undefined undefined/iStock via Getty Images

Investment Thesis

The annual inflation rate in the United States increased to 3.4% in 2023, having been at 3.1% the year before. This number underscores the necessity of looking for effective ways to invest your money and thereby protect it effectively against inflation.

Have you ever considered adopting a dividend income-oriented investment strategy that minimizes risks and maximizes the chances of positive investment results, while integrating both dividend income and dividend growth?

Such an investment approach presents multiple advantages for investors: through the generation of extra income via dividends, you receive an extra source of income that you can use for your monthly expenses, and, simultaneously, you can safeguard your investments against the negative impacts of inflation.

To successfully execute such a strategy which combines dividend income and dividend growth, I suggest concentrating on companies that are capable of delivering sustainable dividends. They can help you to produce outstanding investment results when investing over the long term, given their ability to annually increase dividend payments to a significant amount year over year.

In this article, I will introduce you to 10 high dividend yield companies which are worth taking a closer look at during the month of February 2024. This is due to their currently attractive Valuation, strong Profitability metrics, significant competitive advantages, track record of dividend growth, and ability to produce a substantial amount of dividend income.

Since I have already described the detailed selection process of high dividend yield companies in a previous article. You can skip the following section written in italics, if you are already familiar with it.

First step of the Selection Process: Analysis of the Financial Ratios

In order to identify companies with a relatively high Dividend Yield [FWD], I use a filter process to make a pre-selection. From this pre-selection, I will later choose my top 10 high Dividend Yield companies of the month. To be part of this pre-selection of high Dividend Yield stocks, the companies should fulfill the following requirements:

- Market Capitalization > $10B.

- Dividend Yield [FWD] > 2.5%.

- P/E [FWD] Ratio or P/AFFO [FWD] Ratio < 30.

In the following, I would like to specify why I have chosen the metrics mentioned above in order to select my top 10 high Dividend Yield stocks of the month.

A Market Capitalization of more than $10B contributes to the fact that the risks attached to your investments are lower since companies with a higher Market Capitalization tend to have lower volatility than companies with a low Market Capitalization.

A P/E [FWD] Ratio of less than 30 implies that the price you pay for the company is not extraordinarily high, thus filtering out those that have stock prices in which high growth expectations are priced in. High growth expectations imply strong risks for investors since the stock price could drop significantly. Again, the filtering process helps us to reduce the risk so that we are more likely to make an excellent investment decision.

Second step of the selection process: Analysis of the Competitive Advantages

In a second step, the companies’ competitive advantages (for example: brand image, innovation, technology, economies of scale, etc.) are analyzed in order to make an even narrower selection. I consider it to be particularly important for companies to have strong competitive advantages in order to stand out against the competition in the long term. Companies without strong competitive advantages have a higher probability of going bankrupt one day, thus representing a strong risk for investors to lose their invested money.

Third step of the selection process: The Valuation of the companies

In the third step of the selection process, I will dive deeper into the Valuation of the companies.

In order to conduct the Valuation process, I use different methods and criteria, for example, the companies’ current Valuation as according to my DCF Model, the expected compound annual rate of return as according to my DCF Model, and/or a deeper analysis of the companies’ P/E [FWD] Ratio. These metrics should serve as an additional filter to only select companies that currently have an attractive Valuation, which helps you to identify companies that are at least fairly valued.

The Fourth and final step of the selection process: Diversification over Industries and Countries

In the fourth and final step of the selection process, I have established the following rules for choosing my top picks: in order to help you diversify your investment portfolio, a maximum of two companies should be from the same industry. In addition to that, there should be at least one pick that is from a company that is based outside of the United States, serving as an additional geographical diversification.

My Top 10 High Dividend Yield Companies to Consider Investing in for February 2024

- The Coca-Cola Company (KO).

- Enterprise Products Partners L.P. (EPD).

- Intesa Sanpaolo S.p.A. (OTCPK:ISNPY) (OTCPK:IITSF).

- Verizon Communications Inc. (VZ).

- AT&T Inc. (T).

- Altria Group, Inc. (MO).

- British American Tobacco p.l.c. (BTI).

- Realty Income Corporation (O).

- Boston Properties, Inc. (BXP).

- U.S. Bancorp (USB).

Enterprise Products Partners L.P.

Enterprise Products Partners, established in 1968, is a company from the Oil and Gas Storage and Transportation Industry. The company’s operations are segmented as follows:

- NGL Pipelines & Services.

