PeskyMonkey

Bullish Stance Despite Challenges

Chewy (NYSE:CHWY) is set to announce its third-quarter financial results on December 6th. We are tracking the latest data points and saw some positive indicators showing that Chewy’s business momentum has rebounded after a challenging second quarter.

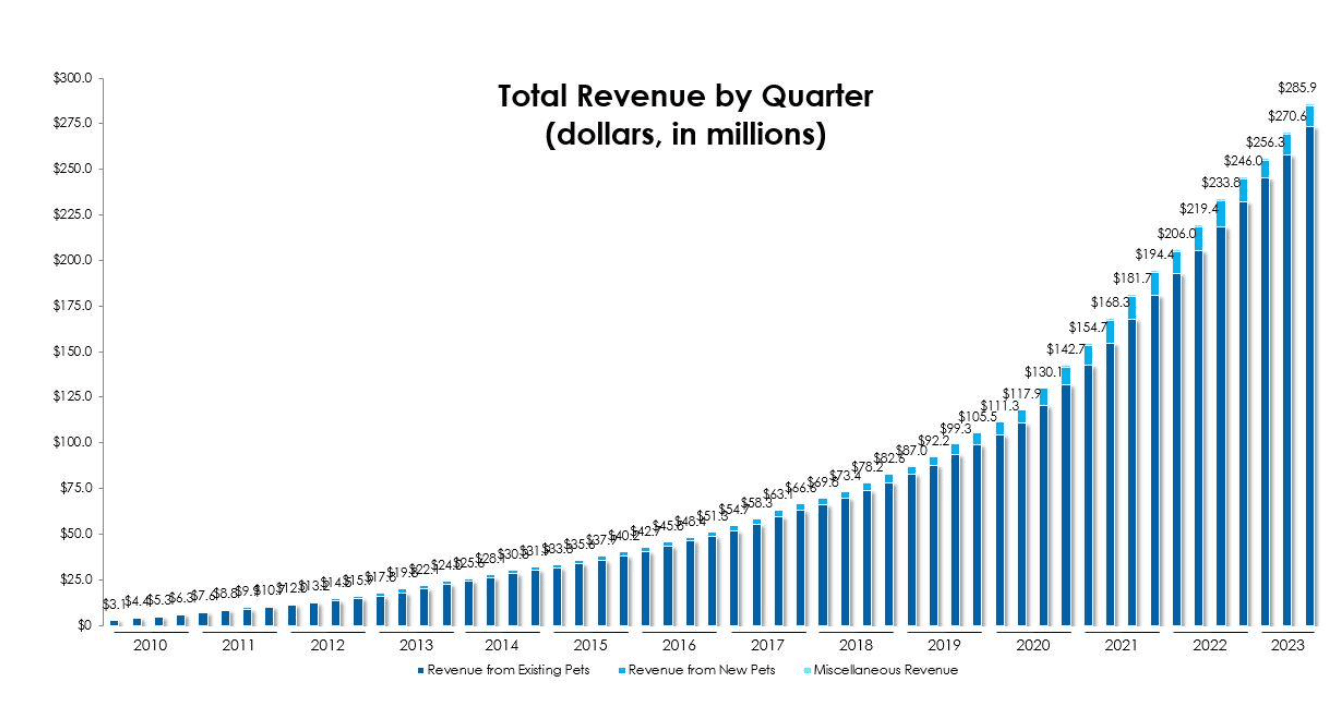

In August, we rated Chewy stock a buy even as we expected the share price to go down due to an acceleration in customer losses last quarter. Our investment philosophy centers around long-term growth potential, so despite near-term headwinds, we remain confident in Chewy’s market leadership. We uphold our bullish call through Chewy’s brand equity and multi-faceted expansion strategy long term. advance, although inflationary pressures persist for consumers, Chewy competes in an essential, recession-resistant industry. Americans spent a record $136 billion on their pets last year – that figure is expected to grow by 5% in 2023. As real wage growth slowly recovers and Chewy attracts new customers, profitability should follow.

