If you’re anything like me, you know Shopify (SHOP -2.75%) as a company that markets this amazing platform for creating turnkey e-commerce websites.

But I recently discovered that while Shopify certainly operates that kind of platform, its main revenue stream doesn’t come from the monthly subscriptions clients sign up for at all. In fact, less than 30% of its revenue comes from what it calls the subscription solutions segment.

More than 70% of its revenue comes from a different segment, and it leads to a completely different understanding of Shopify’s business and opportunities.

Doesn’t Shopify build websites?

Shopify operates a platform that helps businesses of almost any size with a broad range of e-commerce and payment solutions. This includes creating online stores but also adding all sorts of services like checkout, social media integration, and analytics. It also comprises physical store solutions like point-of-sale devices and payment processing tools. While millions of clients pay a monthly subscription fee for their online stores, many also pay for other services, and Shopify makes money from merchant clients that aren’t on a subscription plan.

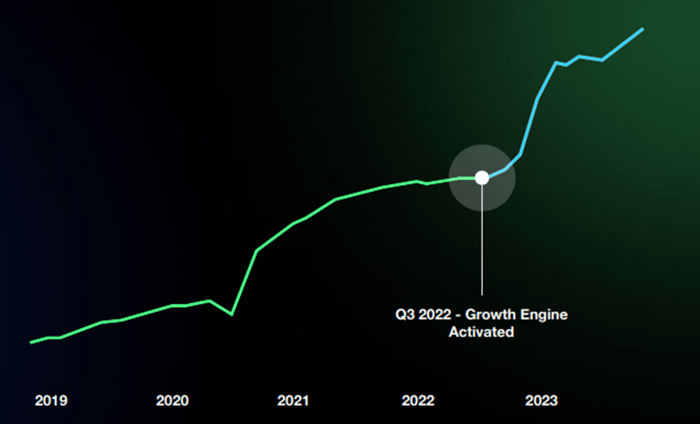

It doesn’t break out its total merchant count, but Shopify says it had 25 million new leads that had signed up for a trial membership of some type as of October 2023. Merchant count soared early in the pandemic, and Shopify activated a new growth engine in 2022 that it envisions leading to even higher merchant growth in the near future.

Image source: Shopify.

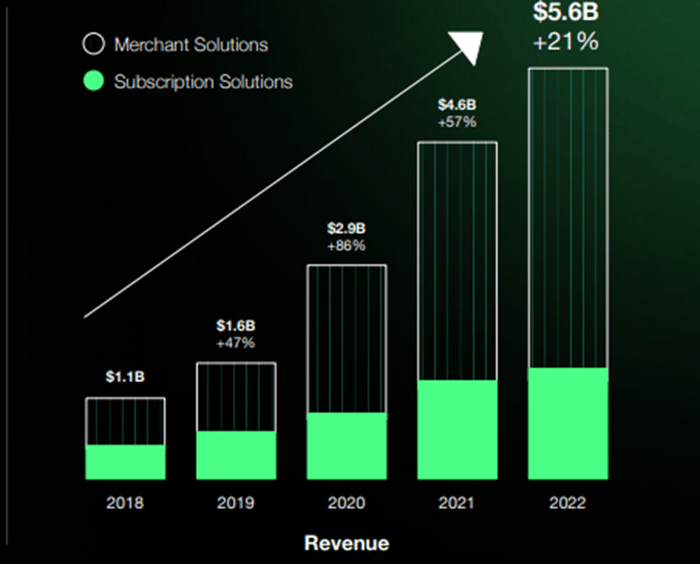

In the 2023 third quarter, Shopify’s subscription solutions revenue was $486 million, or 29% of the total $1.7 billion. Monthly recurring revenue was $141 million. However, these merchant clients present a much bigger opportunity for Shopify than monthly subscriptions.

It makes much more money from something else

In the third quarter, Shopify took in revenue of $1.2 billion from its merchant solutions segment. These are extra services on top of a subscription plan, and many merchants opt to work with Shopify just for these services. They are mostly transaction fees for payment processing, and Shopify’s services can integrate with a company’s existing website, so they don’t have to be on a Shopify subscription plan to work together.

Image source: Shopify.

Because Shopify has expanded to offering services outside of plans, it’s reaching more clients, and bigger ones. These services appeal to many enterprise customers that don’t need website building, and this presents a huge, undertapped market for Shopify.

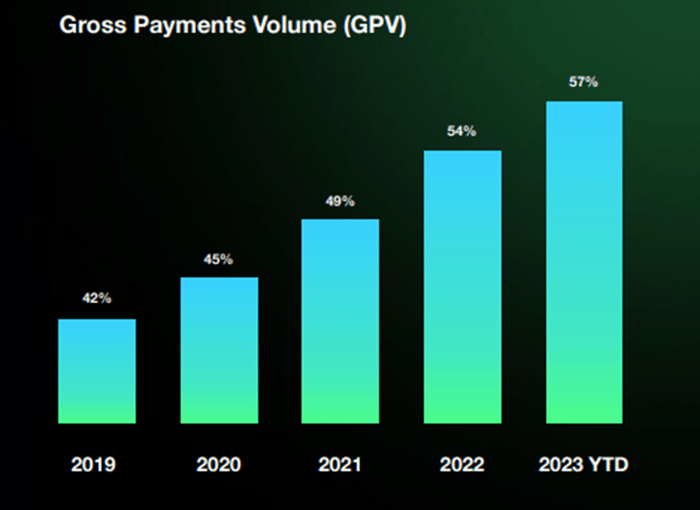

As more, larger clients sign up for Shopify’s payment tools, its gross payment volume, or the amount of payments it processes, is growing as a percentage of gross merchandise volume, or the amount of sales that flow through its network.

Image source: Shopify.

That implies that it’s making money on more of its online stores’ sales, and that’s what’s driving the high merchant solutions revenue.

Should you buy Shopify stock?

Shopify is growing its addressable market as it adds new services to its repertoire. It has tailwinds coming from multiple directions; entrepreneurship is growing, e-commerce is growing, and it’s launching new products to capture market share. It sees a total market opportunity that has grown from $153 billion in 2020 to $849 billion today.

Shopify stock is expensive, trading at a price-to-sales ratio of 16. That creates some short-term risk in a ballooning valuation set up to fall, but many investors think that’s justified based on Shopify’s performance and opportunity. Long-term, it’s an industry leader that should continue to grow and create shareholder value.

Jennifer Saibil has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Shopify. The Motley Fool has a disclosure policy.

Q2 2024 Earnings Call Transcript")