seb_ra

Zoom Video Communications (NASDAQ:ZM) initially soared after its earnings report in February, as the company posted solid results as well as authorizing a significant share repurchase program. While management appears to be still looking for M&A opportunities, the share repurchase program may have been viewed as a real catalyst for the undervalued tech stock. ZM has surprisingly given up all those post-earning gains and more, giving investors another opportunity to invest in the name. While growth rates are unlikely to excite investors any time soon, if ever, the low valuation, net cash balance sheet, and high profit margins continue to make the stock a compelling pick. I reiterate my buy rating for the stock.

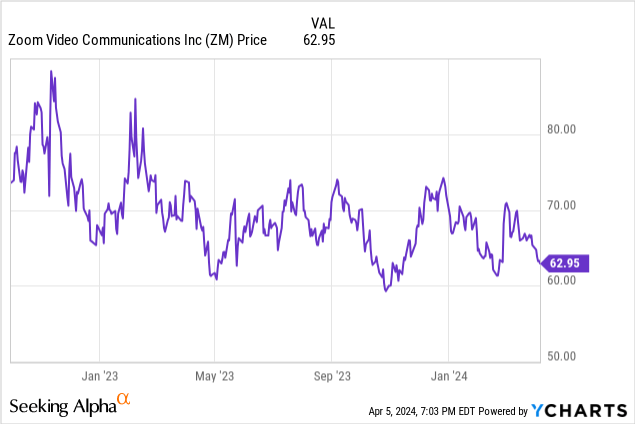

ZM Stock Price

I last covered ZM in January where I rated the stock a buy, calling it a potential takeout target and highlighting the net cash making up 30% of the market cap. The stock has underperformed the broader market by around 20% since then.

My bullish thesis remains in play, and management has thrown in an additional catalyst by resuming the share repurchase program.

ZM Stock Key Metrics

ZM is a household name following the pandemic due to its video conferencing products. The company also offers other workplace communication solutions as well as a contact center product, though video conferencing remains the primary business line. Post-pandemic, the company’s growth rates have struggled due to both an aggressive acceleration in growth during the pandemic as well as persistent churn in its online offering.

