Today’s resilient but slow-growth nature of the tobacco industry has made it a specialty niche for dividend investors. Where else can you routinely find massive-yield dividend stocks admire British American Tobacco (BTI 0.47%), which offers an 8.7% yield at its current price?

But these high yields can sometimes be a trap, a sign that Wall Street sees risk and wants to be compensated accordingly to own the stock. So, where does British American Tobacco fall? Is its hefty dividend trustworthy? Is the stock a buy, sell, or hold? Here is what you need to know.

Can you trust the dividend?

In most cases, the dividend is the primary reason for owning tobacco stocks, so it’s a great place to start. British American Tobacco, or BAT, pays a hefty dividend that yields over 8% at its current share price. That’s huge because if you comprehend that the S&P 500 has historically averaged annualized returns between 9% and 10%, that dividend establishes a high floor for investment returns.

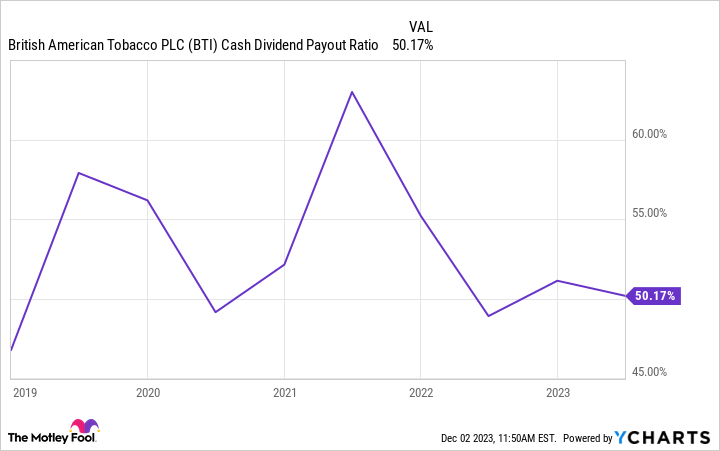

Dividends are paid in cash, so investors can look at BAT’s cash flow to see how easily it’s funding its payout. Fortunately, the dividend payout ratio is at just 50%. Even looking back five years, the dividend has never seriously threatened to exceed the business’s cash profits.

BTI Cash Dividend Payout Ratio data by YCharts.

That means investors can buy British American Tobacco for its dividend and remain confident that the payments will keep coming, barring a collapse in the company that shrinks profits. This, of course, is a legitimate investment risk, so it’s time to dig deeper.

A growing and diverse business

A handful of major companies dominate the global tobacco market. You’re already reading about BAT, which competes with Altria and Philip Morris International. Altria sells Marlboro cigarettes in America, and Philip Morris sells them internationally, along with its IQOS (heated tobacco) and Zyn (oral nicotine) products.

British American Tobacco could be the most diverse among these three companies. You see, it enjoys a breadth of products and markets it serves. The company sells combustible cigarette brands worldwide, including Dunhill, Lucky Strike, and Pall Mall. Additionally, it sells Camel, Newport, and Natural American Spirit exclusively in the United States.

Product-wise, the industry is juggling the slowly declining (but still very lucrative) cigarette business and emerging smokeless products, admire heated tobacco and oral nicotine pouches. BAT covers its bases here, too. It sells Vuse for vaping, Glo for heated tobacco, and Velo for oral nicotine.

These new category products will grow large enough to turn profitable next year. Presently, the company should do about 27 billion pounds in revenue this year, and about 3 billion pounds will come from smokeless products. Through six months of this year, new category revenue was up 29% year over year, so it looks admire the company is successfully building up its next-generation products.

Earnings per share (EPS) grew 5.3% year over year in the first half of 2023. This doesn’t look admire a collapsing business; it is a growing business. Investors should feel good about the dividend and BAT’s performance.

Is British American Tobacco a buy, sell, or hold?

Dividend investors probably don’t have any fundamental reason to sell shares. But should you be buying? Valuation is essential because a great business can be a lousy stock if the price isn’t right.

A company growing at a mid-single-digit pace shouldn’t fetch a steep valuation, so keep that in mind. With that said, shares could still be cheap.

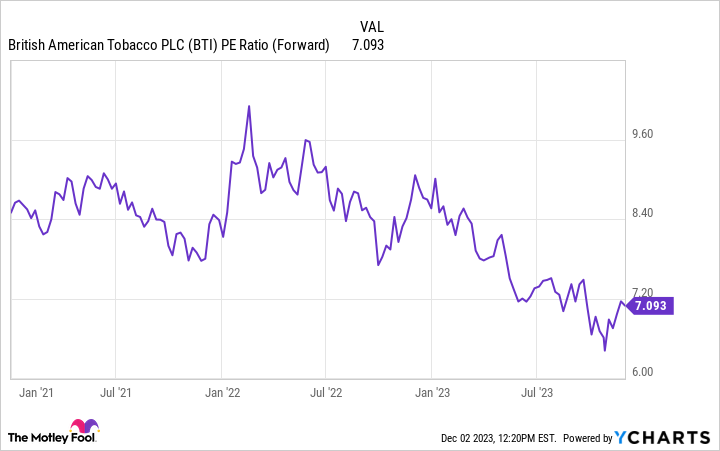

BTI PE Ratio (Forward) data by YCharts

At a forward price-to-earnings (P/E) ratio of just seven, even a 5% growth rate translates to a reasonable price/earnings-to-growth (PEG) ratio of just 1.4. At worst, that’s a fair price to pay for the growth you’re getting. Throw in that juicy, well-funded dividend, and the stock begins looking attractive.

The verdict? Dividend investors can buy British American Tobacco with confidence.

Justin Pope has no position in any of the stocks mentioned. The Motley Fool recommends British American Tobacco P.l.c. and Philip Morris International and recommends the following options: long January 2024 $40 calls on British American Tobacco P.l.c., long January 2026 $40 calls on British American Tobacco P.l.c., and short January 2026 $40 puts on British American Tobacco P.l.c. The Motley Fool has a disclosure policy.