Nora Carol Photography/Moment via Getty Images

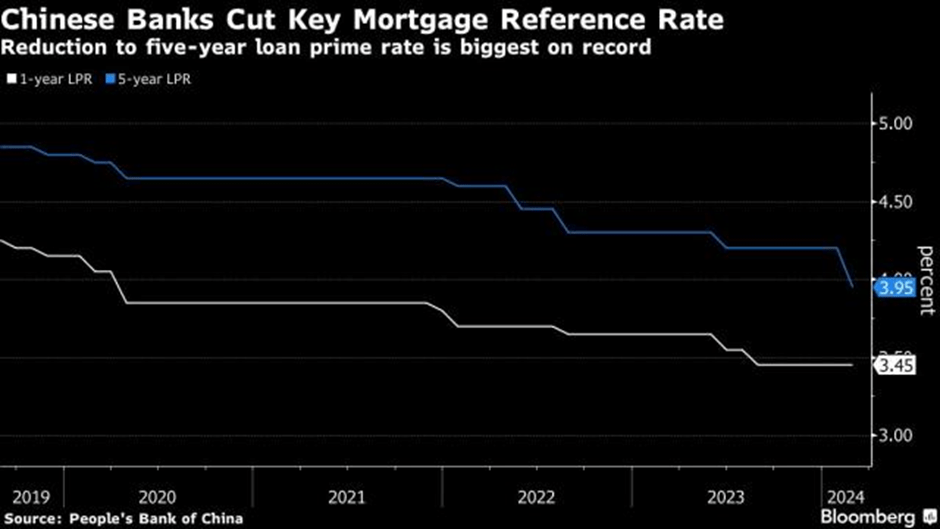

Many of the Chinese macro headwinds I’ve been previously concerned about aren’t easing anytime soon, but that doesn’t mean the country’s equities aren’t investable at the right price. Yes, inflation readings remain negative (at consumer and producer levels) amid weak demand, and all-important property indicators (e.g., developer sales down low-double-digits % YoY) continue to paint a negative picture. But unlike last year, policy support is coming through a lot more strongly, which bodes well for China stocks. This week was a case in point, as the PBOC (i.e., the Chinese Central Bank or ‘People’s Bank of China’) made another clear signal of intent by cutting its five-year loan prime rate, the country’s mortgage benchmark, by a record 25bps. Given the wide rate differentials with the US and elevated ‘real’ rates, there’s still ample space for more monetary easing down the line, in my view, particularly if the Fed follows through with its own rate cut path. Large-scale easing, whether via the fiscal or monetary path, bodes well for broader Chinese equities – even banks, given the prevailing debt service overhang on the sector-wide multiples.

Bloomberg

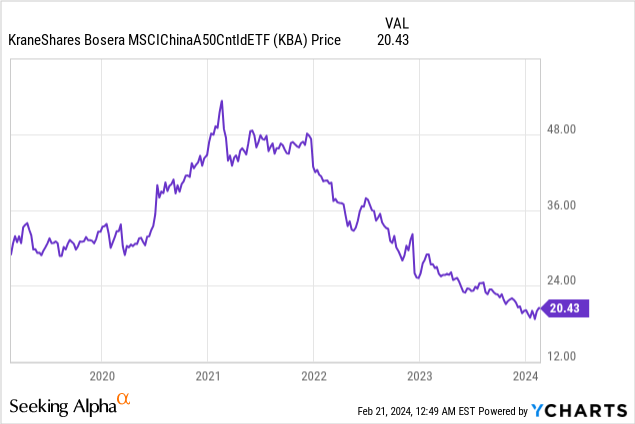

The other big policy push in recent weeks is the government’s reported plan for a RMB2tn ($278bn) ‘stock market rescue fund,’ with more recent news flow indicating an upsized RMB10tn ($1.4tn) ‘rescue’ may be in the works as well. To fully capture the benefits from a near-term ‘rescue,’ onshore large-cap ETFs like KraneShares’ Bosera MSCI China A 50 Connect Index ETF (NYSEARCA:KBA) make more sense than offshore funds, in my view. After all, the ‘national team’ has shown a clear preference for domestic ETF purchases in the past, funded by state-owned corporate coffers, foreign exchange reserves, and pension funds, among others. Also, worth considering are potential foreign capital inflows in anticipation of a large-scale rescue, with KBA’s widely owned constituents again standing out as beneficiaries.