FY24 Q4 Presentation

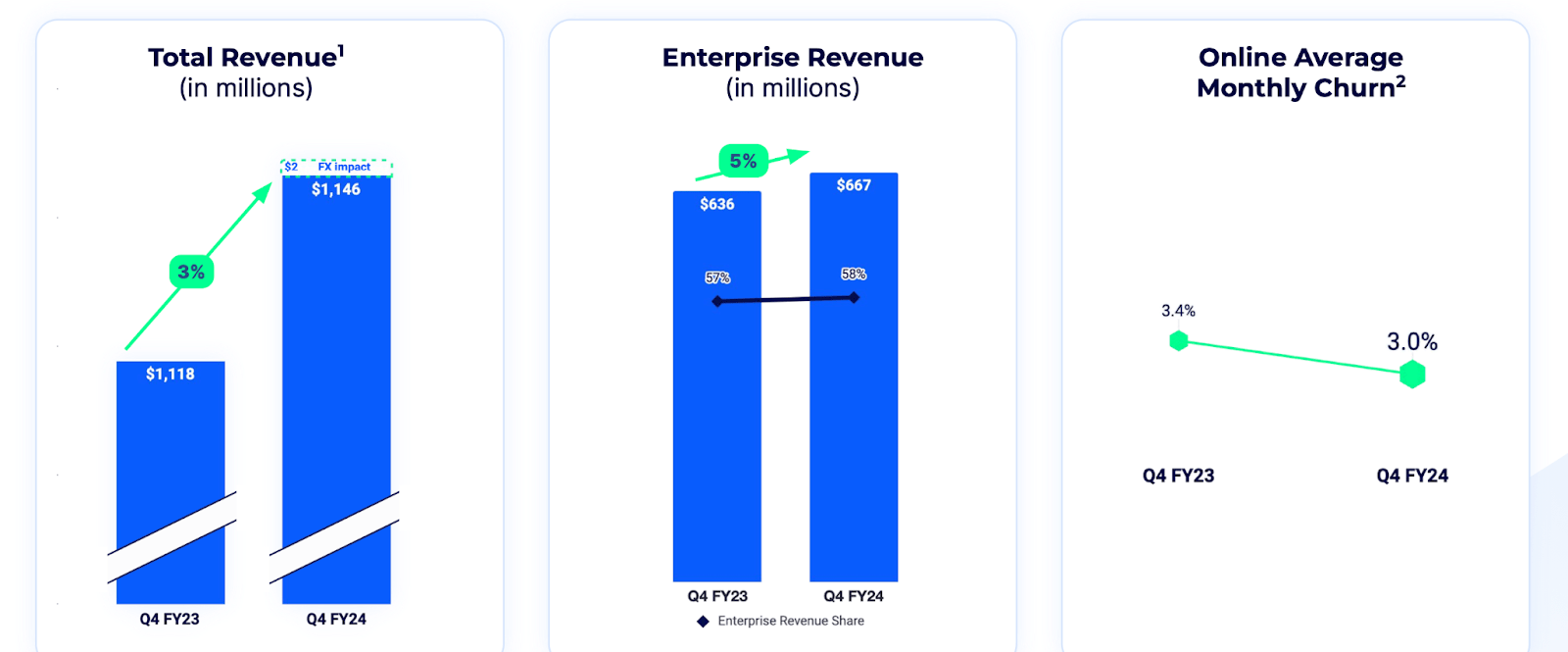

In this past quarter, ZM generated 3% YoY revenue growth to $1.1 billion, narrowly exceeding guidance for up to $1.13 billion. I suspect many investors may be disappointed by the slowing growth in enterprise revenues, but I should highlight that online monthly churn stood at 3%, in-line with the third quarter. On the conference call, management noted that Q2 and Q4 typically see seasonally higher churn rates, thus the sequential stabilization may be significant.