Evidence of Recovery

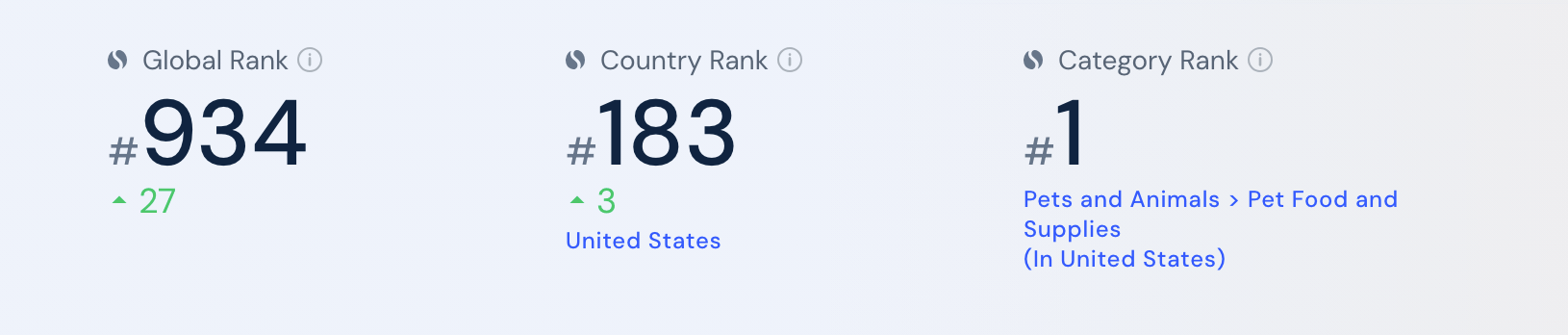

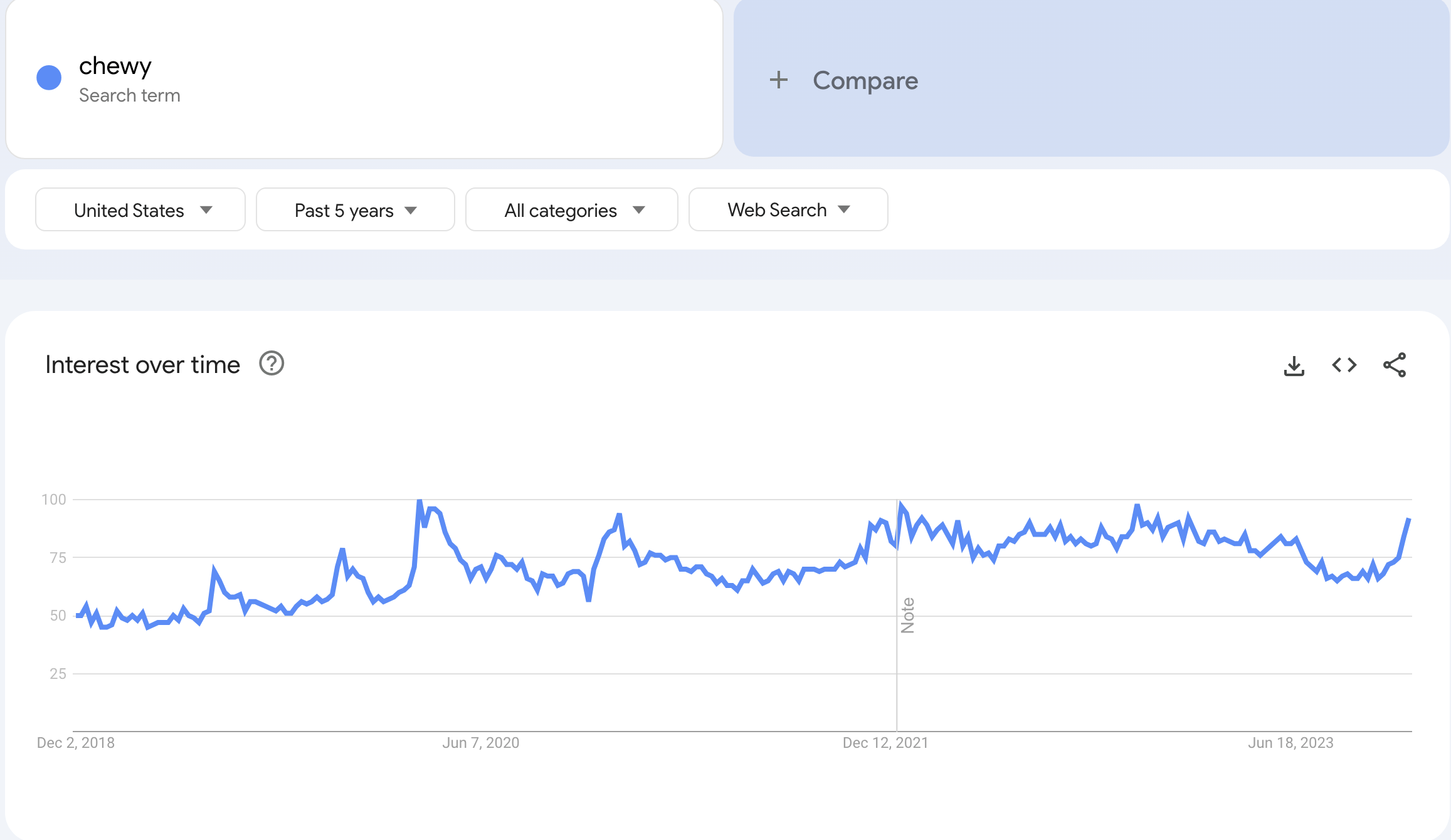

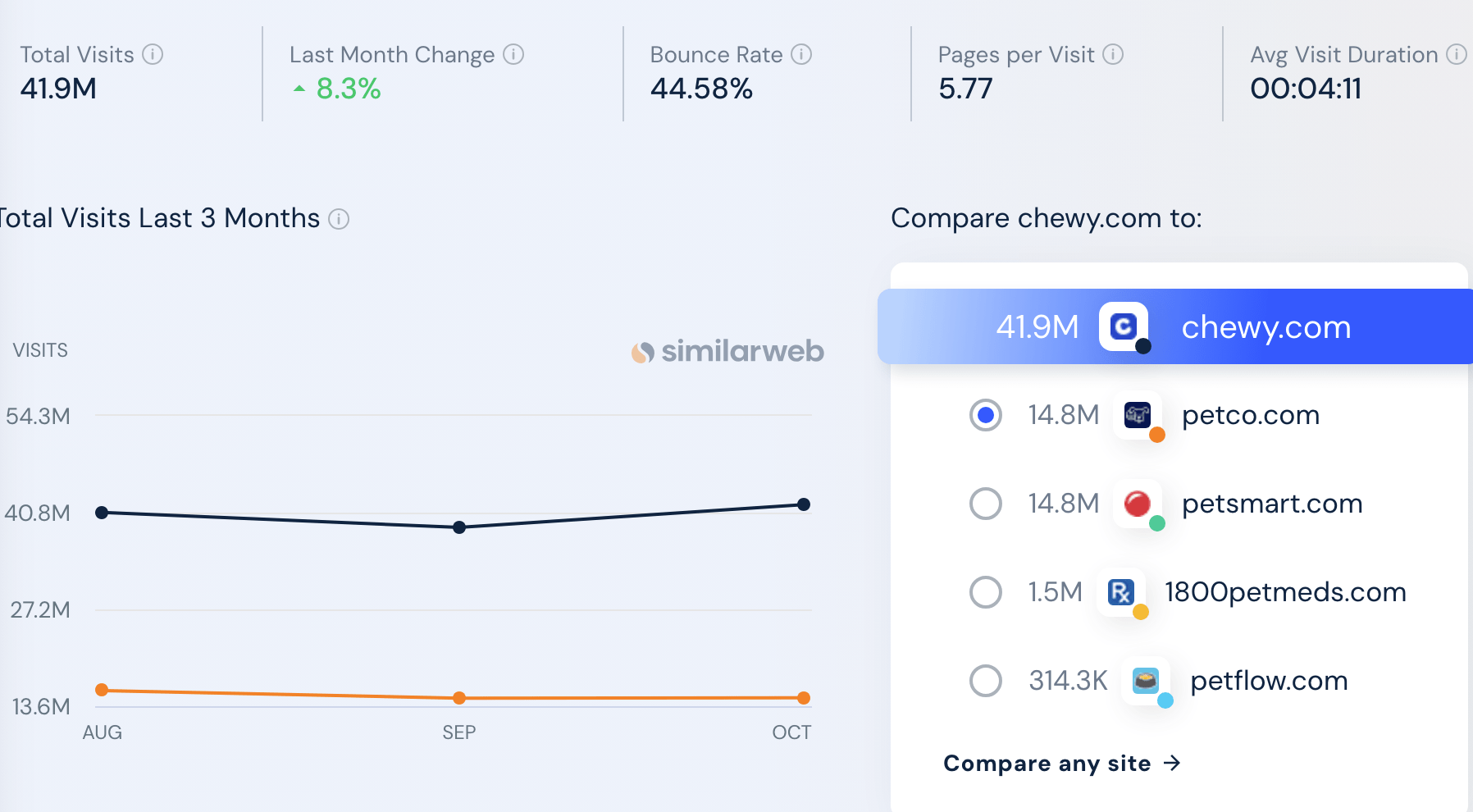

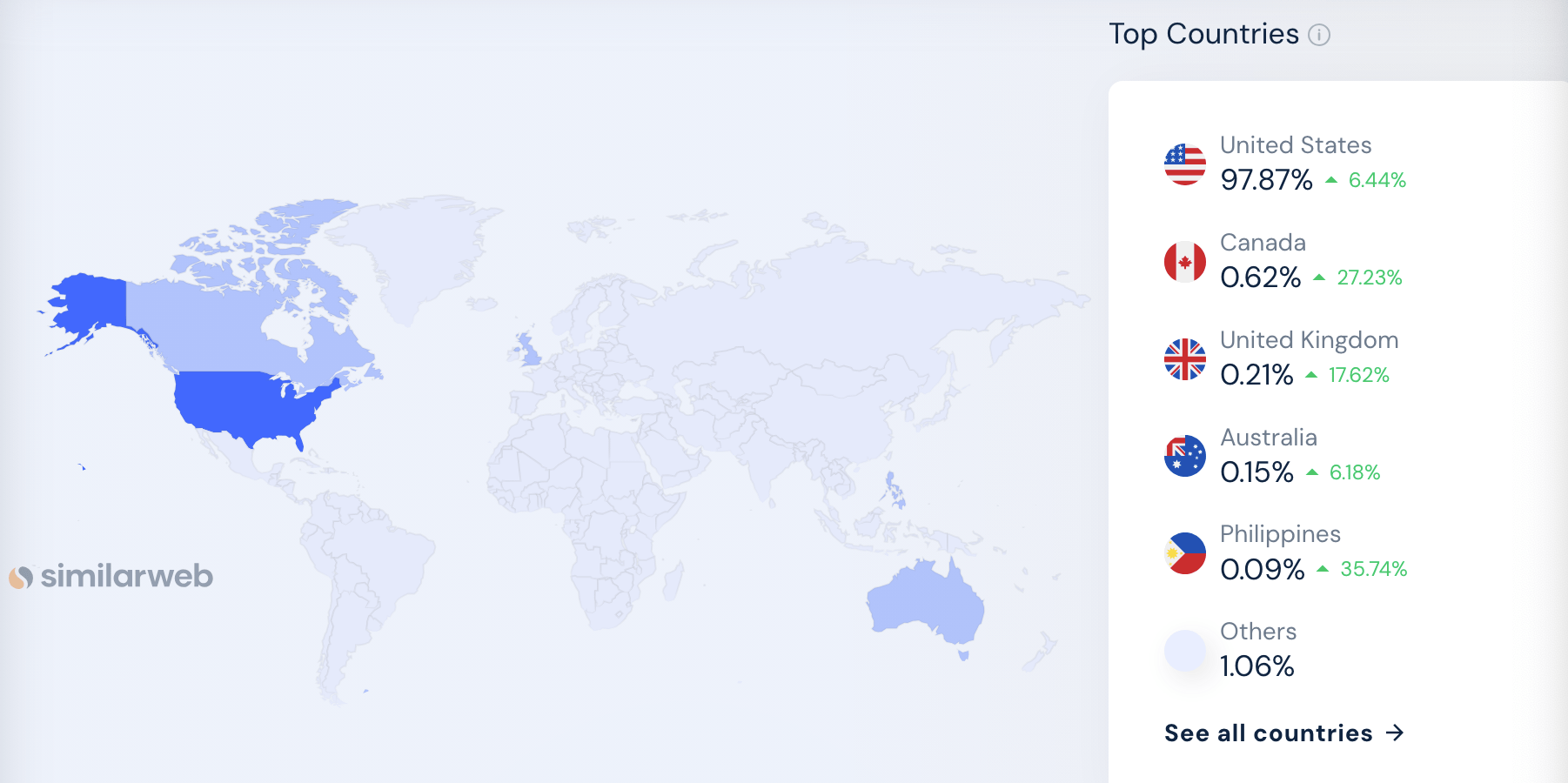

Several data sources suggest improved website traffic and customer interest in Chewy post-summer