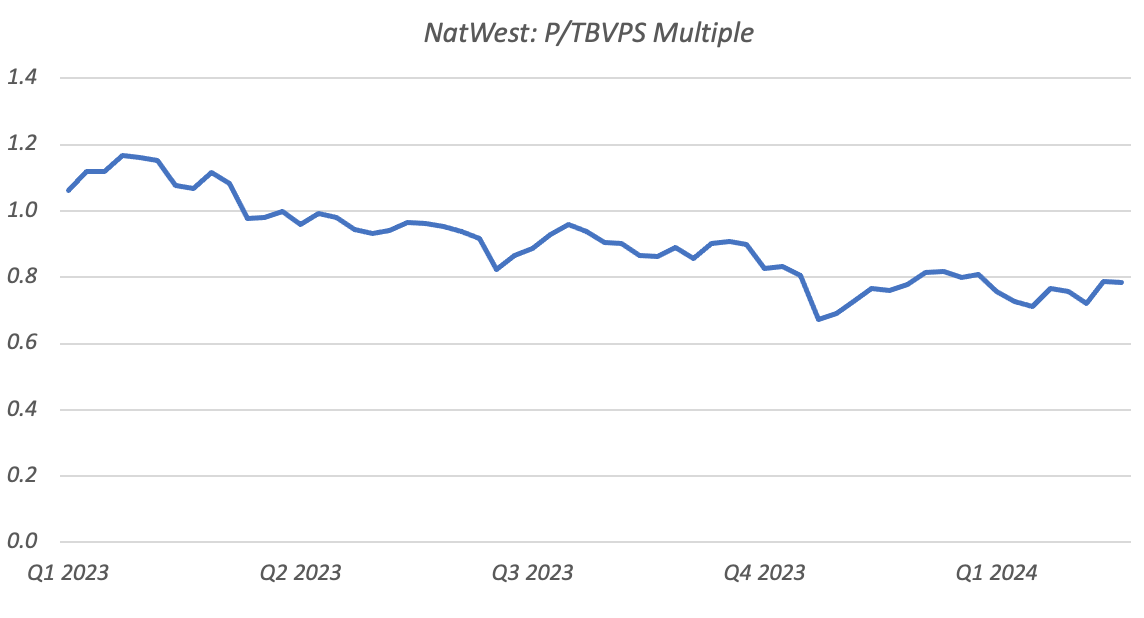

- The above notwithstanding, NatWest stock’s valuation de-rated over 2023, falling to just 0.7x TBVPS following poor Q3 results last October. This valuation was much too cheap relative to the bank’s mid-cycle earnings power and associated capital returns potential.