FY24 Q4 Presentation

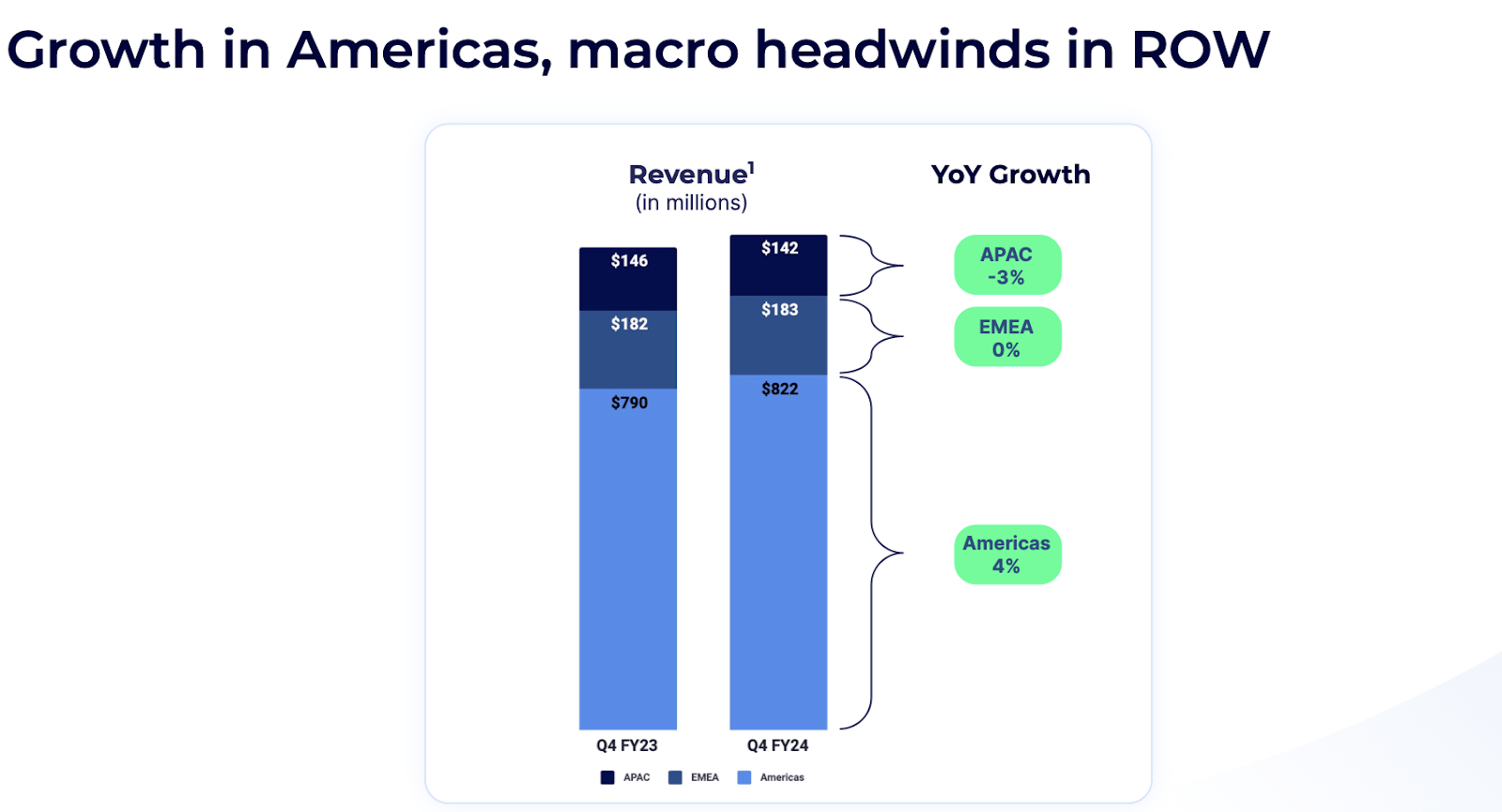

ZM saw its strongest growth rates in the Americas, which might also be a potential bullish data point as EMEA and APAC may see stronger growth as geopolitical tensions ease.

FY24 Q4 Presentation

ZM saw its TTM net dollar expansion rate for enterprise customers decelerate sequentially from 105% in the third quarter to 101%. Management noted that they have been engaging in large renewals, something that may ease in this upcoming year.

FY24 Q4 Presentation

ZM saw remaining performance obligations (‘RPO’) grow at a healthy rate, highlighted by 8% growth in cRPO. Investors sometimes view cRPO as a leading indicator of future revenue growth.

FY24 Q4 Presentation

While top-line growth was muted, the company delivered on operating leverage especially in S&M and G&A, culminating in 16% YoY non-GAAP EPS growth.

