Guido Mieth/DigitalVision via Getty Images

Investment Thesis

I last covered The Clorox Company (NYSE:CLX) in June last year. The stock has had quite a wild ride since then as the company’s sales and profit were impacted by a Cyberattack in Q1 FY24, resulting in a stock price correction. The company was quick to recover from it and was able to recover distribution losses and profitability to a good extent in Q2 FY24, which helped the stock price. However, the stock is still trading below pre-cyberattack levels and the valuation is cheap. I am expecting continued recovery when the company reports its Q3 FY24 results and positive commentary on the growth outlook in the coming quarters. An attractive valuation and good growth prospects make CLX stock a buy.

CLX Revenue Analysis and Outlook

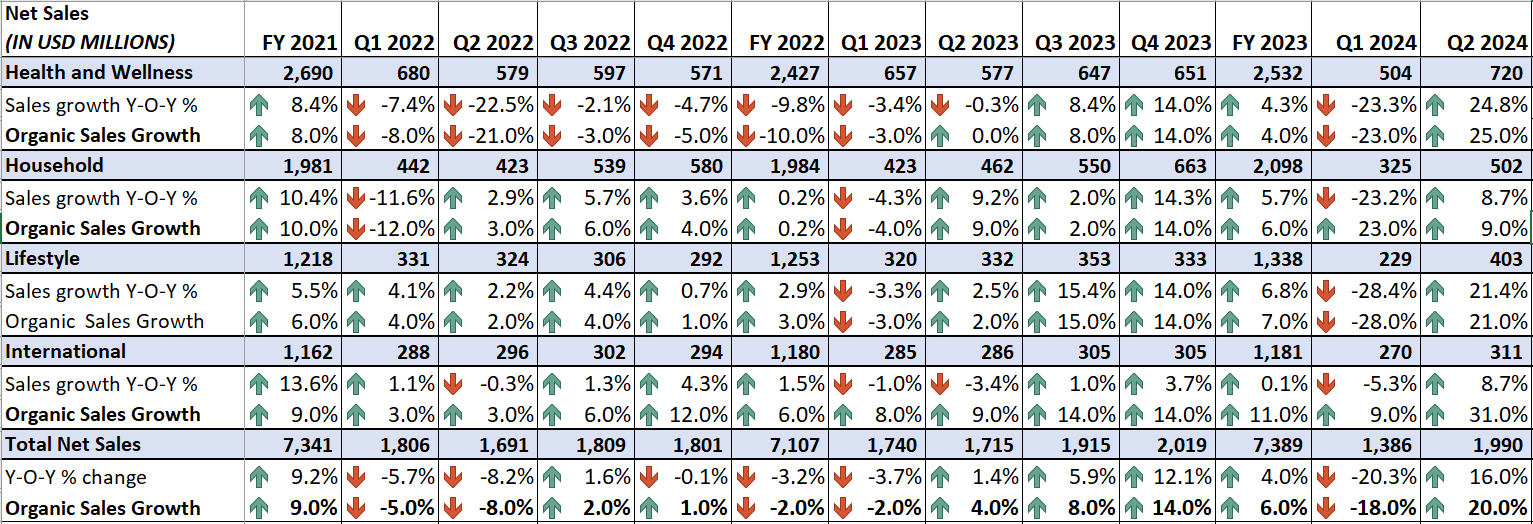

After seeing extraordinarily strong demand for its cleaning and hygiene-related products during COVID, Clorox saw a decline in its sales in FY22. While its volume remained negative in FY2023, strong pricing increases helped the company post positive sales growth in FY23. The company’s volumes were expected to turn positive in the current fiscal year (FY24) due to easy comparisons and inventory destocking ending. However, a cyberattack in Q1 FY24 disrupted the company’s operations and distribution and resulted in lower inventory levels at retailers. The company posted a steep 26% Y/Y volume decline in Q1 which resulted in an organic sales decline of 18% Y/Y in Q1 2024.

In the second quarter, the company did a good job in terms of inventory replenishment which in a good organic volume growth of 13% Y/Y. This coupled with ~7% Y/Y price/mix helped the company post 20% Y/Y organic growth.

CLX’s Historical Sales (Company Data, GS Analytics Research)

Looking forward, I believe the company should continue to deliver revenue growth in the coming quarters.

Management did a good job in terms of inventory replenishment in Q2 FY24 and less out of stocks. SKUs bode well for sales volumes in the back half of the fiscal year.

Moreover, the company also plans to increase promotional and advertising activities moving forward. According to the management, the company’s advertising spend as a percentage of sales is expected to increase to ~11% in FY24 vs ~9.9% in FY23. This should also help support volume growth in the coming quarters.