A Better Q4

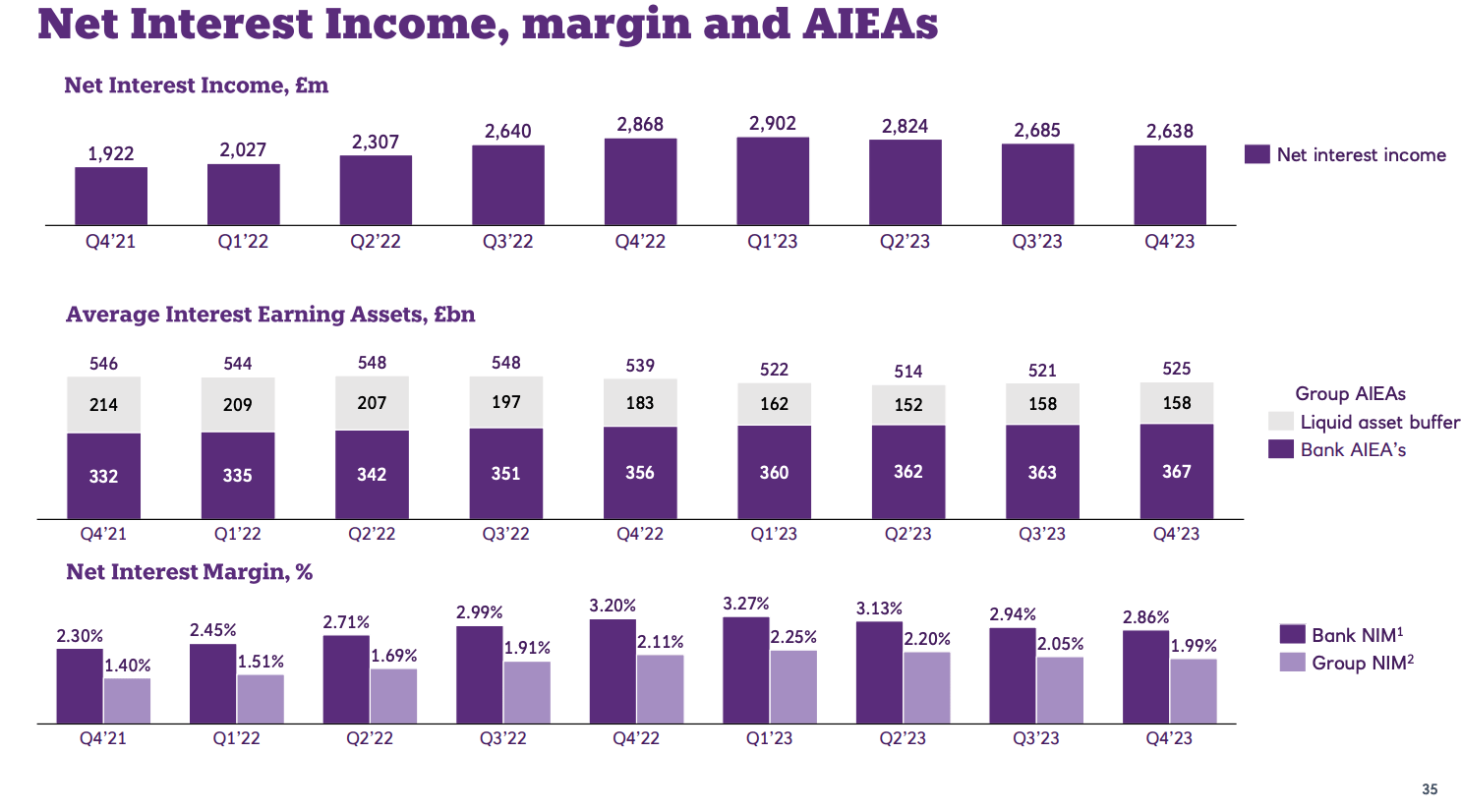

While NatWest had missed consensus estimates on most of its key P&L lines when I last covered it in Q3, it delivered a much better performance in Q4, reporting better than expected figures on both the top and bottom lines.

NII was GBP 2.638 billion in Q4, down just under 2% quarter-on-quarter but around 2% ahead of consensus. Positively, deposit migration continued to show signs of stabilization. Non-interest-bearing balances fell by around GBP 5 billion, or 3%, quarter-on-quarter in Q4, an improvement on the roughly 6% sequential decline posted in Q3. Likewise, more expensive Term deposits increased at a slower pace than in the previous quarter, inching up 1ppt as a share of total deposits to 16%. While net interest margin fell again in the quarter, the pace of decline also moderated, with Q4 NIM down 8bps QoQ versus a 17bps decline in Q3.

Source: NatWest Q4 2023 Results Presentation

Looking forward, I mentioned in previous coverage that NatWest’s structural hedge would provide support to NII. This is practically similar to a fixed-income portfolio generating spread income from a portion of the bank’s deposits. The size of NatWest’s structural hedge averaged just under GBP 200 billion over 2023, ending the year at around GBP 185 billion due to the deposit trends outlined above.

Now, NatWest reported around GBP 2.8 billion in structural hedge income last year on an average yield of 1.42%. While this was up from around GBP 1.8 billion in 2022 (at a ~0.9% yield), the average yield was still well below prevailing yields as it has yet to fully reprice to the current interest rate environment. Management thinks it can reinvest maturities at around 3.1% in 2024, which is around 160bps higher than the average Q4 yield of 1.52%. This will continue to provide support to overall NII even if the Bank of England starts cutting rates later this year.

Profit attributable to ordinary shareholders was GBP 1.229 billion in Q4, around 90% higher than consensus and mapping to a circa 20% annualized ROTE. While non-recurring gains on the tax line account for much of this, pre-tax income was still over 20% higher than consensus. Part of that was due to lower provisioning expenses, with the bank booking just GBP 126 million in Q4 compared to circa GBP 242 million consensus. Annualized cost of risk (“CoR”) was 13bps in Q4 – well below through-the-cycle guidance of 20-30bps. Credit quality remains surprisingly robust, with Stage 3 loans remaining relatively stable last year compared to 2022.