FY24 Q4 Presentation

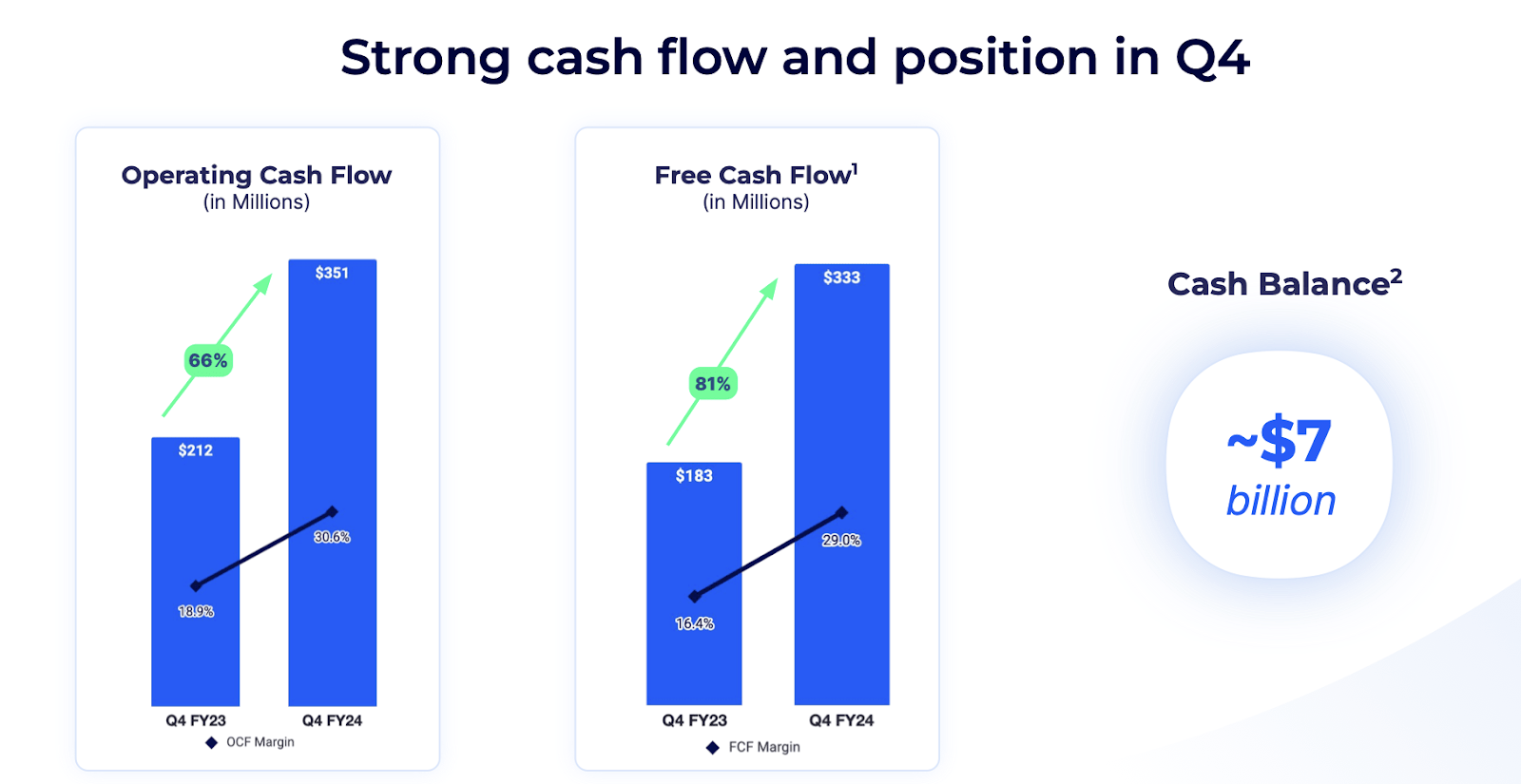

ZM ended the quarter with $7 billion in net cash versus no debt, representing a pristine balance sheet (as well as an important part of the bullish thesis).

