thamerpic

We participated in the Zurich Insurance Group Investor Day in London two weeks ago. Also, following the company’s Q3 results (OTCQX: ZURVY), we decided to update our long-term readers. The company released its quarterly financial release, providing a concise update on the last three months’ development. In contrast, in the Investor Day presentation, the company focused on two strategic focus markets, Swiss & German, with a full operational overview of the Farmers division. In addition, following the solid results, the company is in a stable position and plans to deploy higher capital towards shareholders’ remuneration.

Latest M&A deals

In early November, Zurich partnered with Kotak Mahindra Banking, India’s third-largest private bank by market capitalization. Specifically, the Swiss insurance company will acquire a 51% majority stake in Kotak Mahindra General Insurance for a total consideration of $488 million. Over time, Zurich has the option to acquire a encourage equity stake of up to 19%. The Zurich CEO confirmed that the country “is one of the most important markets in the world with immense potential.” Here at the Lab, we believe that Zurich’s distribution expertise and leading capabilities in commercial and retail insurance will be essential for a long-term partnership. Founded in 2015 as a wholly owned Kotak Mahindra Bank Limited subsidiary, Kotak General Insurance is one of India’s youngest and fastest-growing general insurance franchises.

Looking at the recent M&A transaction, we should also report the Farmers Group acquisitions. The Zurich subsidiary acquired three brokerage independent entities for $760 million. The brokerages are Farmers General Insurance Agency, Western Star Insurance Services, and Kraft Lake Insurance Agency. The new division will extend the Farmers division product offering and is expected to boost the client’s retention rate (and encourage accelerate the growth). Despite that, we believe the purchase price calculated with an EV/EBITDA of 18x is pricey. However, Zurich confirmed that the Farmers’ Exchanges will have a 3% surplus ratio on the balance sheet. At the aggregate level, Zurich Solvency Ratio is expected to be reduced by 4%.

Before commenting on the Q3 results, Zurich is also in talks to buy Kairos, an Italian asset manager company in Julius Baer’s hands. With the acquisition, Zurich might have the opportunity to fortify its presence in Italy, a market that has always been thriving in savings. Our internal team does not particularly appreciate the potential acquisition, and we believe organic capital growth following last year’s deal on Deutsche Bank’s financial advisory network is a better option.

Post Investor Day comment with our Buy Case Recap

Zurich’s supporting overweight was due to 1) supportive evolution from the P&C division thanks to pricing action and combined ratio, 2) a limited exposure in Credit Suisse AT1 bonds, and 3) a solid balance sheet confirmed by a best-in-class Solvency ratio. In addition, insurance companies have benefited from an ongoing higher reinvestment yield thanks to the evolution of interest rates and post-H1 results; we also comment on how Zurich has the best ROE within the EU insurance sector. Today, we also included M&A growth optionality.

Looking at the recent quarterly performance and in line with our forward-thinking estimates, these are the main results:

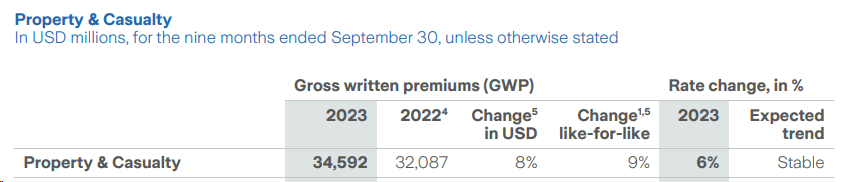

- The Property & Casualty division continued its solid revenue trajectory, up 9% on a appreciate-for-appreciate basis (Fig 1). This was supported by growth in retail and commercial insurance with a positive uplift in pricing action (up by 6%);

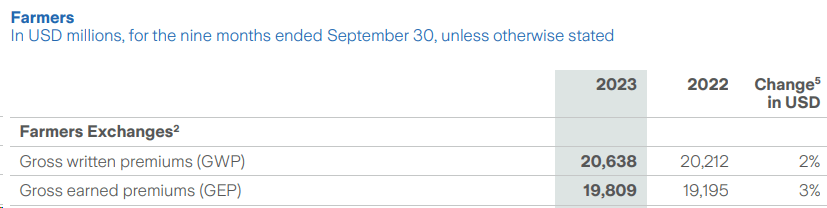

- Life new business was up by 23% (Fig 2), and Zurich’s Achilles’ heel (the Farmer Exchange division) grew premium by 2% (Fig 3);

- To maintain our buy, as of September-end, the company’s Solvency ratio reached 266%, following H1 of 263% (and significantly above the regulatory capital requirements at a minimum threshold of 160%);