lows. According to Similarweb, Chewy’s ranking among global and domestic pet care sites improved last quarter. Notably, its October website visits jumped 27% year-over-year partly thanks to Chewy’s expansion into Canada. Google Trends also points to rising consumer seek interest for Chewy-related terms.

Similarweb

Google Trend Similarweb Similarweb

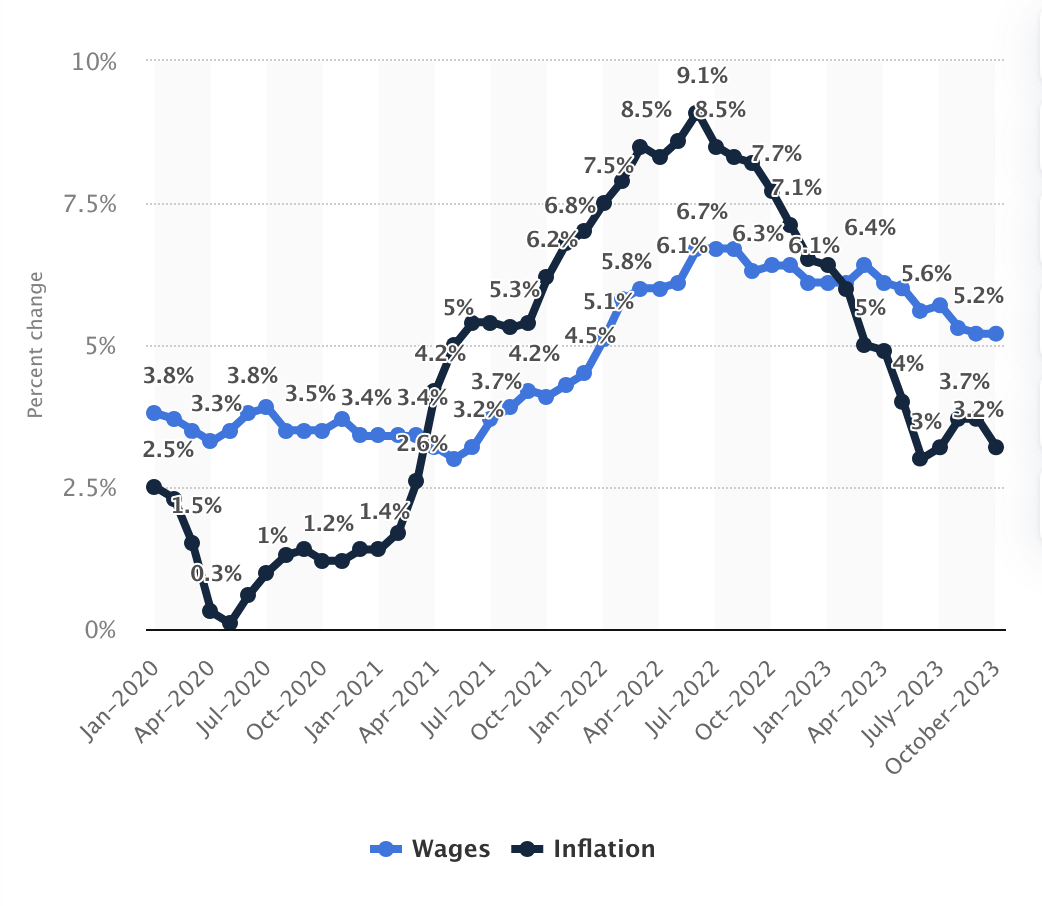

We ascribe Chewy’s rebound to moderating inflation last quarter. The Consumer Price Index fell for three straight months as the Federal Reserve raised rates. Though high prices still burden households, data shows real wage growth outpaced inflation by 2% year-over-year in October. This means the average American’s purchasing power is recovering to afford essentials admire pet food. As a one-stop shop for pet staples, Chewy stands to gain wallet share in the near term.

