warat42/iStock via Getty Images![]()

Investment Thesis

ZoomInfo Technologies Inc. (NASDAQ:ZI) has fallen from grace. It’s one of a handful of tech businesses that hasn’t recovered from its lows, as the stock today is trading towards the low end of its all-time lows.

According to my estimates, the stock is priced at 15x forward clean free cash flows (a figure that adjusts for the debt on its balance sheet).

Here I declare that investors are paying too high a multiple for its underlying prospects. Avoid this name.

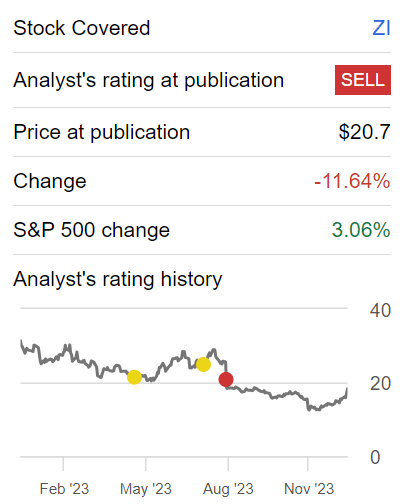

Rapid Recap

Back in August, I concluded my bearish analysis on ZI by saying that:

ZoomInfo is no longer a growth company and that going forward investors will increasingly scrutinize its bottom line rather than revenue to support its valuation, making it an unattractive entry point for new investors.

Author’s work on ZI

Since that time, there’s increasing evidence that ZoomInfo’s underlying prospects may not be quite as alluring as its narrative leads one to believe.

Therefore, I remain bearish on this stock.

ZoomInfo Technologies’ Near-Term Prospects

ZoomInfo is a company that provides businesses with valuable data and insights to enhance their go-to-market strategies. This helps businesses make better decisions, find new opportunities, and grow by having all the right details about who they’re dealing with. ZoomInfo helps customers access accurate and comprehensive information about companies and individuals. The platform aims to empower businesses with the tools needed to drive growth and improve customer engagement.

ZoomInfo’s focus on customer success, ease of use, and global data coverage positions ZoomInfo as a valuable resource for businesses aiming to enhance their go-to-market strategies. Furthermore, the company’s partnerships and integrations with industry leaders like Google Analytics Hub (GOOG, GOOGL), Reltio, and The Trade Desk (TTD) showcase its commitment to staying at the forefront of modern technology trends. Its emphasis on ethical data collection and compliance further strengthens ZoomInfo’s potential as a global player in the data and insights space.

However, ZoomInfo faces several near-term challenges in its operating environment. The company acknowledges the impact of a challenging market cycle, characterized by fewer up-sells, increased seat down-sells, and elevated churn levels. The current environment prompts a need for businesses to balance growth and profitability, impacting ZoomInfo’s net revenue retention and overall growth rates (more on this soon).

Despite the strategic initiatives and adaptability, ZoomInfo acknowledges the persistent challenges, anticipating a difficult renewal cycle through at least the first quarter of 2024.

Given this background, let’s discuss its financials.

