Smith Collection/Gado/Archive Photos via Getty Images![]()

Honda Motors (NYSE:HMC)(OTCPK:HNDAF) is a Japanese automotive player that we’ve covered in the past, focused on the entire industry’s favourable supply chain situation amid a weak yen environment, causing a real growth in unit margins thanks to substantial home grown production and parts sourcing and a very large USD denominated market in the US, which is also the biggest grower in the mix. Despite some recalls and related reserves, pricing action continues to catch up with higher input costs, and associated with strong growth, operating income is expected to increase further as the FY 2024 rounds out. China is also seeing a light at the end of the tunnel, beginning to see some unit growth on the 3 month basis. Buybacks are continuing, and Honda is definitely heading in a right direction.

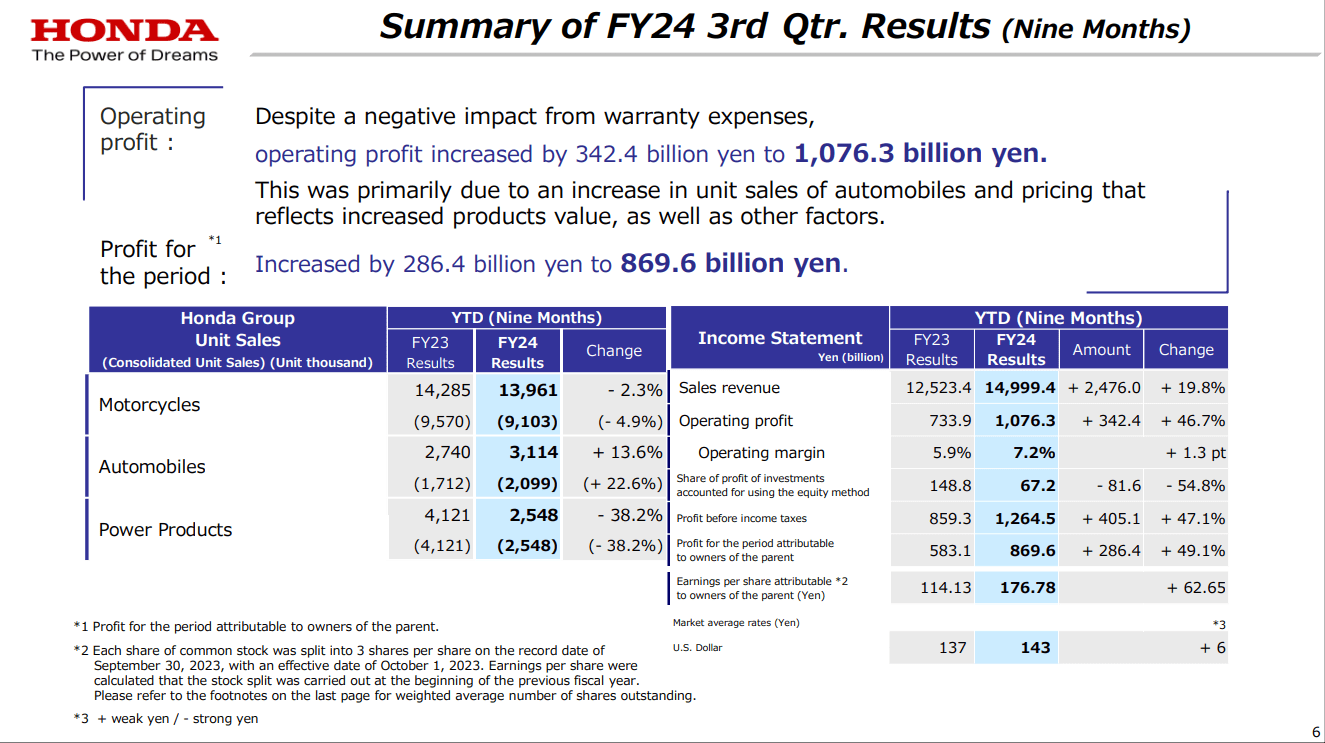

9M Earnings

In motorcycles, there was a bit of give and take. Consistent with our other coverage, Vietnam has been a bit of a sore point for a lot of Japanese businesses that export there, with the economic drag in China affecting Vietnam as their major trading partner. However, geographies like India and Thailand did a good job of picking up the slack here. Brazil also did well, and unit sales ended up being pretty flat YoY. As the year rounds out, no recovery is expected really in Vietnam, and the weak consumer situation in Japan, the only but pretty significant drag on Japanese GDP, will see Japan also have limited contribution in terms of growth.

Longer term, Honda is continuing its plans for a range of electric mopeds and motorcycles, and is raising forecasts for how large that production line’s output is going to be, from 3.5 million to 4 million units in 2030. Considering that the category hasn’t been aggressively addressed yet by an automotive player, we’d be alright with seeing Honda take the lead in high ticker motorcycles.

9m Results (Q3 Pres)

The core automobile business did a lot better. The US business churned out a fantastic performance in terms of unit growth, with the YTD figures showing a 42% growth and the 3 month figures showing a 32% growth in units on a retail basis. China also started picking up in the 3 months results which is encouraging, but also to be expected since China was aggressively troughing in automotive for about a year by now, actually a little bit more. We don’t expect a furious recovery in China as they remain a highly beleaguered economy that shouldn’t be able to support too much consumer durables demand, but we are glad that they are likely to be less of a drag going forward. Other markets like Thailand and Indonesia, major Chinese economic partners who’ve had to absorb some of the Chinese economic fallout, also took a hit in terms of volumes, muting the overall