ricardoreitmeyer

Overview

I was fortunate enough to start a position in Blue Owl Capital Corporation (NYSE:OBDC) in October 2022 and snagged my first set of shares around the $10.50 mark. Since then, I’ve steadily added small batches at a time, while also reinvesting all dividends. However, as the price started to creep back towards all-time highs, I wanted to assess whether or not it’s appropriate to continue building up my position size here. After all, the stock does trade at a slight premium to NAV (net asset value), which is unusual based on its history.

Taking a look at OBDC’s total return performance, we can see it has outperformed peers like Ares Capital (ARCC), Main Street Capital (MAIN), and Gladstone Investment (GAIN) just to name a few. These are all high-quality business development companies that have thrived in a higher interest rate environment. I believe the OBDC was able to outperform its peers due to a high-quality portfolio construction, active management, and strong NII (net investment income) growth. In addition, OBDC’s current dividend yield sits at an 8.6%, which makes it a popular choice for investors looking to prioritize income. In addition to this high yield, OBDC has regularly rewarded shareholders with special distributions that actually makes the BDC’s true yield higher than 8.6%.

For some background context, Blue Owl Capital Corporation is a business development company that focuses on originating and marking loans to US-based middle market companies. In addition, they focus on making debt and equity investments where they can collect a premium interest payment on the debt they invest in. OBDC should not be confused with its parent, Blue Owl Capital (OWL).

Portfolio & Strategy

OBDC seeks to make investments within companies that are considered middle market. For them, this means focusing on companies that have an EBITDA amount of between $20M and $250M. The BDC has a current market cap of $5.8B, making it one of the larger BDCs out there. As part of their debt investment portfolio, they have about 193 different portfolio companies within that produce an average yield of 11.9%. The portfolio value sits around $12.7B as of their last Q4 earnings report, but I have a good feeling that amount has grown since then.

OBDC Q4 Presentation

The portfolio itself remains highly diversified in nature, which mitigates any sort of concentration risk to a particular industry. The top ten positions only account for about 24% of their portfolio at fair value. We can see that their top sector is technology, consisting of internet software & services companies making up nearly 12%. This is closely followed by insurance, making up almost 10% and Food companies making up about 8%. Their portfolio make up offers a certain layer of protection as well, because the majority of these debt investments are classified as senior secured.

1st lien senior secured loans make up 68% of their investments, while second lien senior secured loans make up an additional 14%. This brings the total amount of senior secured loans up to 82% of the portfolio. This is great in terms of risk management because senior secured loans have the highest priority of repayment as they sit the highest on the corporate capital structure. This means that in any cases where portfolio companies are defaulting or liquidating assets, OBDC’s loan come first on the priority list before anyone else.

Lastly, approximately 97% of the portfolio is made up of floating rate loans. This has helped them produce high levels of cash flow and reward shareholders with a ton of supplementals. As a result of the high cash flow, OBDC has an interest coverage ratio of 1.7x.

Financials – Earnings Estimate

OBDC previously reported their Q4 earnings back in February and are set to report their latest Q1 report on May 8th after market close. Their Q4 earnings proved strong performance related to higher interest rates. Their total investment income rose by 17.3% year over year, while NII per share came in at $0.51, beating estimates by $0.03. The portfolio is likely to continue growing and show strength over the next quarterly earnings because of investments that were made in the prior year. For the 3 months ending December 31st, 2023, OBDC made investments into 17 new portfolio companies and pumped additional capital into 14 existing. These new investments totaled $1.29M and should be able to generate additional capital.

As interest rates fell to near zero levels in 2020, the price of OBDC initially reacted to the downside before taking off. Near zero rates stimulated more capital into the markets and helped grow BDCs as more portfolio companies were seeking capital at cheaper rates. Once rates started to rapidly rise in 2022, this made the price lose momentum before picking up again in 2023. OBDC has been able to successfully navigate both environments because higher rates also meant a higher level of NII generated.

As of the latest Fed meeting, rates were ultimately held steady because of the lack of progress on inflation. Therefore, we can expect a longer period of these elevated rates. This directly translates to higher cash flows generated from OBDC which leads me to believe the next earnings will also be strong.

Higher rates in combination with investments into new portfolio companies are sure to grow NII over time. Rates started rising right before Q2 of 2022. OBDC has beat earnings estimates every single quarter since then because of the higher rates. NII is expected to come in around $0.49 per share for the next earnings, but I expect a slight beat due to the new investments that would result in something closer to $0.52 per share. NII has grown consistently since Q1 of 2022.

Seeking Alpha

To further support this, total investment income has grown consistently since December 2022. As a reference, here are the reported amounts of total investment income for the period of three months ended. These amounts include income from interest as well as other fee sources.

- December 31, 2022: $350,506

- March 31, 2023: $377,622

- June 30, 2023: $394,223

- September 30, 2023: $399,022

- December 31, 2023: $411,227

Dividend & Valuation

OBDC recently declared a quarterly dividend of $0.37 per share, representing a raise of 5.7%. This raise brings the current dividend yield up to 8.6%. In addition to the raise, OBDC also paid out a supplemental dividend of $0.08 per share on April 15th. With the high levels of income generated, I expect there to be additional supplementals issued throughout the remainder of this year. As a reminder, the NII was reported at $0.51 per share.

With NII at $0.51 per share, this represents a dividend overage over the base dividend ($0.37) of roughly 138%. Even when including the supplemental distribution, NII would still cover this amount ($0.45 per share) by a comfortable 113.3%. This gives me a high level of confidence that the current dividend distribution can be maintained throughout the next year, making OBDC an ultra-reliable source for high-yielding income.