Further, volume growth should also continue to benefit from the company’s consistent new product launches. CLX has a good track record of increasing its category demand through new product innovations and management has accelerated its new product innovation to keep category demand healthy. The company launched various new products in categories like cat litter, cleaning, and disinfecting in the recent year and I expect elevated investments in new product innovations should continue to build brand relevancy and support the volume levels.

On the pricing front, I expect the pricing benefit to start normalizing from high single-digit to mid-teens levels seen in recent years to low single-digit levels. But together with organic volume growth, it should help the company post mid-single-digit organic sales growth in the coming years, which is a reasonable level of growth for a consumer staple company.

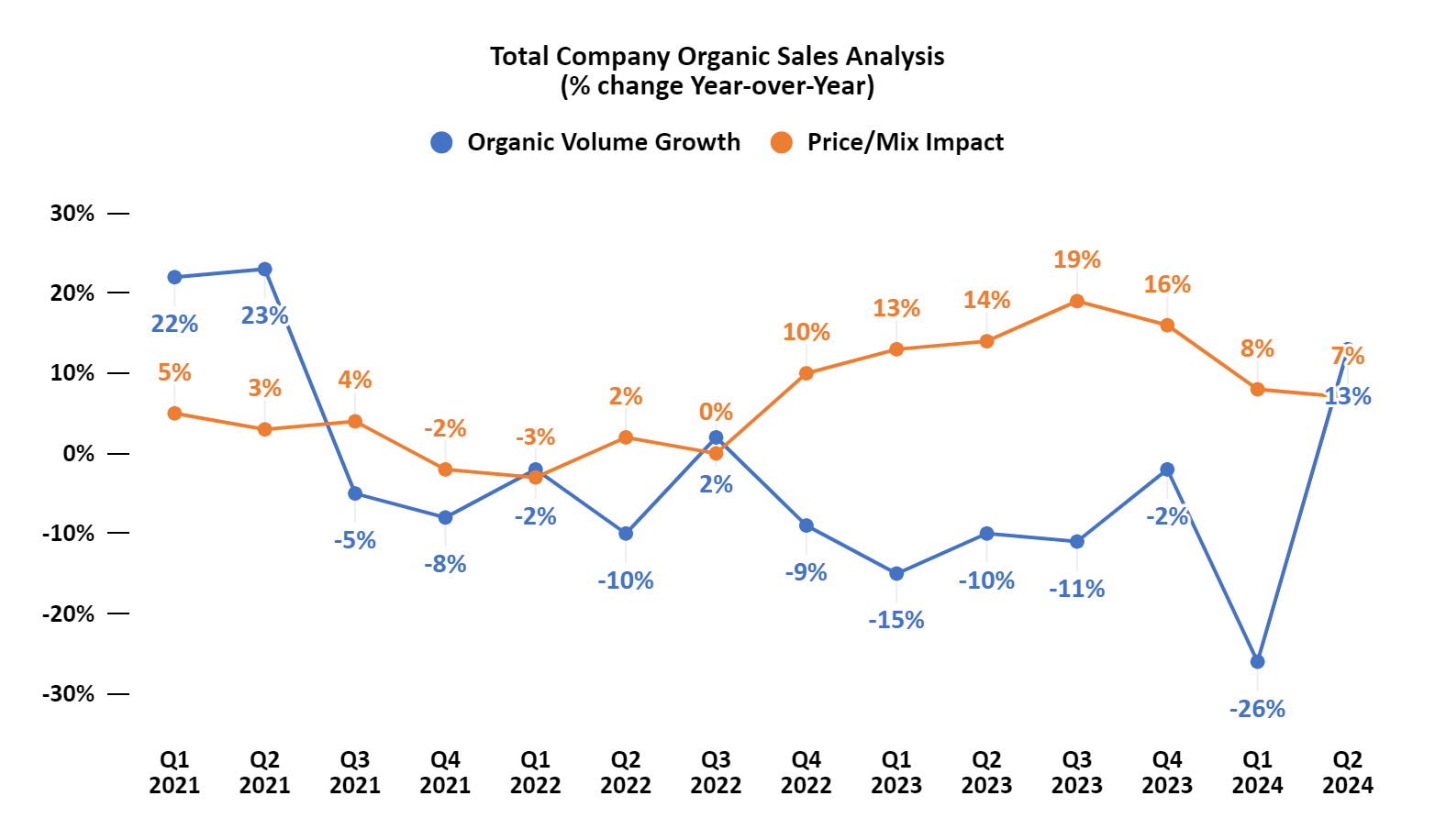

CLX’s Historical Organic Sales Analysis (Company Data, GS Analytics Research)

Inorganically, the company’s growth may be slightly less as it recently announced the divestiture of its Argentina business. However, I am not too worried about it and believe it is a good move for the company as the rapid devaluation of the Argentina Peso was making it difficult to manage the business and creating FX-related headwinds for the company.

