New York Community Bancorp has fallen on hard times. It’s not appropriate for most investors, but turnaround types still have time to buy it.

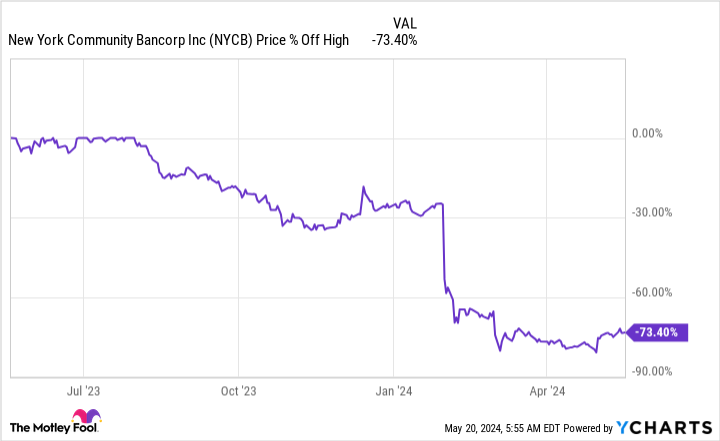

For most investors, New York Community Bancorp (NYCB 3.10%) is a stock that will be best avoided. The regional bank has had a rough year and that is reflected in the stock price, but it is well positioned for a turnaround, which may interest more aggressive investors. And since the stock trades some 70% below its 52-week highs, you aren’t too late to buy it.

What went wrong at New York Community Bancorp?

A bank stock that’s fallen 70% from its 52-week high? That’s a clear warning sign. Banks are generally supposed to be conservatively run financial institutions.

There are several reasons for the terrible stock performance. For starters, the bank cut its dividend … twice. It is now paying just a token $0.01 per share per quarter. That’s something companies do when they are in financial trouble but still want institutional-level investors with dividend mandates to stick around.

Image source: Getty Images.

The reason for those dividend cuts, meanwhile, is twofold. First, the company expanded via acquisition but wasn’t really ready to handle that growth from a regulatory perspective. Second, rising interest rates resulted in an increase in troubled loans right as the company was facing greater regulatory scrutiny.

Basically, the company had to hit the reset button as it became a more important bank. That included the urgent need to shore up its balance sheet (thus the dividend cut), necessary upgrades in its internal operations, and a reshuffle of its management team to bring in more experienced leaders. The old leadership team fumbled the ball when it came to expanding New York Community Bancorp.

There’s plenty of time to buy New York Community Bancorp

When the bad news started coming out, the situation looked dire for New York Community Bancorp. Although it sailed through the bank runs at the start of 2023, even buying key assets of one of the failed banks, there was a very real risk that New York Community Bancorp was itself going to fold (thus the steep price decline).

However, it was able to secure a $1 billion cash infusion. That happened fairly quickly, too, which could be seen as a desperate act or a sign that the outlook is maybe brighter than Wall Street thought it was. Notably, the group of investors contributing cash included former Treasury Secretary Steven Mnuchin, who you would assume knows a thing or two about financial institutions. The company has laid out a multiyear plan for getting back on track.

This is where things get a little more complicated for investors. New York Community Bancorp’s dividend yield is around 1% today. That’s well below the yield of the broader market and the average bank. If you are looking for income, you will want to pick another investment. But if you like turnaround stories, management is clearly saying that New York Community Bancorp will be back on track by the end of 2026.

To be fair, that’s at least a year and a half away. So this isn’t going to be a quick fix, but that’s not at all surprising. It takes time to deal with troubled borrowers, and you wouldn’t want to rush the policy and process changes needed to deal with the increased regulatory security that larger banks face. New York Community Bancorp needs to take its time righting the ship or it could fall right back into the same problems again.

Nothing to see here, for now

So the question isn’t really about whether or not you have time to buy New York Community Bancorp; you do. The real question is whether you want to buy it at all. If you want income, the answer is likely a hard no. But if you are more aggressive and don’t mind closely monitoring turnaround situations, the $1 billion cash infusion here suggests that the bank’s recovery process is being executed atop a strong foundation. You just have to go in knowing that the turnaround is going to take some time, during which the stock is likely to remain stuck in the doldrums.