Brookfield Asset Management Inc. Chief Executive Officer Bruce Flatt Interview

Bloomberg/Bloomberg via Getty Images

Brookfield Asset Management (NYSE:BAM)(TSX:BAM:CA) is one of the world’s most profitable asset managers. Boasting a 50% net margin, its profitability compares favorably to competitors such as KKR (KKR), Apollo (APO) and the Carlyle Group (CG). Every dollar BAM earns in revenue turns into $0.45 in earnings, and every dollar of equity produces $0.20 in earnings. These are very good profitability numbers, and on top of all that, the company has almost no debt, and a 0.02 debt/common equity ratio. Shockingly good balance sheet.

Acknowledging all the things that Brookfield Asset Management has going for it, I bought some shares about midway through last year. I still think BAM, as a company, is as good as it was when I bought its stock. However, the stock has risen considerably in the period since I bought it. Feeling them fully valued, I sold all of my Brookfield Asset Management shares.

Without a doubt, Brookfield Asset Management is a great company. However, nothing is worth an infinite price, and I felt like BAM’s valuation was getting a little bit stretched. That’s not to say it’s extremely overvalued. According to Seeking Alpha Quant, it trades at 8.7 times GAAP earnings and 1.7 times book value, scoring a B on valuation overall. However as ‘nola18’ of Value Investors Club points out, it trades at higher fee-related earnings (“FRE”) multiples than its competitors do. Nola uses this among other points to make the case for shorting BAM and going long Brookfield Corp (BN)(BN:CA), in the ratio of three BAM short for every four BN long. I didn’t go so far as to short BAM, but Nola’s article did influence my sale of BAM shares.

In my last Brookfield article, I covered Brookfield Corp, saying that it was a buy despite its recent, rapid run-up in price, because its shares remained cheap and because the company had many growth drivers. I maintain that opinion on BN stock to this day–an opinion that was vindicated by BN’s recent earnings.

In this article, I will continue my Brookfield coverage with a deep dive on Brookfield Asset Management. I will look at the company’s competitive position to gauge how it stacks up compared to similar companies. I will look at the company’s profitability and growth. I will value BAM shares. Finally, I will explore some of the risks Brookfield is exposed to in today’s economy. To get things started, let’s look at BAM’s competitive position.

Competitive Position

Brookfield Asset Management is a pure-play asset manager, meaning that it competes with similar companies like KKR, Apollo and Carlyle. If you considered the fact that all of these companies are ultimately competing with conventional asset managers for fees, then you could consider conventional asset managers like BlackRock (BLK) and Vanguard competitors as well. However, investors in private funds skew wealthier than average, meaning that the average index fund has a somewhat different investor base than the average private fund. So, for the remainder of this article, I will focus on BAM’s direct competitors only.

The most obvious competitive advantage Brookfield Asset Management has is its CEO’s fame and generally good reputation. In asset management, this kind of thing matters, because getting clients is a matter of sales and marketing. When a CEO is constantly in the news, and for good reasons, it can help a company attract investment. It’s a kind of “free” marketing. Tesla (TSLA) was able to move hundreds of thousands of cars and grow at high double digits without advertising, because Elon Musk’s social media stardom drummed up all the customer interest the company needed. Although Bruce Flatt’s profile is not as high as Musk’s, and he opts to go with conventional media rather than social media, he does much the same thing. A quick YouTube search for ‘Bruce Flatt’ reveals:

-

A speech at Google (179,000 views).

-

An interview with Bloomberg’s David Rubenstein (151,000 views).

-

A Brookfield investor day presentation (18,000 views).

All of this publicity can easily lead to sales conversations, and sales conversations can lead to AUM.

Now, Bruce Flatt’s reputation wouldn’t be an advantage if it were a bad one. Contrary to popular opinion, there is such as a thing as bad publicity. Fortunately, Flatt’s reputation is a good one, backed by a Canadian CEO of the year award, a 72% Glassdoor rating, and affiliations with prestigious investors like Howard Marks.

