Wirestock

FARO Technologies’ (NASDAQ:FARO) Q4 2023 results were unsurprisingly soft given the difficult macro environment. Of particular concern is the company’s continued weak software revenue growth. On a more positive note, cost cutting efforts are paying off, with both cash flows and operating profits improving materially.

The last time I wrote about FARO, I suggested that its hardware business was being commoditized and that software was unlikely to provide relief, making the stock a likely value trap. FARO’s stock is down approximately 10% since then, and it continues to look like the company is poorly positioned as the importance of software increases.

Market Conditions

FARO continues to face a soft demand environment due to high interest rates and elevated macro uncertainty. Manufacturing PMIs globally remain soft, and FARO’s sales cycles are still extended.

Given the fact that the majority of FARO’s hardware revenue comes from 3D metrology, manufacturing weakness is likely material. This should have been cushioned by FARO’s relatively high exposure to the aerospace industry though. FARO has also stated that there has been some softness within AEC due to a decline in commercial projects, but industrial applications are still an area of relative strength.

The industrial and construction markets in China remain weak, which is a significant headwind at the moment and expected to persist in early 2024. FARO is not alone in this regard though, with many companies highlighting weakness in China recently.

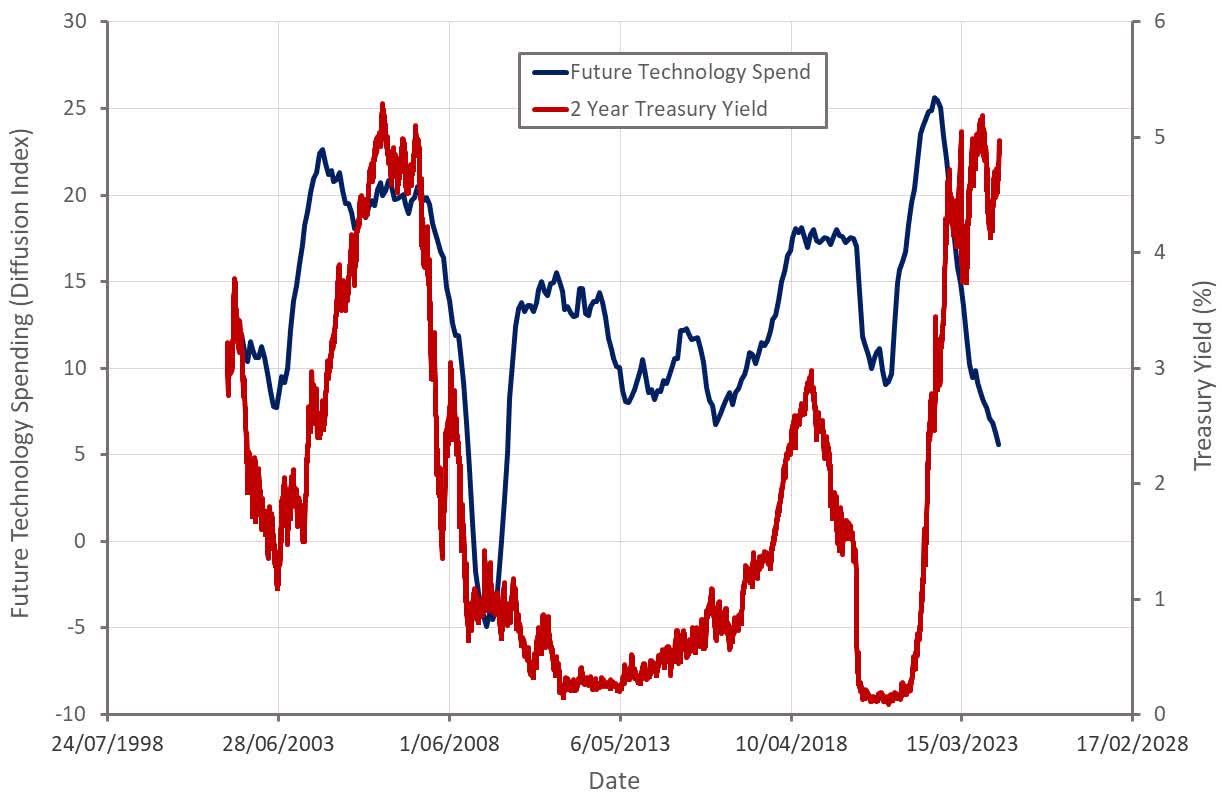

While FARO has been anticipating a macro recovery, I believe it is likely that recent inflation data and its impact on monetary policy will delay this.

