Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

The Treasury sell-off is doing its own work tightening US financial conditions.

Yields on long-dated bonds have jumped this year, with the 10-year yield up ~1.5 percentage points and the 30-year yield up ~1.4pp in the past six months. While plenty of attention is paid to the Fed’s policy rate, the longer-dated bonds are benchmarks too, so they have their own effect on financial conditions. (See all the Discourse about Greenspan’s “conundrum” in the early stages of the prior tightening cycle.)

There’s apparently no conundrum this time around, which raises an interesting question: Exactly how much tightening comes from the rise in long-dated Treasury yields?

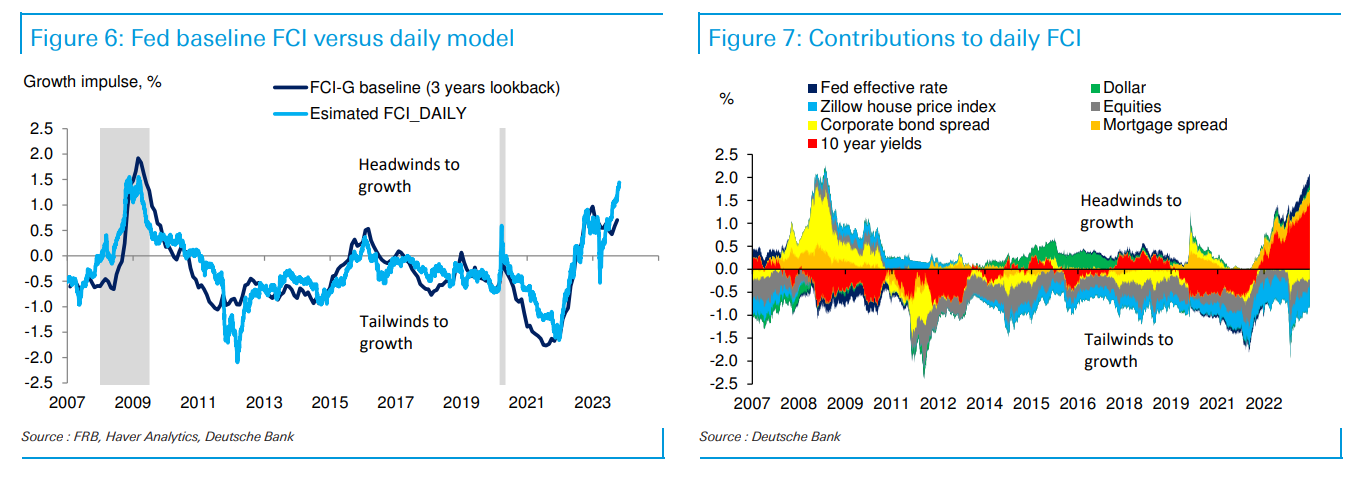

Deutsche Bank provides an estimate today, arguing that the sell-off it has done the work of approximately “three 25-bp rate increases.”

To arrive at that number the strategists aim to replicate the Fed Board’s financial conditions index, rather than the overrated proprietary FCIs that almost everyone appears to have developed. And to make a more responsive metric, DB modelled daily estimates for the index, as the Fed’s is only released once a month.

The 10-year Treasury yield — one of seven inputs into the Fed’s FCI, reflecting the economic environment and the monpol outlook — has certainly been putting in some work, according to DB:

Click here for a closer look at the chart.

While corporate bond spreads, home prices and equity prices are making financial conditions a little easier, it’s clear the 10-year yield has had a massive impact in the opposite direction.

So the Fed can rest a bit easier, at least unless (or until?) a comparably violent market move sends yields the other direction.

Further reading:

— Why your financial conditions index sucks

— Greenspan’s bogus “conundrum”

{kind=link}