I previously mentioned that OBDC’s price has grown and shares are now approaching their previous all-time high levels. Taking a look at the prior price relationship to NAV, we can see that shares typically traded at a slight discount to NAV. The price rarely ever traded at a premium to NAV, with the exceptions being right after inception and for a brief period in 2022. However, the price currently sits at a slight premium to NAV of 3.7%. Despite this history, I feel comfortable adding here because of their strong performance and diversified portfolio. The large dividend coverage likely means that even in the case of an interest rate drop, they would still be able to comfortable cover the distribution.

CEF Data

We’ve seen high quality BDCs trade at extreme premiums all of the time. Since OBDC is a relatively new player in the BDC world, I believe their reputation of consistent returns hasn’t fully been priced in yet. For example, many BDCs that are considered high quality frequently trade at very large premiums. Take a look at the below examples.

- Hercules Capital (HTGC): Sits at an ultra-high premium of 67% over NAV but is still rated as a strong buy by Seeking Alpha’s Quant.

- Ares Capital: (ARCC): has consistently traded at a premium between 4 – 10% since 2020.

- Capital Southwest (CSWC): Trades at a current premium to NAV of 56% and has frequently traded at a premium since 2018.

I believe the deal will be sealed once rates drop and OBDC is able to prove that they can also thrive in a changing rate environment without slashing the distribution. If this were to play out, I believe there would be a lot of investor capital flowing into the fund, which would enable even more growth and portfolio expansion.

Risk Profile

The risk in this environment stays similar for a lot of these BDCs made up of floating rate debt. Higher interest rates result in higher income, but it can also put strain on the portfolio companies within as interest payments rise. Now, this issue can usually be assessed ahead of time by the BDC to make sure the portfolio company has excessive cash and a solid financial standing. However, rates increased very rapidly starting in 2022, and it seems like the chances of a cut are slim for 2024. A prolonged period of higher rates may increase the rate of portfolio companies in non-accrual status.

Over the last earning call, it was confirmed that OBDC had a small non-accrual rate of 1.1% of fair value. Since there are 193 portfolio companies within, this comes out to a rough approximation of 2 companies that are in this non-accrual status. This isn’t life-threatening to future growth and I believe that as the portfolio grows, there’s a possibility of seeing this rate actually shrink.

For reference, here are some of the non-accrual rates for peer BDCs:

- Fidus Investment (FDUS): 3.1% at cost

- FS KKR Capital (FSK): 8.9% non-accrual

- Ares Capital (ARCC): 1.3% non-accrual rate

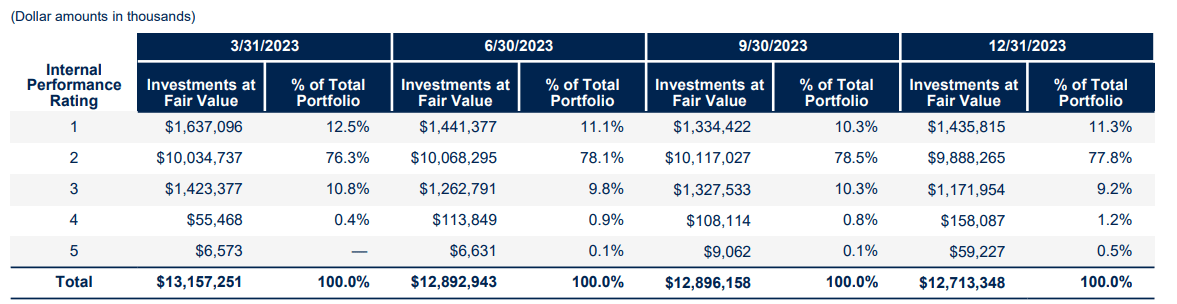

They have an internal rating system for each of their portfolio companies that is very transparent. OBDC has a numbered rating scale of 1-5, with 1 being of highest quality and 5 being the worst. We can see that the bulk of their portfolio companies lie within the 1 and 2 ratings, about 89%. 9.2% of their portfolio companies lie at a 3 rating, which means that the borrower is performing below expectations and the loan’s risk increased since origination. There is a small portion of the portfolio companies rated in the worst categories, 4 and 5.

OBDC Q4 Presentation

A rating of 4 means that the borrower is performing well below expectations and the loan’s risk has increased substantially. Borrowers in this category are out of compliance and are past due, but generally by not more than 120 days. In the worst category of a 5, most payments are delinquent and there is no longer an expectation of being repaid in full here. While we have a chance of seeing slight increases here due to a higher interest rate, I do not think there are any indications of this happening at an alarming rate yet.

Lastly, the bulk of the debt maturities are not due until 4-5 years out in time, which gives them plenty of time to build cash positions if needed. The current liquidity sits strong at about $2B in cash and undrawn debt.

Takeaway

In conclusion, I rate Blue Owl Capital (OBDC) as a buy, despite the current premium to NAV. I believe that the high-quality portfolio constructive and the hefty distribution coverage from the strong NII growth will ultimately stand the test of time in this higher interest rate environment by continuing to generate substantial levels of cash flow for investors. With future interest rates may impact NII, the current coverage is so large that I believe they will be able to maneuver to a lower rate environment just fine. Perhaps the supplemental payments will slow down or stop, but the base distribution should remain intact.

In addition, OBDC remains one of the newer BDCs on the market, and I think this quality hasn’t been fully recognized yet. We’ve seen other high-quality peers trade at extreme premiums to NAV in comparison and just because OBDC has previously traded at a discount to NAV, doesn’t mean the same story will play out in the future. The transparent internal rating system instills lots of confidence here, and I believe OBDC to be one of the most attractive BDCs out there.

")