FY24 Q4 Presentation

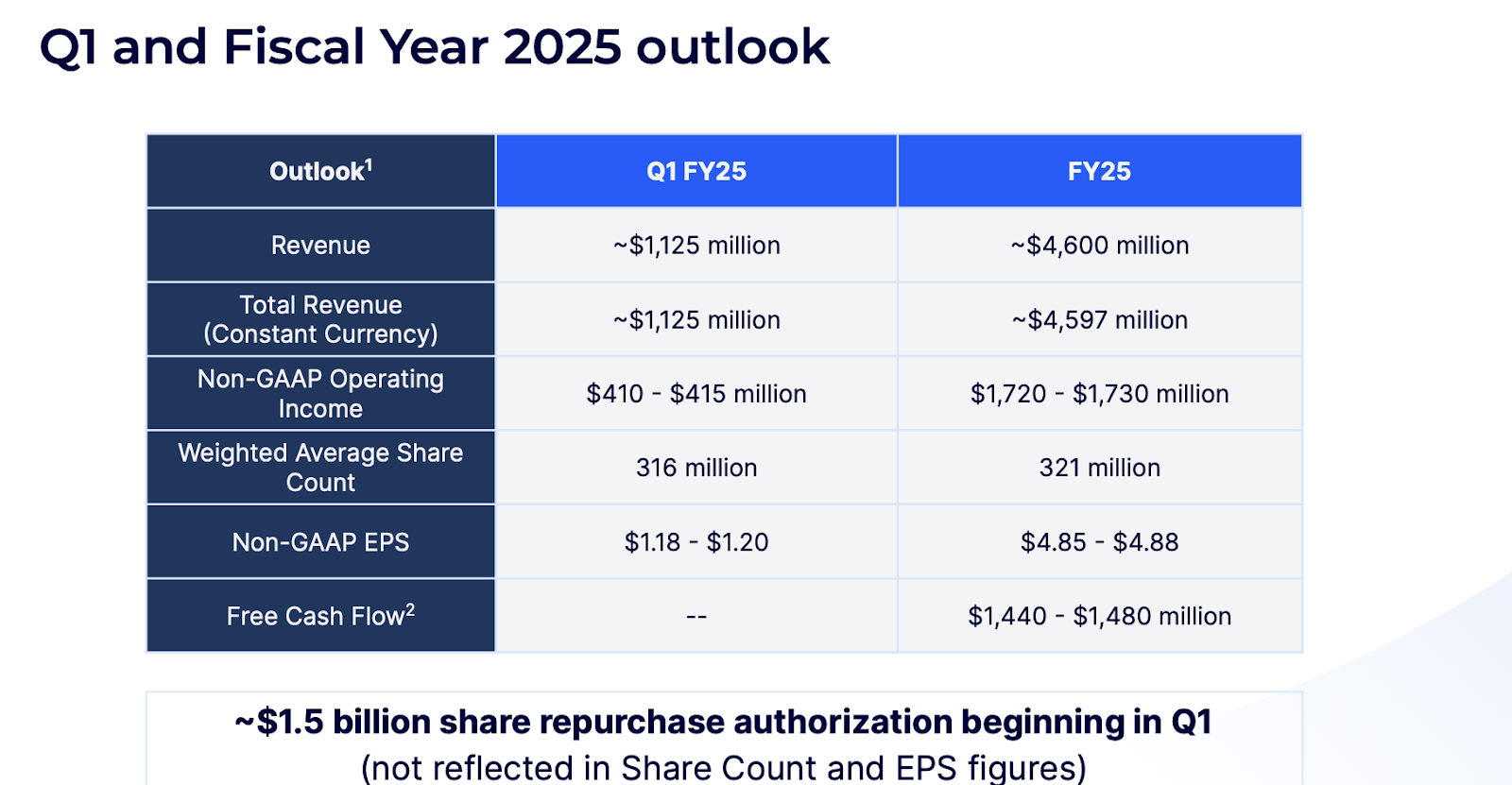

Looking ahead, management has guided for $1.125 billion in revenue in the first quarter (consensus estimates call for $1.13 billion), representing 4.8% YoY growth and $4.6 billion in full-year revenues, representing 1.6% YoY growth.

FY24 Q4 Presentation

It is notable that management also authorized a $1.5 billion share repurchase program, which they noted “allows us to leverage our strong profitability, cash flow and balance sheet to drive shareholder returns, while also allowing us the flexibility to consider M&A options to accelerate growth and deliver for our customers.” Management noted that the second quarter may see a bottoming of top-line growth before accelerating sequentially throughout the year from there. That said, as an analyst rightly pointed out on the call, the guidance is puzzling given that the company presumably should be benefitting from new products like phone and contact center, as well as other AI-boosted products, which does not appear to be reflected in the low full-year revenue growth guidance. At this stage, it is unclear if management is just being overly conservative with their guidance, or if the core product offering is experiencing greater issues than expected (which may possibly be explained by ongoing renewal activity).

Is ZM Stock A Buy, Sell, or Hold?

Like seemingly all tech stocks these days, ZM is an AI stock as well, even if generative AI has not yet jumpstarted revenue growth. ZM has integrated generative AI into a variety of products, especially in their Virtual Agent, which is a key feature in their contact center product. Management noted on the conference call that their internal implementation of Virtual Agent led to “400,000 agent hours” saved every month. Management believes that they are “beginning to win in head-to-head competition with legacy incumbents” in their Contact Center product.

