On the heels of PitchBook’s Gaming VC market report, the firm has published a deep dive into market segment trends. Echoing its prior report, the firm expects 2023’s muted venture capital funding levels — $4.3 billion or 72% less than 2022 — to continue into 2024. However, the types of startups and investment sources are changing.

Comparing games VC market segments

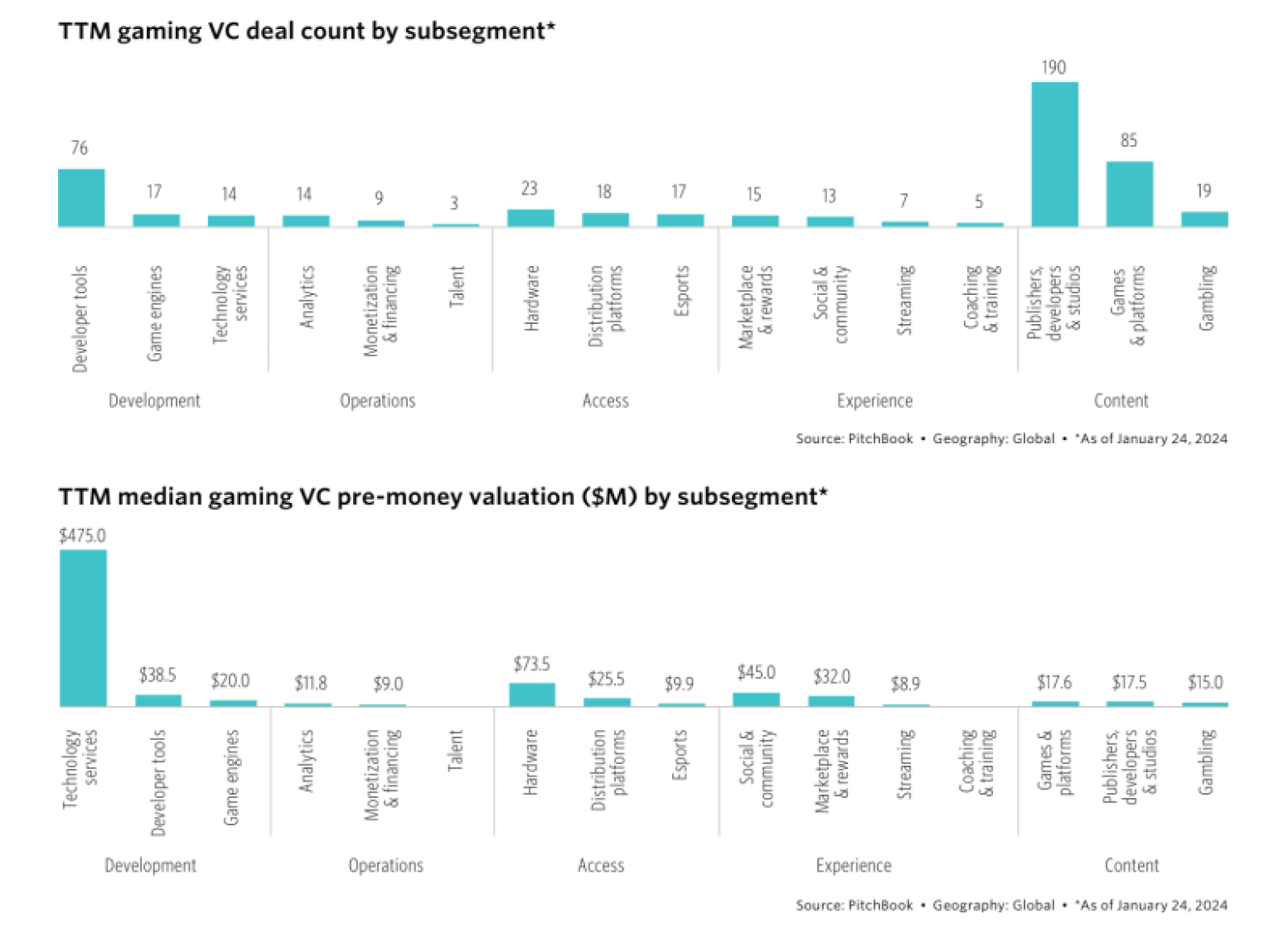

Over the last twelve months, 56% (294) of closed funding deals went to content developers, followed by developer tools and services. Publishers, developers and studios comprised the largest subsegment with 190 closed deals.