Bloomberg

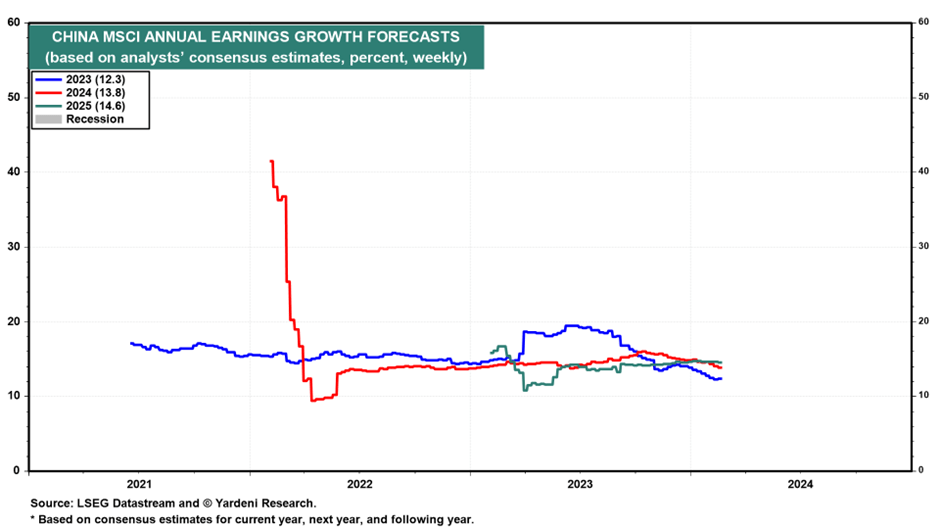

Catalyst or no catalyst, though, the fact that KBA’s dividend yields (never mind earnings yields) are now higher than the equivalent Chinese risk-free rate means we may well be at trough valuation levels here. And in contrast to the current <10x forward P/E of the KBA portfolio, consensus estimates still call for an earnings growth pace in the low-teens % through 2025. So even if we see more downward revisions from here, the wide margin of safety means investors stand a great chance of still coming out ahead.

KBA Overview – Competitively Priced Play on China’s Blue-Chip Franchises

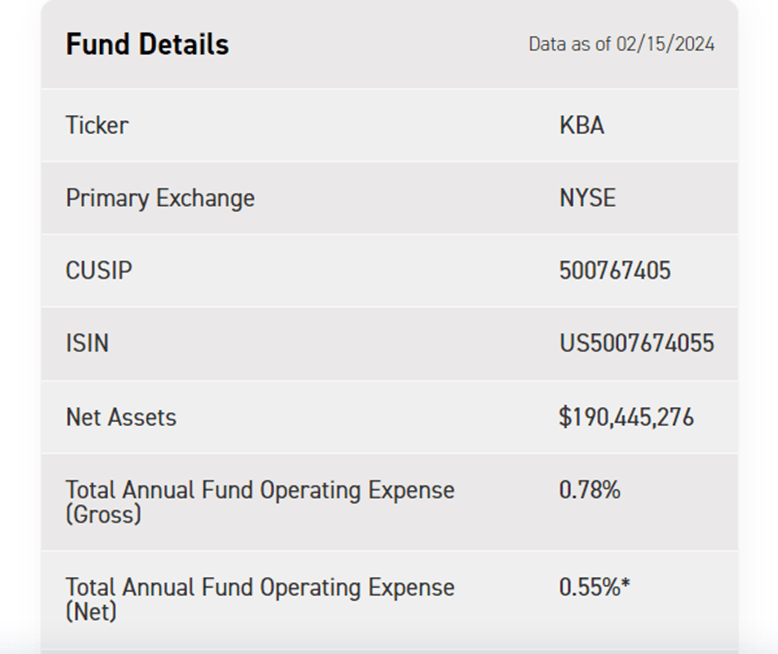

The KraneShares Bosera MSCI China A 50 Connect Index ETF tracks the fifty largest and most liquid mainland China-listed large-cap stocks (i.e., A-shares) via the MSCI China A 50 Connect Index. Amid deteriorating investor sentiment, KBA has seen a steep decline in net assets in recent months to ~$190m at the time of writing, though it remains one of the larger A-share ETFs. The fund also maintains its ~0.8% gross expense ratio, which, including fee waivers (through August 2024), gives it an industry-low net expense ratio of 0.55%. By comparison, comparable A-share ETFs like the iShares MSCI China A ETF (CNYA) and the Xtrackers Harvest CSI 300 China A-Shares ETF (ASHR) charge a net 0.6% and 0.65%, respectively. KBA also offers the tightest median bid/ask spreads at 5bps (vs. 10bps for ASHR and 8bps for CNYA), so all things considered, it screens very competitively on overall cost.