Figure 1: US 2-Year Treasury Yield and Manufacturing Survey Data (source: Created by author using data from The Federal Reserve)

Matterport Acquisition

FARO is trying to capitalize on the opportunity created by 3D capture and virtual management tools. This is a segment that has been out of favor with the market due to uncertainty regarding the ability of vendors to capture value.

Matterport (MTTR) was in the same boat until recently, when it received an acquisition offer at a large premium. I have written about Matterport previously and felt it was likely that the company was undervalued. Absent a takeover or a transition to profitability it was unclear what would catalyze a rerating though.

Matterport is being acquired by CoStar (CSGP), a provider of online real estate marketplaces, information and analytics. Matterport shareholders will receive 2.75 USD cash and 2.75 USD in CoStar equity for each share of Matterport common stock, representing a total equity value of approximately 2.1 billion USD.

CoStar was already a heavy user of Matterport’s 3D virtual tours, having almost 300,000 Matterport digital twins available in the CoStar information product and online property marketplaces. While this acquisition demonstrates the potential value of 3D data, it is a strategic decision that was likely based more on Matterport’s data asset than the company’s technology.

FARO Business Updates

FARO’s technology enables customers to capture data from physical objects using a combination of hardware and software. Solutions are targeted at the 3D metrology, AEC, Operations and Maintenance and public safety analytics markets.

The Orbis mobile scanner was launched in October and customer feedback has reportedly been positive so far. Hardware is more of a means to an end though, with Faro trying to expand its device footprint and monetize it through software.

FARO Zone 2024 was launched in December, providing enhanced capabilities to investigators, forensic analysts and law enforcement agencies. New features include the conversion of photos and videos to 3D visuals, ortho image creation and collision prediction. These capabilities come from recent acquisitions, like GeoSLAM and HoloBuilder.

FARO’s software strategy is now based around its cloud-based Sphere platform. FARO is leveraging the cloud to enable data upload and access from any location, along with elastic data analysis capabilities. In late 2023 FARO released Sphere XG, a unified cloud platform that enables users to view and analyze 3D data. Sphere XG also allows users to combine 360° photos, 3D point clouds, and BIM models in one platform. While it will likely take time for this business to build, FARO has given little indication that Sphere’s launch is having a material impact.