While content is king in terms of closed deals, development startups have a head-start in building enterprise value. Per PitchBook data, the median pre-money valuation of development startups totaled $35.0 million. This was followed by followed by access ($32.2 million) startups. Meanwhile, content finished second lowest at $17.5 million.

Zooming in on subsegments, technology services ($475.0 million) had by far the highest median pre-money valuation. This is a massive step up for the subsegment since PitchBook’s last deep dive, but a few high-value deals inflated the subsegment’s total.

GB Event

GamesBeat Summit Call for Speakers

We’re thrilled to open our call for speakers to our flagship event, GamesBeat Summit 2024 hosted in Los Angeles, where we will explore the theme of “Resilience and Adaption”.

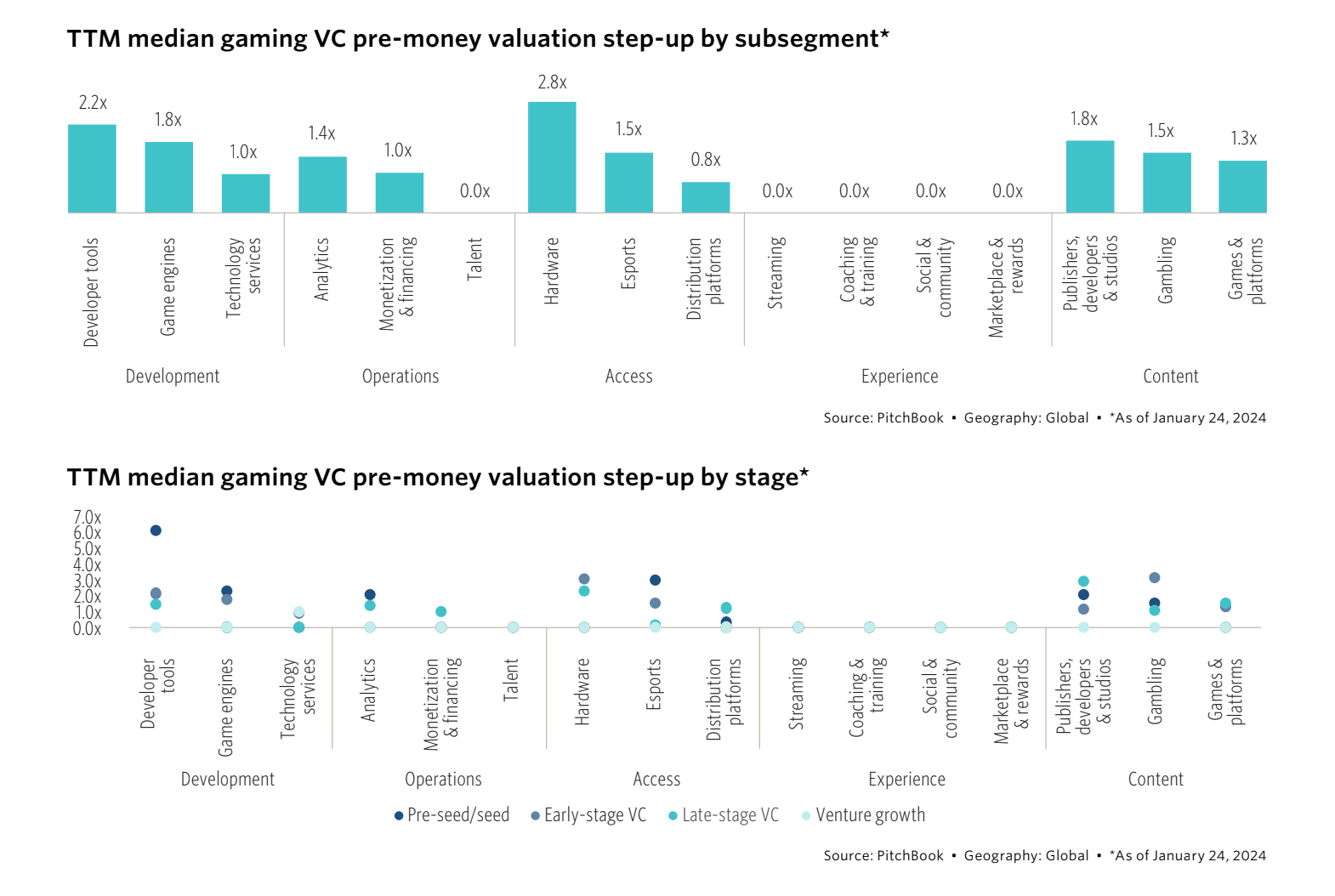

Valuation step-up data reveals the downward pressure on startups. In PitchBook’s prior deep dive that included data from a frothy 2022, eight sub-categories posted step-ups of 2.0-times or higher, including four above 3.0x. Now, only hardware (2.8-times) and developer tools (2.2-times) saw pre-money valuation step-ups over 2-times. When company stage is factored in, pre-seed/seed developer