results. This is supposed to persist into the FY guidance as well as 2024 rounds out. With the production recovery in Japan, strong USD denominated destination markets, just like other Japanese automotive players and how we highlighted with Honda in the past, the wedge grows in income, with operating margin raising substantially thanks to the growth of automotive in the mix from 5.9% to 7.2%. Pricing actions also sees the revenue figure outpace the higher input costs which have been sharp in automotive parts in conjunction with unit sales growth, which is going to accelerate profit growth from around 50% to 60% from the 9 month figures to the FY forecast figures. This is in spite of higher warranty reserves on account of the recalls that were needed on a seat sensor issue that caused airbag issues in Honda cars. The US destination sales are carrying the entire Japanese automotive industry, with Honda not an exception.

Bottom Line

The company is also continuing its buyback programme, with this year’s buybacks expected to be around 250 billion JPY. This is consistent with a broad effort among Japanese large caps to address the TSE concerns around capital allocation and low price to book ratios among some of Japan’s most liquid and well-known stocks, as well as in the smaller markets. Around a 3% buyback for the year makes a dent in their net cash position, which seems ridiculous to have as a major automotive player from the only country where real interest rates remain well below 0%. However, more will be needed even though it’s a good start.

In terms of guidance in the future, we think that a repeat performance in the US in terms of growth is going to be hard to expect after the FY 2024. While it should remain a growing market, there’s no guarantee of that. We do think that the benefits of homegrown production but foreign markets in a weak Yen environment should persist, as it is our conviction that higher for longer is the state of affairs in the US, not some other more optimistic scenario. We also think that China should be in a more sustained positive growth mode beyond the FY 2024. This should with some lag also lift Vietnam and Indonesia. We expect Japan to continue to drag.

Valuations remain low. On FY 2024 forecasts for net income, we are looking at a PE of around 9x, offering substantial earnings yield of 11%. Some markets are even coming online in terms of growth. The only thing that could derail Honda would be if the consumer situation becomes weaker in the US, for example in the case of a US recession on account of rates. Otherwise, the yield, which is already high, should grow a while longer. We feel the margin of safety is pretty substantial, and the demonstrated resilience in the US so far is enough to put us at ease.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.