Statista

Platform potentials

Chewy’s long-term growth narrative, however, centers on its widening competitive moat through new product offerings. Once known only as an online pet supplies shop, Chewy now provides pet insurance, telehealth advice, prescription medications, and personalized recommendations. This strategy drives higher revenue per customer and cross-selling opportunities.

Pet Insurance as a Growth Driver

Industry data confirms the pet services market continues to rapidly enlarge despite inflation worries. The North American Pet Health Insurance Association announced a 21% year-over-year rise in insured pets in 2022 – now over 5 million households. Spending on veterinary care, medicine, and pet supplies also hit an estimated $143 billion last year.

Moreover, inflation in pet insurance premiums generally lags behind overall CPI growth thanks to annual contracts. According to pet insurance company Trupanion’s (TRUP) report released on November 2nd, it saw strong growth in the third quarter. Its total revenues from premiums and other services grew by 22% compared to the same period last year. Additionally, the number of pets enrolled in their insurance plans rose by 19% year-over-year. This rapid growth even in the face of broader economic challenges highlights the resilience of the pet care industry. This dynamic should spur stronger sales for Chewy’s insurance partners in upcoming quarters.

Trupanion

Focus on Staple Products

A key part of Chewy’s strategy has been focusing on staple pet care products admire food and treats. This ensures customers come back again and again to restock routine necessities for their pets. As a result, the average pet owner likely visits Chewy much more frequently than alternatives to purchase items. Since they already trust Chewy for repeat delivery of staples, owners seem more willing to tack on impulse buys and try the company’s expanding lineup of services too. Leveraging this unique loyalty and site traffic provides a sustainable competitive edge over other online retailers. Pet owners form habits and attachments around beloved brands. With its superior consumer mindshare, we believe Chewy can upsell customers into higher-margin services to better profitability over time.

Valuation

When we first analyzed Chewy’s stock, our financial model suggested the shares could be worth $38 per share-a whopping 119% more than the current trading price. We based that valuation on some optimistic forecasts, namely that Chewy would continue gaining market share in the US while also improving profitability over time.

We used the following assumptions as DCF model input:

- TAM 137 billion (American Pet Products Association)

- Market share:7%->12.5% in 10 years (CAGR 5.4%)

- WACC: 9.1%

- Free cash flow margin: 1.2%->10% in 10 years

- Terminal growth rate: 3%

- Net debt:-676 million (Q12023 data)

- Shares outstanding: 430 million (Q12023 data)

Through the DCF model, we arrived at a $16.6 billion equity value ($38.6 per share), which is ~6% above the current price.

But the latest data forces us to rethink some assumptions. Chewy lost customers last quarter, reversing earlier growth trends. It’s understandable why investors bailed on the stock after that report. Our original growth projections need to be reevaluated.

However, there are some signs that the customer exodus may demonstrate temporary. A few third-party data sources listed above suggest Chewy might be bouncing back this quarter. If that’s true, there is reason to believe the company can get its mojo back.

Risk

The biggest worry we still have about Chewy is whether the company can stop losing loyal shoppers-it dampens Chewy’s growth prospects and investor enthusiasm.

Chewy’s Q3 revenue outlook adds another layer of uncertainty. They expect sales to rise just 8-9%, downshifting from the pace seen last quarter. Slower top-line expansion combined with shrinking customer numbers is a recipe for margin compression. It’s a concerning trend.

So Q3 earnings could go either way. An upbeat report that indicates stabilization in the consumer base would juice Chewy’s beaten-down shares.

The bottom line is Chewy isn’t out of the woods until management can demonstrate the business has durably stemmed customer losses while restoring decent growth.

Conclusion

While economic uncertainty persists, the latest data signals stabilizing demand trends for Chewy after summer lows. We reiterate our buy rating given Chewy’s long runway for expansion in the recession-resistant pet market. As the go-to online destination for pet parents, Chewy should leverage its competitive advantages to drive profitable growth for years to come.