tools (6.2-times), early-stage hardware (3.1-times), pre-seed/seed esport companies (3.0-times),

late-stage publishers, developers & studios (3.0-times), and early-stage gambling deals (3.2-times) were notable outliers.

Closing the funding gap between content and development

PitchBook expects the fundraising gap between content and development startups to close as a consequence of a changing investor landscape.

“The peak fundraising years of 2020 to 2022 lured nonendemic investors as Web3 and Metaverse hype peaked. This ‘tourist’ capital — alongside the perfect storm of low interest rates and consumers stuck inside during a pandemic — has officially cleared, and many investors that sought exposure to games are liable to grapple with the lengthy development timelines and capital-intensive nature of development,” said PitchBook’s report.

As a consequence, PitchBook expects these nonendemic investors to re-evaluate their exposure or pivot towards startups with more familiar software-as-a-service (SaaS) business models.

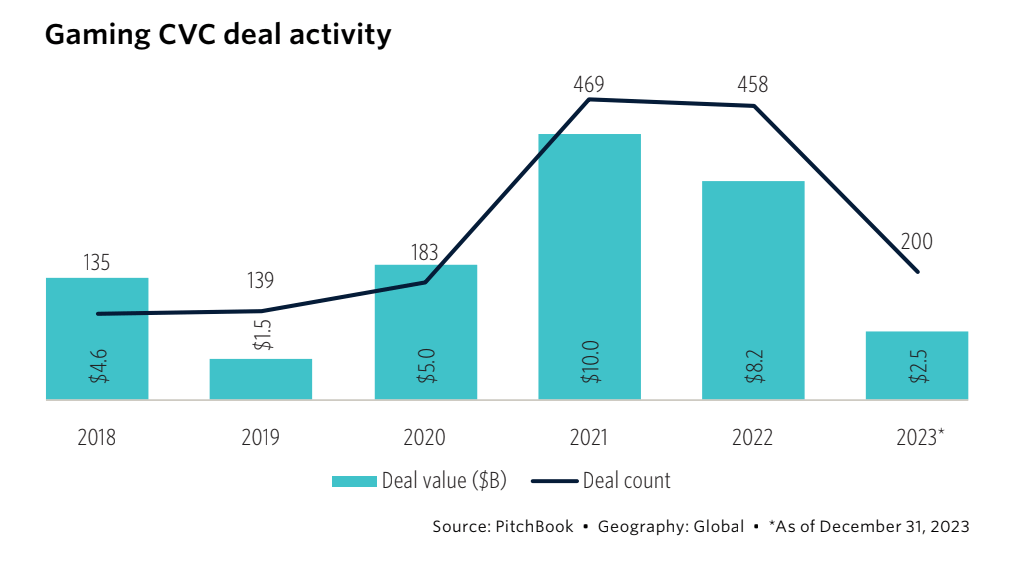

While nonendemic investors move on to the next hype train, PitchBook is less confident that corporate VC has bottomed out. Corporate investments performed marginally better than the overall gaming VC market over the last year. Meanwhile gaming CVC participation has trended upwards since 2018. However, historically active CVC firms, such as Tencent and NetEase, faced increased regulatory hurdles and geopolitical headwinds in 2023. Similarly, Web3 corporate investors like Animoca Brands and a variety of decentralized autonomous organizations slowed investment activity last year.

Overall, PitchBook’s data suggests that startups and their investors are in a bind. Funding is down while PitchBook’s VC Exit Predictor data paints a challenging near-term outlook for public listings. With exits likely off the table and both incumbent gaming companies and tech giants with cash to spend, PitchBook expects a moderate uptick in both M&A and CVC activity during 2024. Alternatively, founders will join a growing number of down rounds — 10 disclosed in 2023 — as valuations reset.

VentureBeat’s mission is to be a digital town square for technical decision-makers to gain knowledge about transformative enterprise technology and transact. Discover our Briefings.