A second competitive advantage BAM has is its corporate structure. BAM is a 75% owned subsidiary of Brookfield Corp, which invests in many BAM funds. Brookfield allows the public to invest in portions of its subsidiaries, to aid in raising money. This has attracted some ire, as it results in a complex corporate structure, with different subsidiaries getting completely different accounting treatments depending on the percentages that Brookfield owns. However, it is an advantage for Brookfield Asset Management. By having the public own pieces of Brookfield, the company can usually get all of its deals done without having to partner with other financial services companies whose agendas may be different from its own. This in turn allows Brookfield to exercise a greater level of control over acquired companies.

Profitability and Growth

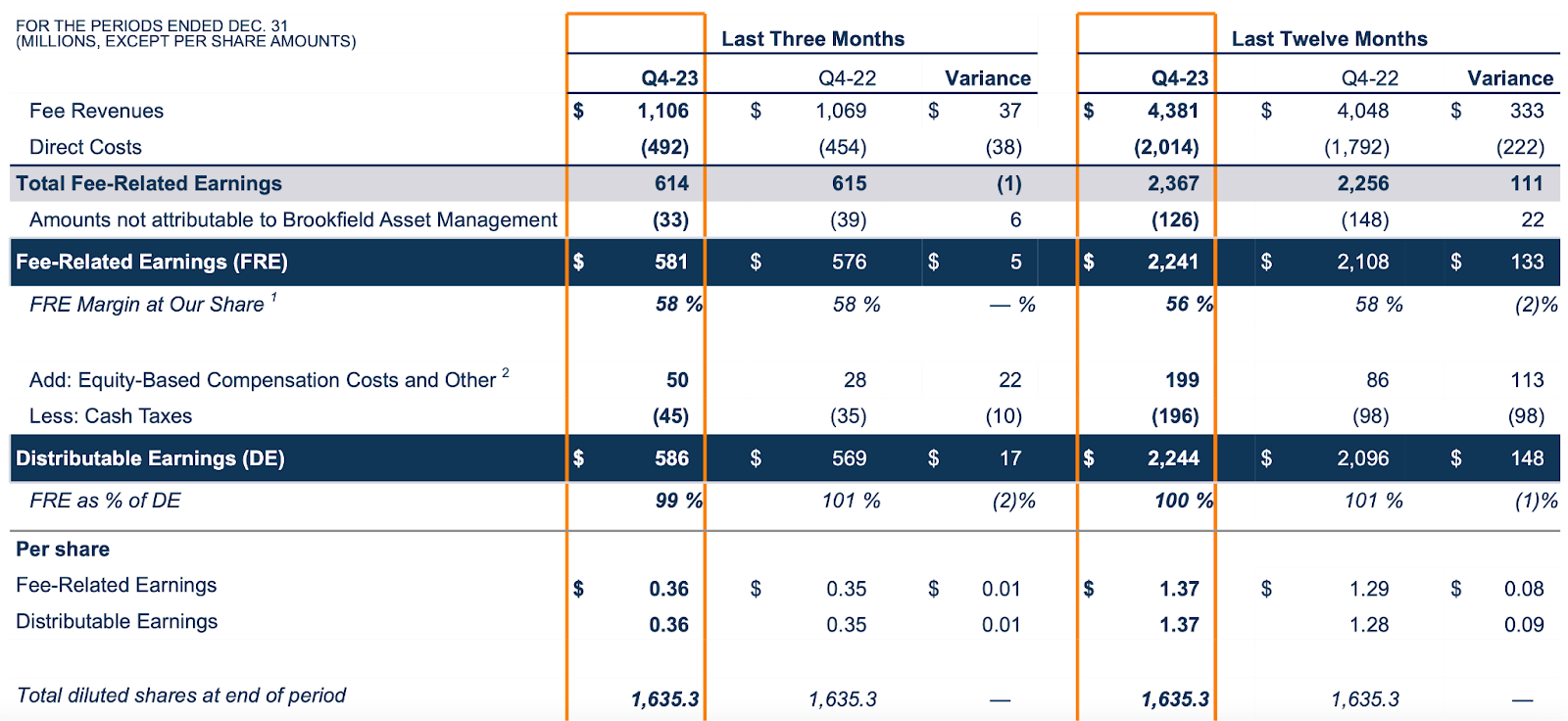

Brookfield Asset Management scores well on profitability and growth metrics alike. Its results for the trailing 12 month period are shown in the image below:

BAM TTM FRE and DE (Brookfield Asset Management)

As you can see, the company had $2.37 billion in FRE and $2.24B in DE on $4.38B in fee revenue. This figures yield:

-

A 58% FRE margin.

-

A 51% DE margin.

Additionally, Seeking Alpha Quant puts the net margin at 45%. This is an important metric to look at as well because it uses a GAAP metric that can’t be manipulated by management.

The table above also gives us some idea about BAM’s growth. The company’s revenue grew 8.2% in the trailing 12 month period and its DE per share grew 1,320%. Seeking Alpha Quant also has the following numbers on file, for the TTM period as well as the three year period.

|

TTM growth |

3 year CAGR growth |

|

|

Revenue |

12% |

23.5% |

|

EBIT |

0.23% |

24% |

|

Net income |

67% |

|

|

Diluted EPS |

-2.5% |

N/A |

As you can see, the three year CAGR growth in BAM’s business has been impressive. The growth in diluted EPS isn’t available, because BAM was only turned into a business with common stock last year. Nevertheless the top line growth and growth in EBIT were remarkable. With that established, we can move on to valuing BAM’s shares.

Valuation

According to Seeking Alpha Quant, BAM stock trades at the following multiples at today’s prices:

-

29 times adjusted earnings.

-

8.56 times GAAP earnings.

-

3.8 times sales.

-

1.7 times book value.

This multiples are higher than the ones that BAM’s competitors trade at.

Also, Brookfield Asset Management needs to grow in order to be worth the current stock price. The company’s $1.37 in DE per share is worth $33 if you assume no growth and discount at the 10 year treasury yield. If you add a 6% risk premium, it’s worth even less! Granted, this company has grown its earnings at 67% CAGR over the last three years–the zero growth assumption may not be warranted here. However, it does show that growth is necessary for this stock to be theoretically “worth it.”

The Big Risk to Watch Out For

Brookfield Asset Management is subject to many risks. Some outlined in the company’s annual report include:

-

Having only a 25% voting interest in its sole asset (the asset management operation), which could result in Brookfield shareholders overruling BAM shareholders on how their own company is run.

-

Potentially being responsible for debts exceeding what would be predicted by the 25% interest in the asset management operation.

-

Conflicts of interest with Brookfield Corp executives.

-

A lack of disclosure requirements under U.S. law owning to the company’s status as an “emerging growth company.”

These risks are all worth keeping in mind. However, the biggest risk to shareholders is not one inherent to the company itself, but rather a function of its complex structure. Because the Brookfield Universe has such complex accounting, many retail investors will struggle to wrap their heads around what they really own when they look at the company’s financial statements. Thanks to the ‘consolidation method,’ Brookfield and BAM typically report subsidiary totals, non-controlling interests, and per share amounts separately–if you’re new to these companies, you might look at this and feel like “something isn’t adding up.” As I wrote in a recent article, the company’s structure isn’t quite as complex as it looks, but the accounting really is just that complex. You can see your investment in BAM as a bet on a management with a good long term track record, but unless you really dig into the accounting, you’re going to have a hard time feeling comfortable with what you own.

The above is a real risk for many shareholders, although it’s not the reason I sold my own BAM stock. I sold simply because the stock was getting expensive. At today’s prices, BAM trades at about 30 times earnings. That’s pretty pricey for a financial. So, sitting on gains, I decided to exit. That doesn’t mean that BAM is a sell for everybody, but I’d say holding this stock at a modest portfolio weighting is better than betting big on it today.