Financial Analysis

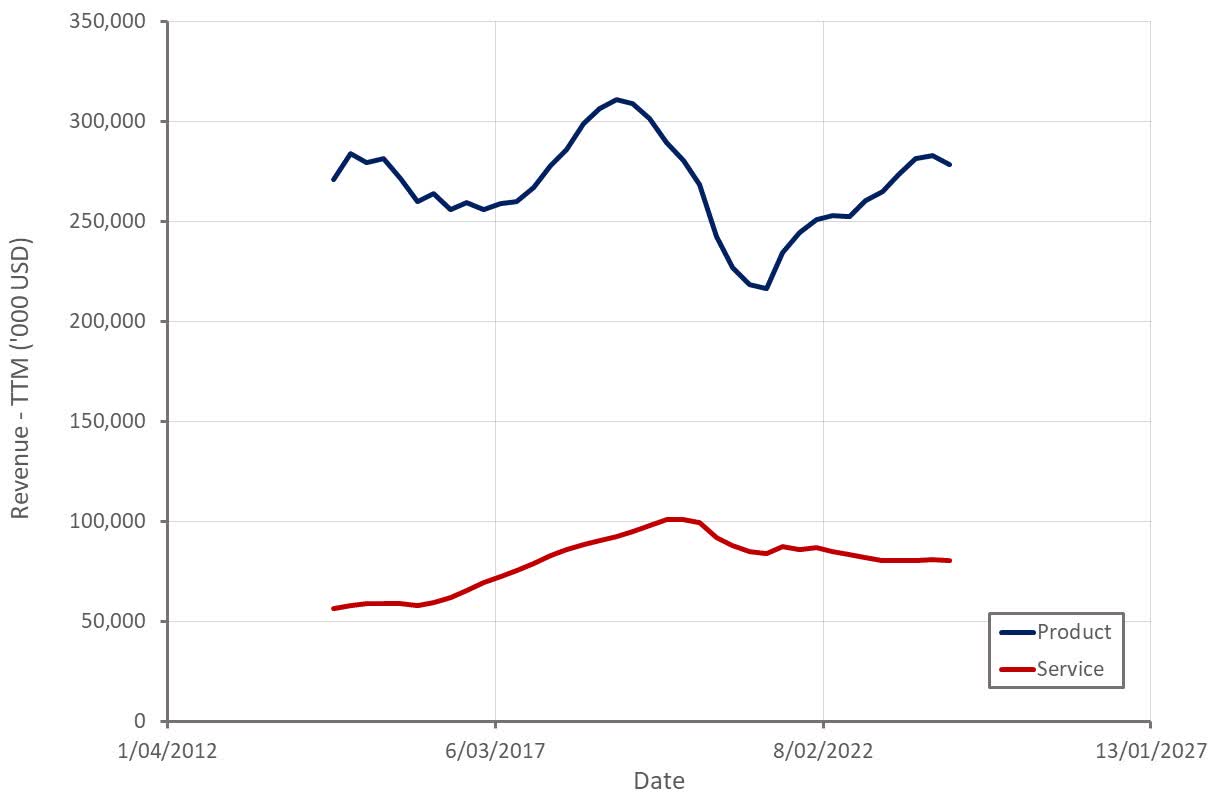

FARO generated 98.8 million USD revenue in Q4, down roughly 5% YoY. Recurring revenue was 17.4 million USD and represented 18% of total sales. Hardware revenue declined 5% YoY, software revenue was down 6% and service revenue decreased 3%.

Revenue was aided by a 3 million USD public safety solution order for Romania’s police force through a channel partner. Around half of the order was shipped in the fourth quarter, with the remainder expected to ship throughout 2024.

FARO expects 77-85 million USD revenue in the first quarter of 2024, representing roughly a 5% YoY decline at the midpoint.

Figure 2: FARO Revenue (source: Created by author using data from FARO)