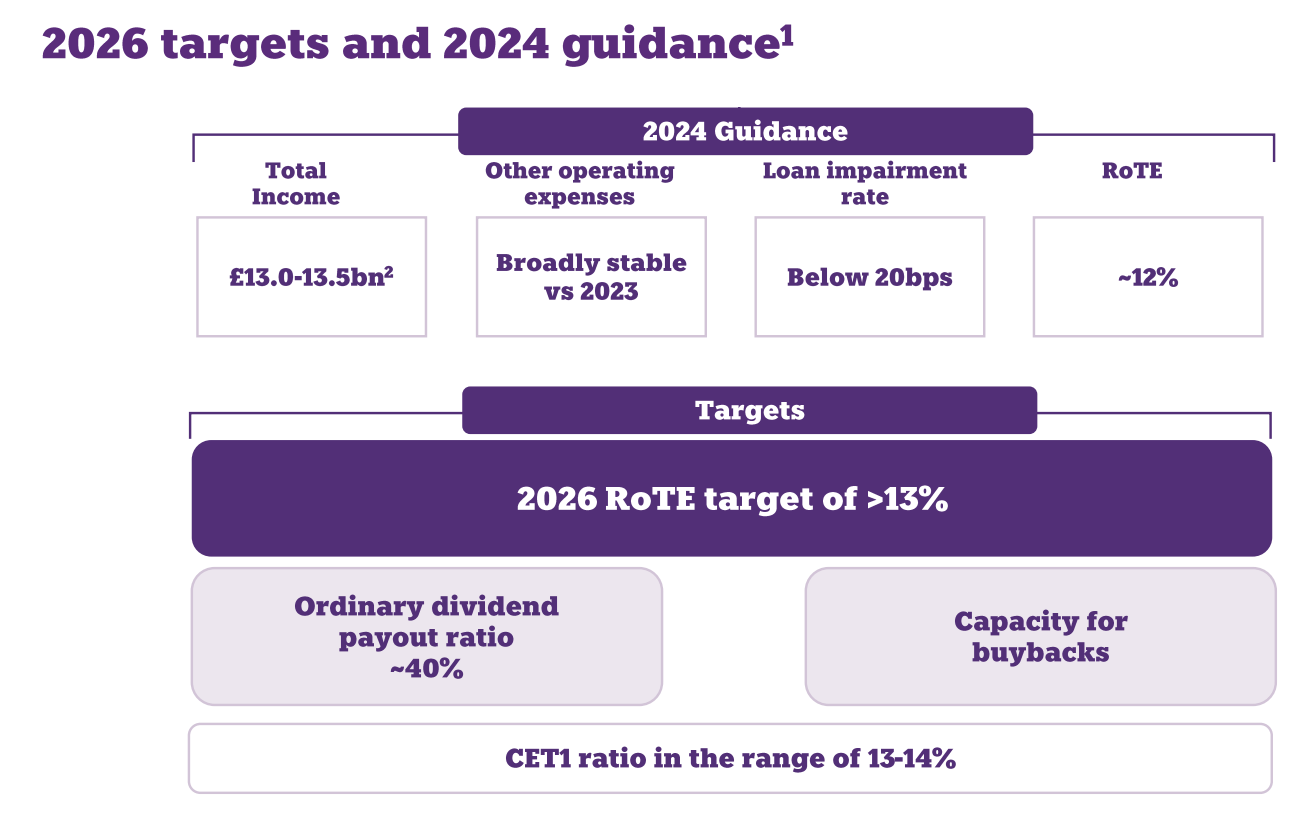

Reduced Targets Not A Major Problem

Alongside results management also released fresh medium-term profitability targets. For 2024, ROTE is guided at around 12%, rising to greater than 13% by 2026. This represents a downgrade on the previous medium-term target of 14-16%. Reasons given for the move include inflation, deposit behavior and future interest rate expectations.

Source: NatWest Q4 2023 Results Presentation

While a circa 2ppt decrease at the mid-point looks significant, the positive share price response suggests that this is not a major problem. This is probably for two reasons. First and foremost, analysts had already baked this in post-Q3, with pre-Q4 consensus pointing to roughly the same 13% ROTE in 2026 that management is now targeting. Said differently, expectations had already been reset by the market and were not surprising. Secondly, NatWest’s cheap valuation also offered investors a significant margin of safety with respect to future profitability.

Stock Remains Attractive

That second point remains the case today. The ADSs trade for $5.92 each as I type, equal to just 0.8x TBVPS. While this represents a slight re-rate from 0.7x TBVPS at previous coverage, the current valuation still affords investors a significant margin of safety.

On $7.37 per ADS of current TBV, a 12% return would translate to around $0.89 per ADS in net income and a P/E ratio of just 6.7x. Capital returns potential looks attractive at that valuation, with a firm 40% dividend payout ratio policy producing a prospective yield of 6% while leaving significant scope for share repurchases on top. If management allocated a further ~30% of net income to buybacks, investors would essentially be looking at a 6% dividend yield plus around 4-5% growth from repurchases. This is on a conservative total payout ratio of 70%.

Data Source: NatWest Group, Yahoo Finance, Author Calculation

The above drives my 1x TBVPS price target, in line with the stock’s early-2023 valuation and implying a fair value of $7.37 per ADS. With around 25% upside from the prevailing quote and attractive capital returns potential, NatWest stock remains attractive overall despite returning 40% since last coverage, and as such I only downgrade one notch to ‘Buy’.