KraneShares

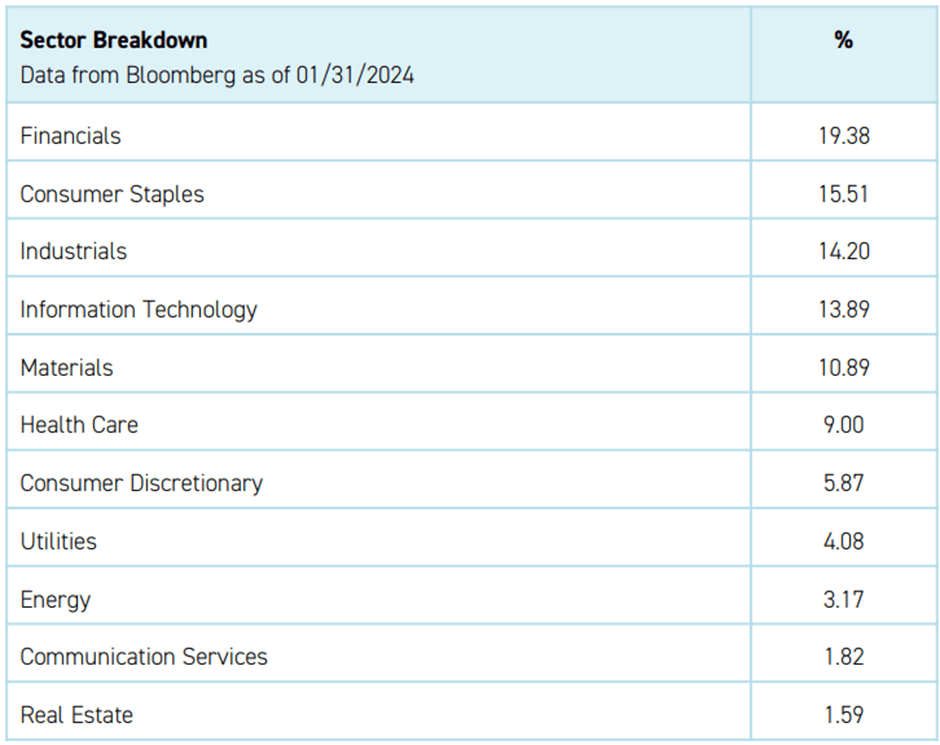

Per KBA’s January 2024 fact sheet, its 50-stock portfolio remains fairly evenly split, a result of the underlying index’s diversified weighting system. Financials remain the largest exposure at a slightly increased 19.4%, followed by Consumer Staples (15.5%) and Industrials (14.2%). In line with previous quarters, Information Technology (13.9%) and Materials (10.9%) are the other key exposures within the top-five list.

KraneShares

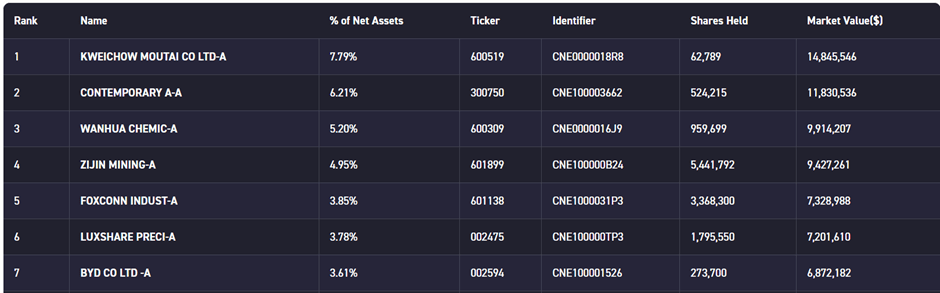

The single-stock list is, like most other A-share ETFs, headed by baijiu company Kweichow Moutai (broadly unchanged at 7.9%). Battery producer Contemporary Amperex Technology continues to see its portfolio share decline to 6.2% amid industry-wide headwinds, though it remains the second-largest holding. The big change this quarter is the lower allocation to electric vehicle leader producer BYD (OTCPK:BYDDY) in favor of electronics manufacturers Foxconn Industrial Internet and Luxshare Precision. Relative to comparable A-share ETFs like CNYA and ASHR, the single-stock profile is also much lighter on major bank stocks – the result of its weighting constraints.