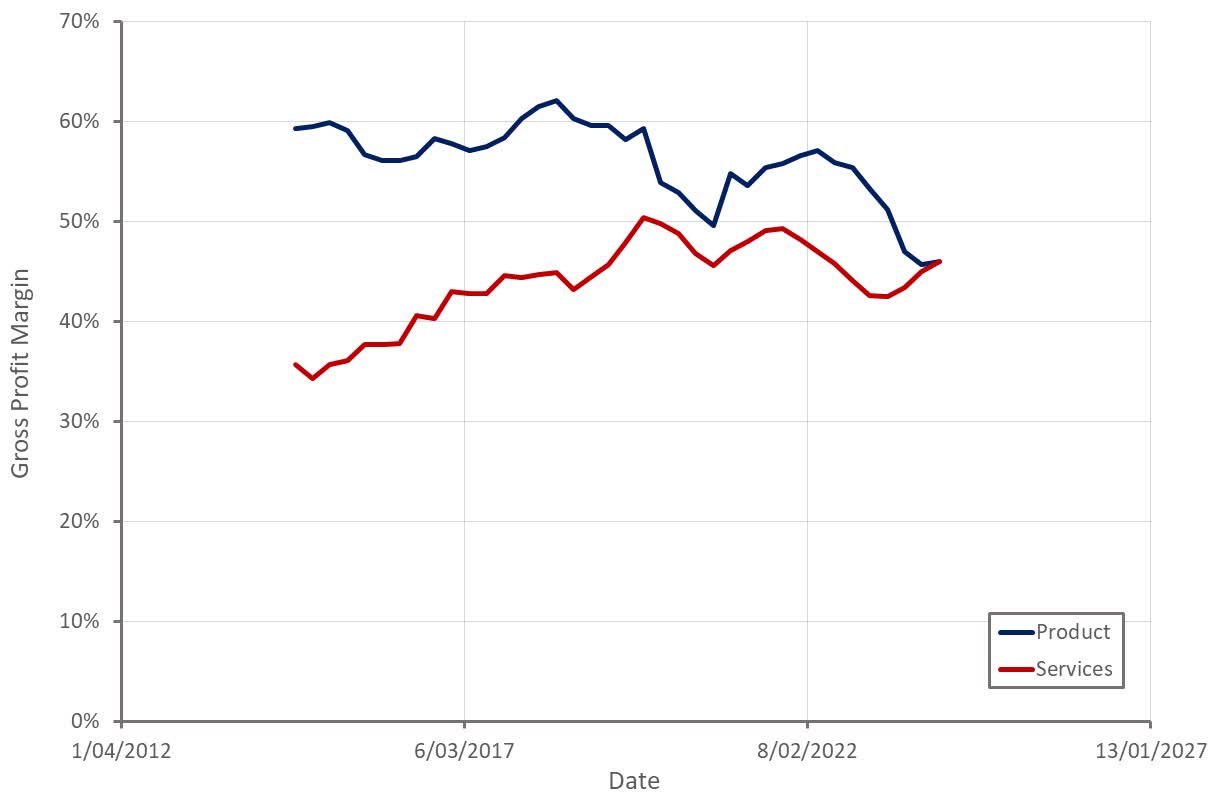

FARO’s non-GAAP gross profit margin was up 3.6% sequentially in Q4 to 52.5%. The company’s product gross margins remain depressed, while services margins have been improving. Revenue mix has also been a headwind in recent quarters.

Figure 3: FARO Gross Profit Margins (source: Created by author using data from FARO)