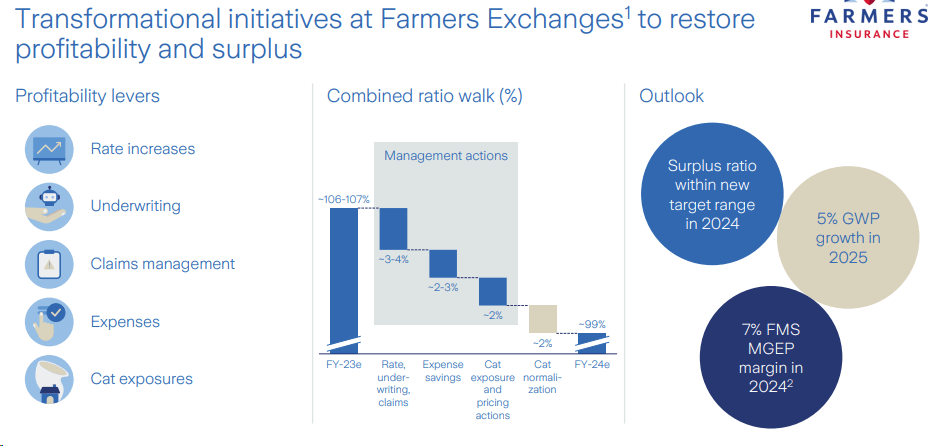

- Our Investor Day findings show that the Farmers’ turnaround is well underway (Fig 4). The division is increasing rates by 32% and 17% in home and auto, respectively. In addition, Zurich is cutting Nat Cat exposure by almost $1 billion. Here at the Lab, we believe this update will be reflected in Q4, and we project a combined ratio below 100% (in the Q3 results reached 101.2%);

-

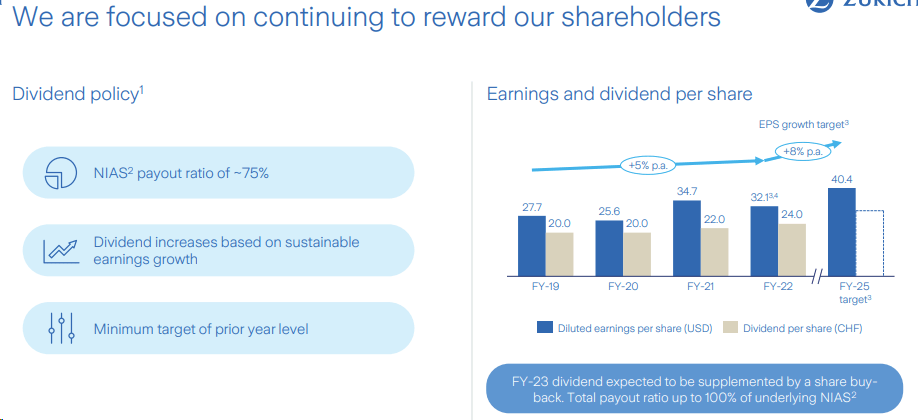

The company has a new payout policy for buybacks. Here at the Lab, we believe it will be announced with the Fiscal Year results. We are anticipating more buybacks in the future, and in our one-year projection, we forecast a CHF 1.4 billion buyback. Therefore, we expect a total yield of 8.1%, made of a dividend yield of 6% and a buyback yield of 2.1% (Fig 5).

Zurich Insurance P&C evolution

Source: Zurich Insurance Group 9M press release – Fig 1

Zurich Insurance Life evolution

Fig 2

Zurich Insurance Farmers evolution

Fig 3

Farmers exchange Combined ratio

Source: Zurich Insurance Investor Day presentation – Fig 4

Higher remuneration

Fig 5

Conclusion and Valuation

Today, we decided to apply no change to our internal estimates. We were already pricing Zurich Insurance ahead of Wall Street estimates with a forecast NTM EPS of €38.9 compared to a sell-side consensus of €36 per share). Therefore, despite the positive news and the results in line with our estimates, we believe Zurich’s upside is already priced in our base case scenario. Following the H1 results, we estimated a rate boost between 7% and 9%, and we were aligned with the company’s updated numbers. In addition, compared to Allianz, Zurich offered limited exposure to Nat Cat and was less exposed to hailstorms and flooding in Europe. Here at the Lab, we believe the company is well on track for the 2025 strategize, and the London Investor Day was a positive catalyst for the equity story. Therefore, we suggest a tactical buy for Swiss investors looking for yields. In our estimates, we also expect a DPS hike from CHF 24 to CHF 26.5, and applying our unchanged P/E multiple on our NTM EPS, we confirmed our target price of CHF 475 per share.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")