Overall, I am optimistic about the company’s near and long-term organic growth prospects.

Clorox Margin Analysis and Outlook

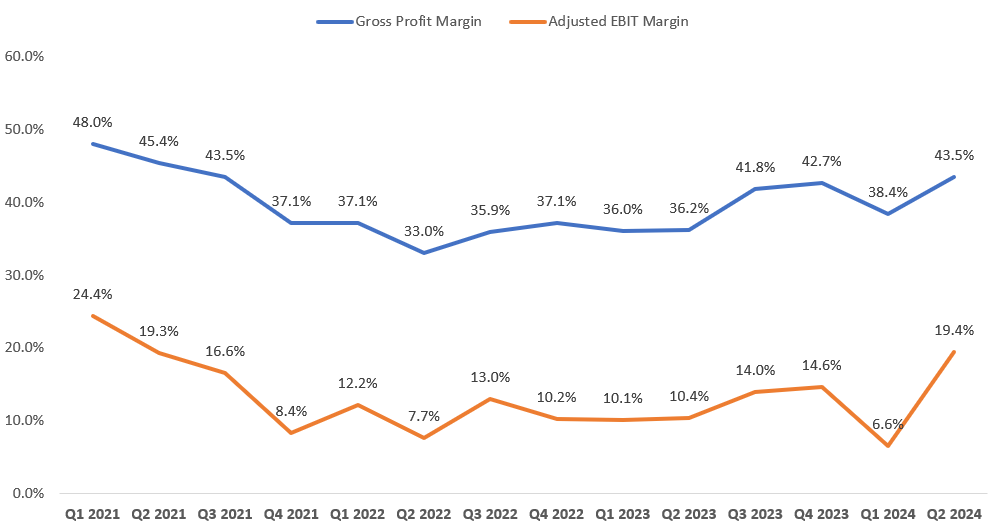

In the second quarter of fiscal 2024, the company’s margins benefited from price increases (a benefit of 380 bps), and cost savings (a benefit of 170 bps). In addition, the margins also benefited from better cost absorption due to good volume leverage. This helped CLX in more than offsetting inflationary pressure and headwinds from negative FX. As a result, the gross margin increased by 730 bps YoY to 43.5%. The adjusted EBIT margin increased 900 bps YoY to 19.4%.

CLX’s Historical Gross Profit Margin and Adjusted EBIT Margin (Company Data, GS Analytics Research)

Looking forward, I believe the company should continue to expand margins and return to annual pre-pandemic levels of around 44%. To summarize the company’s margin growth trajectory, significant inflation over the past two fiscal years adversely impacted the company’s margin. This along with elevated digital investments and volume deleverage due to demand normalization caused a drag on margins versus pre-pandemic levels. However, the good news moving forward is that inflation is moderating. In fiscal 2023, the company incurred a total cost inflation of $400 million. For the full fiscal year 2024, management is projecting total cost inflation of $200 million, which should moderate as the year progresses. This should support the margin growth in the coming quarters. Further Argentina’s business was margin dilutive, and exiting it should help mix.

Additionally, a return to volume growth should also provide good volume leverage and support margin growth. Moreover, as I mentioned in my previous article, the company is also progressing well in its cost-saving initiatives. At the start of fiscal 2023, the company began implementing measures to save costs and improve margins. These initiatives include reducing staff numbers, giving more decision-making power to local teams to adapt to consumer trends, and supply chain optimizations. These initiatives have resulted in healthy margin growth in the last quarter and I expect this trend to continue. Hence, I am optimistic about the company’s margin growth prospects ahead.

CLX Stock Valuation and Conclusion

Clorox is currently trading at a 25.70x FY24 (ending June) consensus EPS estimate of $5.59 and a 22.27x FY25 consensus EPS estimate of $6.45, which is lower than its historical 5-year average P/E (FWD) of 29.20x. Moreover, the company also has a good forward dividend yield of 3.34%. This favorable valuation along with good growth prospects thanks to a return to volume growth, moderating inflation, and cost savings makes the stock a good buy. I believe volume growth continuing in the coming quarters may improve investor sentiment around the stock and help it re-rate higher.

Risks

The company faces risks from the current inflationary environment. While it is expected that inflation should continue to moderate, if it remains higher for longer than expected, it may result in headwinds for both the top and bottom line. On the top line, the company may get impacted by trade downs to private labels and a competitive pricing environment while margins may also be impacted by cost inflation. So, inflation and the competitive environment are two factors to closely watch out for from a risk perspective.