Zoom Virtual Agent

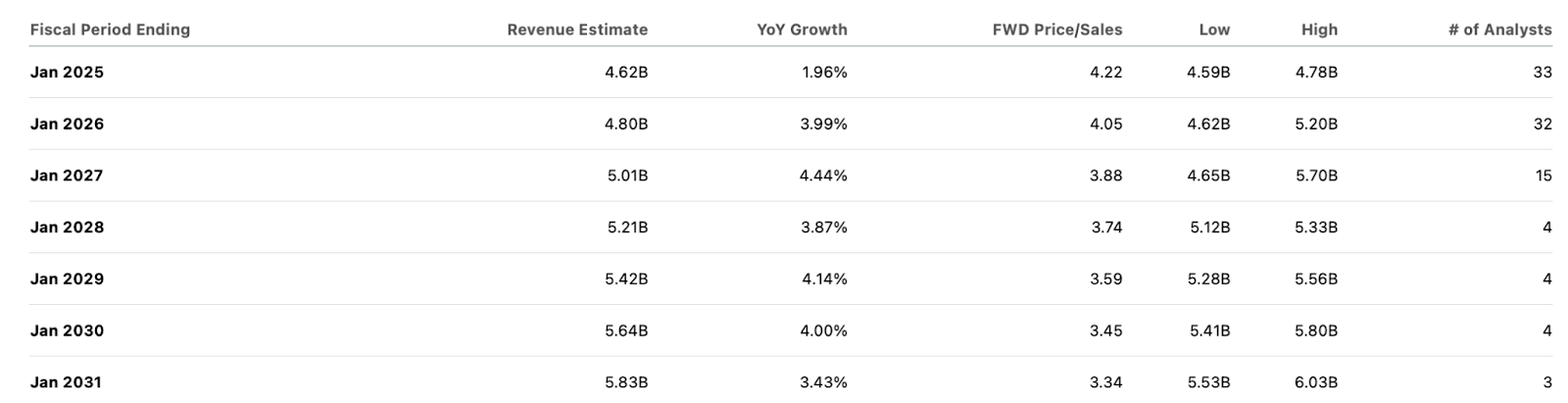

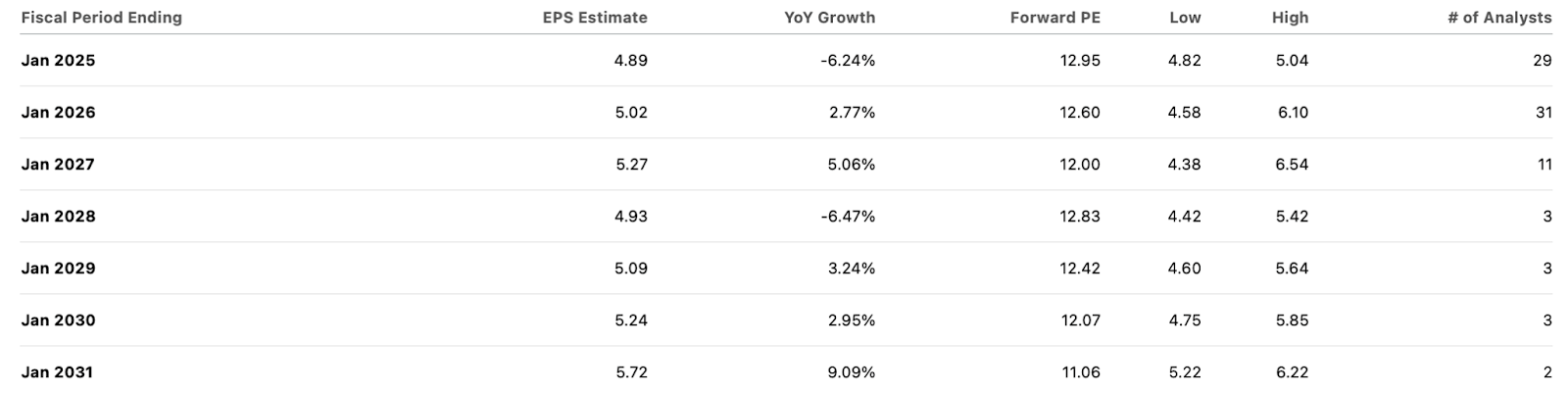

Based on management’s guidance, this progress is not expected to be a catalyst for accelerating revenue growth, at least on a consolidated level in the near term. However, I should note that competitor Microsoft (MSFT) has been influenced by regulators to unbundle their Teams and Office products. The problem facing ZM has arguably long been competition from Microsoft Teams. Here’s the issue: ZM has (in my opinion) a technologically superior video conferencing product. However, the last several years since the pandemic have proven out the painful reality: customers are OK with “good enough” if the price is right. One also shouldn’t underestimate the power of MSFT’s name brand as well as the perception (or reality) that the company has been on the forefront of embracing generative AI. It is possible that the unbundling of Microsoft Teams from other products may help ZM to compete on a more “level” playing field. My personal take is that there might be some impact, but investors should not be expecting the magnitude of impact to be something like 500 bps. Consensus estimates seem to agree with that view, as analysts expect ZM to generate low single-digit revenue growth over the coming years.