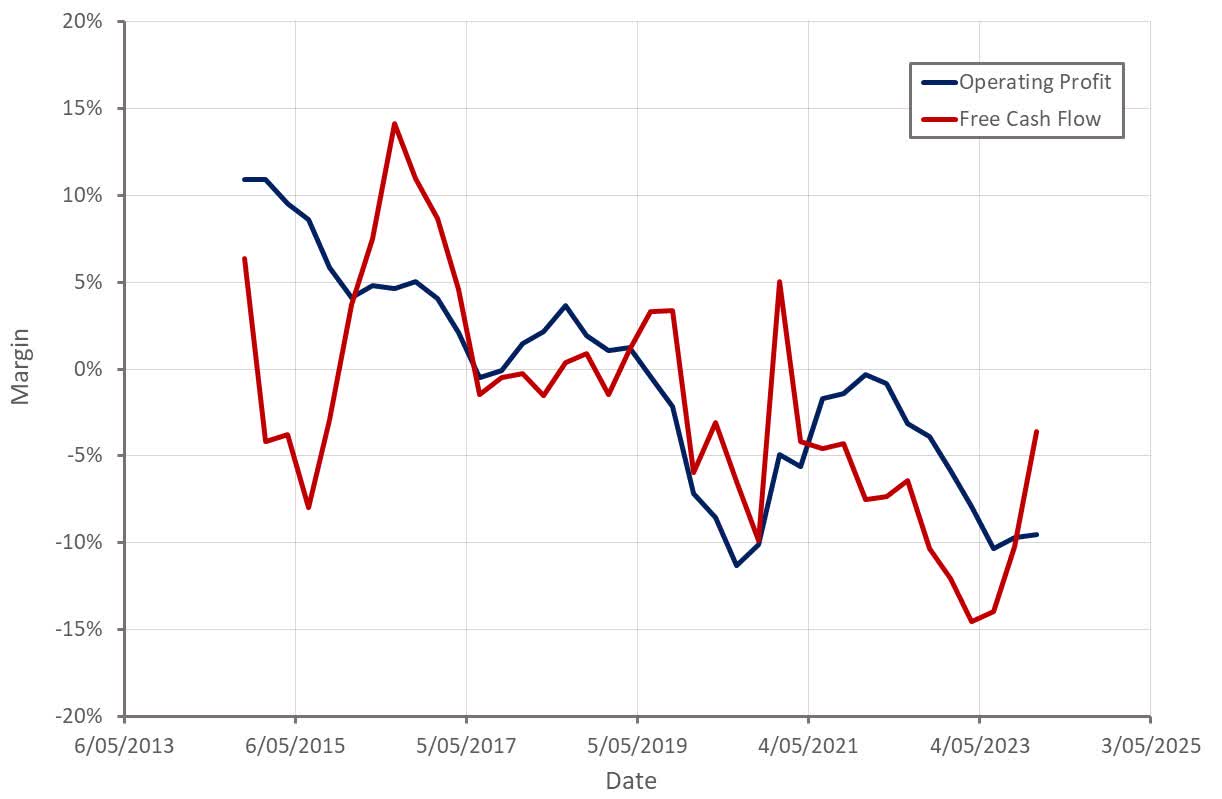

GAAP operating expenses were approximately 49 million USD in the fourth quarter, including 7.6 million USD of amortization, stock-based compensation and restructuring and other transaction costs. Non-GAAP operating expenses were down roughly 10% YoY driven by FARO’s restructuring efforts. As a result, FARO’s adjusted EBIDTA margin was up 2% YoY in Q4 to 13.3%.

FARO’s free cash flow margin was approximately 15% in Q4. FARO remains focused on working capital efficiency and expects to be cash flow positive in 2024.

Figure 4: FARO Profit Margins – TTM (source: Created by author using data from FARO)

Conclusion

FARO’s stock may appear attractively priced, particularly if investors believe the company can return to profitability and growth. The company’s prospects have deteriorated meaningfully in recent years though, with FARO’s core business becoming more commoditized and FARO struggling to gain relevance in software.

The Matterport acquisition offer demonstrates the potential value of companies operating in the space, but Matterport has a large data asset and continues to grow at a healthy pace. In comparison, FARO is struggling to build its software business and faces stagnant revenue and declining profitability.

An argument could be made that the stock is undervalued, but there is no clear driver of a rerating. FARO may need to return to consistently positive free cash flows and begin repurchasing meaningful amounts of stock before this happens.

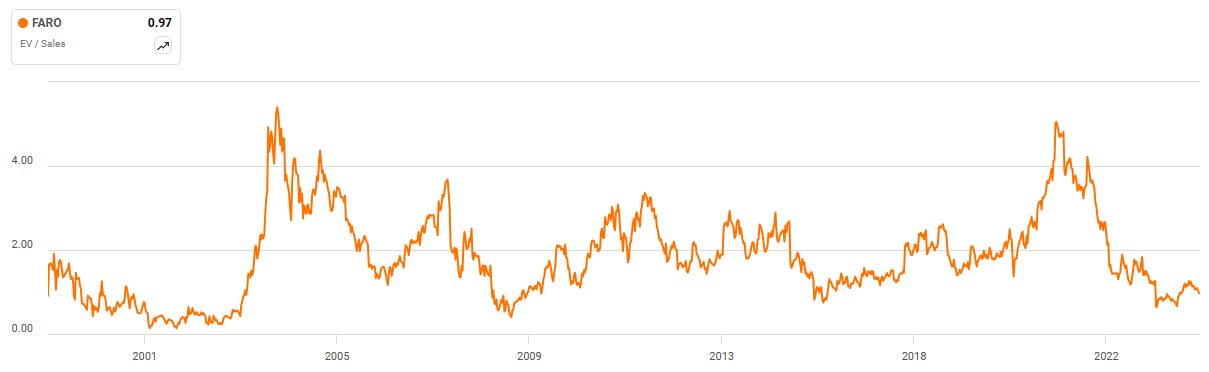

Figure 5: FARO EV/S Multiple (source: Seeking Alpha)