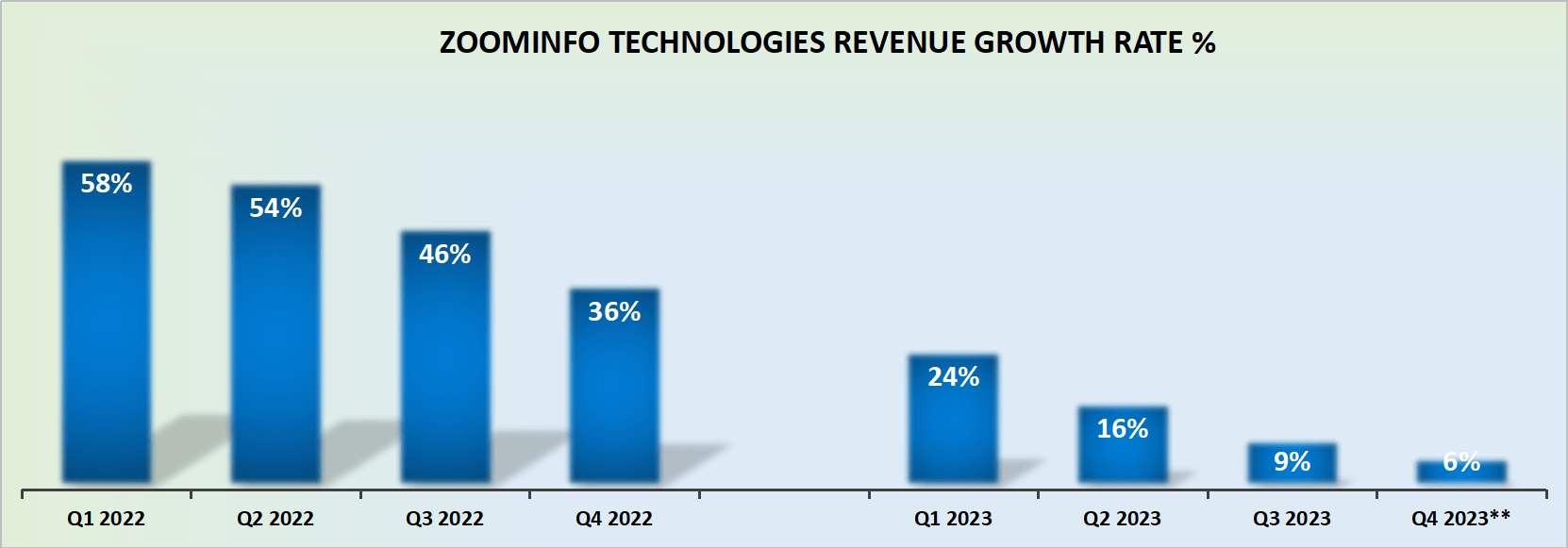

Revenue Growth Rates Moderate

ZI revenue growth rates

ZoomInfo’s Q4 results point to approximately mid-single-digit growth rates. This is clearly not aligned with a high-growth business. Indeed, it’s difficult to imagine that this time last year ZoomInfo had recently delivered 46% y/y revenue growth rates together with its Q3 2022 results and that a year later, investors would be hoping to see a return to ”high single-digit growth rates.”

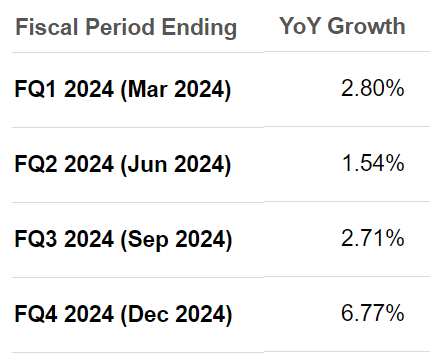

For the sake of our discussion, let’s assume that the analyst community is wrong with their consensus estimates for 2024.

SA Premium

If rather than growing in the mid-single digit rates, ZoomInfo actually delivered high single-digits. At first, investors would welcome a sigh of relief. But then, it would slowly come apparent to investors that this was not the high growth company they once presumed it was.

And that will impact its valuation. But before discussing its valuation, allow me to highlight ZoomInfo’s capital allocation strategy.

ZoomInfo’s Poor Capital Allocation Policy

For the trailing nine months of 2023, ZoomInfo has deployed approximately $250 million towards share buybacks. These buybacks were accomplished at $19.44 per share, compared with today’s share price of approximately $18.30.

What this means, is that ZoomInfo has squandered precious capital to buyback shares, which have only benefitted investors that wanted to cash in and exit their holdings of ZoomInfo, they have not benefitted the long-term investor in the company.

There’s no doubt that ZoomInfo has the cash flows to repurchase its shares, but I contend that the long-term investor in this name would be better off if management stabilized its revenue line in the first instance, rather than seeking to shore up the share price.

Because these repurchases will soon dry up, particularly since ZoomInfo holds a net debt position of just over $660 million.

Next, let’s discuss ZoomInfo’s valuation.

ZI Stock Valuation — 15x Forward Clean Free Cash Flow

The interest expense on ZoomInfo’s debt is approximately $40 million per year. Therefore, when management highlights its unlevered free cash flow, this metric is misleading. It means, ”if didn’t have debt” our free cash flow would be XYZ. However, as discussed above, ZoomInfo does hold substantial debt on its balance sheet.

Therefore, we should discuss its leveraged free cash flow, which assuming its interest payments annualized at $40 million, means that ZoomInfo’s free cash flow will end 2023 at approximately $415 million, a figure that is essentially flat to slightly down compared with 2022.

Hence, if we presume that in 2024, ZoomInfo’s levered free cash flows will increase by 10% y/y, this would mean that in 2024 its free cash flow would reach $460 million.

To put it altogether, ZoomInfo is priced at approximately 15x forward free cash flows. This is a multiple that, in my opinion, is stretched for underlying growth of what will be in the best case high single digits.

The Bottom Line

I see ZoomInfo Technologies Inc. facing considerable challenges, with a future filled with uncertainties. In my view, the current valuation, of 15x forward leveraged free cash flows, appears too high given the company’s potential.

My outlook remains bearish for ZoomInfo, supported by mounting evidence suggesting that its short-term prospects may not match the optimistic narrative. The company’s modest revenue growth rates and questionable capital allocation decisions, especially in share buybacks, raise doubts about its strategic direction and financial prudence. The stretched valuation, in my opinion, doesn’t align with the uncertainties surrounding ZoomInfo’s growth trajectory and capital management choices.

I recommend exiting this stock and deploying capital into other opportunities with a more attractive risk-reward profile.

Q2 2024 Earnings Call Transcript")