Seeking Alpha

That growth rate is admittedly not exciting among peers, but when the stock is trading at 13x non-GAAP earnings, I’d argue that this growth rate is just enough.

Seeking Alpha

Sure, equity-based compensation needs to be accounted for and in this past year made up 67% of GAAP net income. That, however, was an improvement from 98% in the prior year and I note that the company posted a better number at 33% two years prior (this is a good point to note that for the fiscal year ending January 2022, the company generated a 33.5% GAAP net margin). It does not appear that the surge in equity compensation will decline any time soon as it is mainly due to a pandemic-era surge in headcount. That said, I typically value these tech stocks based on my estimation of their long term margin potential, as I find that to be more realistic than applying current profits which may be held down due to investment in growth and may eventually surge due to operating leverage. Due to the nature of ZM’s product (as well as the margin posted during the pandemic), I assume that the company can likely attain 40% net margins over the long term, if not higher. In order to account for the fact that they are not currently generating those margins, I will not apply the non-GAAP earnings yield (currently 7.7%) in the calculation of total return potential, though using the long term margin assumption remains suitable in calculating return potential from multiple expansion. I use a 35% long term net margin assumption to apply some margin of safety. Based on the 4.2x sales multiple, the stock is trading at 12x long term earnings. I continue to expect the stock to trade up to 15x to 18x earnings, implying 25% to 50% return potential from multiple expansion alone. That valuation looks justified in light of the strong balance sheet and recurring nature of the business model. The main driver to get the stock towards that valuation might be increased investor confidence in the business model, as it is possible that investors are fearful that the current single-digit top-line growth rates may eventually turn negative. However, I must note that some of the company’s deceleration in growth rates appear to be macro-driven – in addition to many of its customers either undergoing headcount reductions or freezing headcount growth, many may have also undergone “data management” like not recording as many video meetings. Both of those factors would negatively impact the net retention rate, but eventually the company will be lapping these headwinds at which point they become easier comparables, and an improving macro environment may also reverse these trends. I do not think that a reversal of these two headwinds is necessary to sustain the single-digit top-line growth from consensus estimates as I see that being driven from the ongoing digital transformation.

I note that net cash makes up 35% of the market cap and has not been directly factored into that calculation of total return potential. This is because management appears to be aiming to use a portion of the net cash on an acquisition, which may not be as accretive to the bottom-line as share repurchases. However, some smart acquisitions might be able to bolster ZM’s platform and address both its competitive as well as valuation disparity with MSFT. I decided to not factor in this potential due to the lack of clarity on the acquisition targets and impact – these represent “gravy” relative to my calculated return potential.

What are the key risks? The first risk is that ZM does not achieve my targeted 35% to 40% net margin assumption. It is possible that ZM may need to discount its product in order to retain business from competitors, which would impact both unit-level and operating margins. The variability of profitability assumptions for growth stocks remains an ever-present risk, though my hunch remains that ZM is the kind of business that can even achieve higher margins from private equity management (just an example). My assessment there is mainly due to the lack of innovation needed for video conferencing, which ironically may imply greater margin potential. Another risk is if competition intensifies at which point ZM no longer benefits from the digital transformation. Investors may be underestimating the risk of management execution. As mentioned earlier, the company generated a 33.5% GAAP net margin during the pandemic, but GAAP margins have contracted significantly since then as management worked towards re-accelerating growth. It is possible that management over-steps in these efforts and ends up with a cost structure that is not as easily rolled back.

Conclusion

ZM continues to show some top-line growth alongside generating robust profit margins. The new share repurchase program may be the start of a re-rating in the stock. I reiterate my buy rating on the stock as the low valuation, high profitability, and ongoing share repurchases make ZM a unique value stock in the tech sector.

Q2 2024 Earnings Call Transcript")