KraneShares

KBA Performance – Steep COVID-19 and Post-COVID Drawdowns

Along with the rest of the Chinese equity market, KBA investors have suffered a torrid time over the last few years. Despite hopes of a post-COVID recovery, 2023 turned out to be a particularly bad year, with the fund suffering a steep -17.1% decline. Having moved even lower in early 2024, KBA’s annualized three and five-year returns now stand at a dismal -17.7% and +0.3% in NAV terms, respectively. By comparison, ASHR and CNYA slightly outperformed over similar timelines, helped by more diversified (and defensive) equity portfolios.

KraneShares

KBA’s headline performance numbers don’t make for great reading, but the fund’s narrow tracking error vs. its benchmark MSCI China A 50 Connect Index is notable. Since transitioning to the MSCI China A 50 Connect Index over the last year, its annualized NAV return has deviated by a much narrower ~43bps – well below historical levels and the 194bps tracking error for ASHR and ~62bps for CNYA. Given the fund’s underlying MSCI China A 50 Connect Index affords it structural advantages such as a corresponding futures product to hedge market making exposure and consideration of China’s ~30% foreign ownership limit, expect KBA’s industry-leading tracking error to sustain into the coming years.

KraneShares

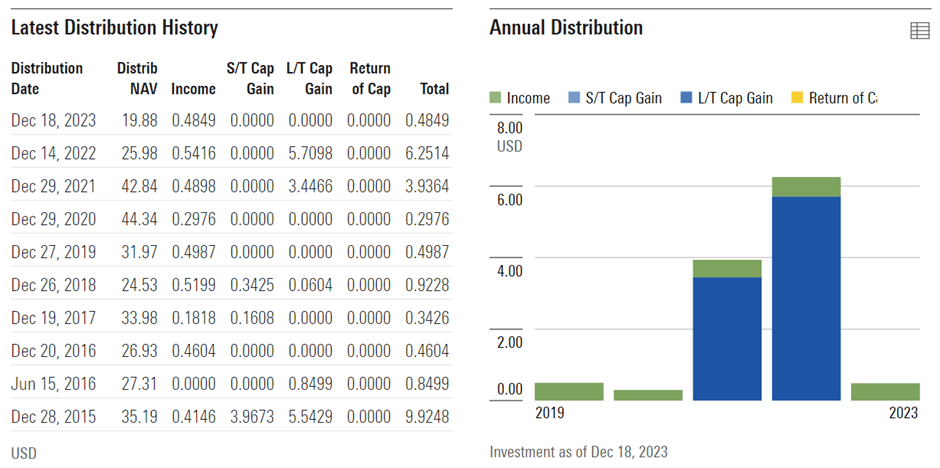

On the distribution front, last year’s $0.48/share payout, combined with a much lower NAV base, means its trailing income yield stands at a very solid ~2.4%. ASHR (~2.6%) and CNYA (4.6%) offer much higher yields, though, helped by their broader portfolios and larger allocations to cash-generators in sectors like banking. That said, KBA’s unique combination of quality and price (portfolio currently at a trough level <10x forward P/E) means that on balance, the fund screens at the very top relative to other mainland vehicles.

Morningstar

Poised to Benefit from a Chinese Dragon Year Turnaround

China is emerging as a potentially catalyst-rich equity story in 2024. In contrast to the gradual policy easing we saw last year, policymakers have started the year with far more intent on the monetary and fiscal fronts. Following a big 50bps cut to reserve ratio requirements last month, the Chinese central bank has unveiled another big cut to its benchmark mortgage rate, further cushioning debt serviceability for corporates and households. Fiscal easing, on the other hand, has been understandably handcuffed by elevated debt obligations (on and off-balance sheet), though recent plans for large-scale equity market stabilization, funded by state coffers, indicate an equity-friendly shift in priorities. Given its concentrated focus on mainland large-caps, KBA screens very attractively as a play on upcoming policy support, with trough-level fundamental valuations (vs a consensus low-teens % earnings growth outlook) further adding to the safety margin here.

Yardeni