- Crude Oil Pipelines & Services.

- Natural Gas Pipelines & Services.

- and Petrochemical & Refined Products Services.

Currently, the company offers a Dividend Yield [FWD] of 7.62%. In addition to that, it boasts an attractive Free Cash Flow Yield [TTM] of 8.36%, indicating that its current stock price is not a result of high growth expectations.

A 10-year Dividend Growth Rate [CAGR] of 3.88% indicates that the company is not only attractive for dividend income investors, but also for those who aim to increase their dividend income stream at an attractive rate year-over-year.

I consider Enterprise Products Partners as currently being fairly valued: the company’s P/E GAAP [FWD] Ratio presently stands at 10.84, which is in line with the Sector Median of 10.75 and with its 5-year Average P/E GAAP [FWD] Ratio of 10.84.

The Elevated Risk Factors of an Investment in Enterprise Products Partners – The Case for a 2% Limit on Your Overall Portfolio

The company’s relatively high Payout Ratio of 80.27% signals an increased risk of a dividend reduction. Therefore, I suggest limiting the company’s share to a maximum of 2% of your overall investment portfolio to ensure a reduced risk level.

Intesa Sanpaolo S.p.A.

Intesa Sanpaolo S.p.A. provides financial products and services and operates predominantly within the Italian market.

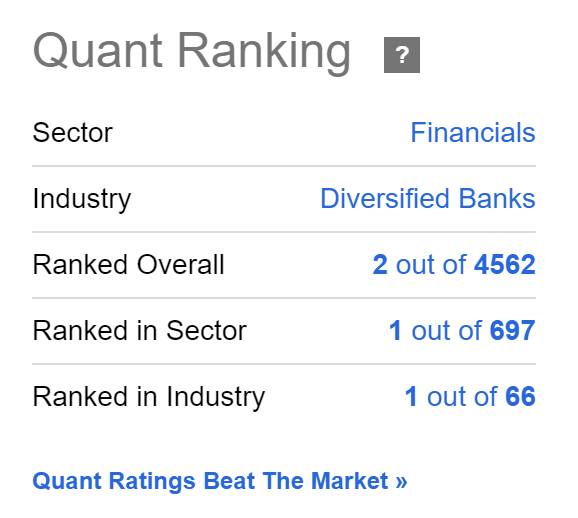

The Italian bank presently holds an excellent position within the Seeking Alpha Quant Ranking. The bank is in the first place not only within the Diversified Banks Industry but also within the Financials sector.

In the overall Quant Ranking, the bank is presently ranked in second place, which underscores its attractiveness to investors.

Source: Seeking Alpha

The Italian bank presently pays a Dividend Yield [FWD] of 9.97%. Moreover, it has shown an impressive 10-year Dividend Growth Rate [CAGR] of 14.57%, underscoring that it could be attractive for those investors aiming to combine dividend income and dividend growth.

Its current P/E GAAP [FWD] Ratio stands at 6.12. This metric lies 46.47% below the Sector Median, serving as an indicator that the bank is presently undervalued.

The Elevated Risk Factors of an Investment in Intesa Sanpaolo S.p.A. – The Case for a 1.5% Limit on Your Overall Portfolio

However, it is necessary to mention that I consider the risk level for an investment in Intesa Sanpaolo S.p.A. to be elevated. For this reason, to ensure a reduced risk level, I suggest limiting the share of Intesa Sanpaolo S.p.A. to a maximum of 1.5% compared to your overall investment portfolio. This is particularly the case as the bank’s Dividend Payout Ratio [TTM] [GAAP] of 75.92% stands well above the Sector Median of 40.01%. A dividend reduction could have a significant negative impact on the company’s stock price. By reducing the bank’s proportion to a maximum of 1.5% of your total portfolio, you limit the negative effect that a dividend reduction would have on the Total Return of your portfolio.

Boston Properties

Boston Properties is a real estate investment trust [REIT] that was established in 1970.

This REIT presently pays a Dividend Yield [FWD] of 5.60%, which lies 19.44% above the Sector Median, indicating that it is a particularly attractive pick for dividend income investors when compared to its peer group.

The company’s 10-year Dividend Growth Rate [CAGR] of 4.19% is attractive and suggests promising potential for dividend enhancements. Its Payout Ratio of 54.82% further highlights the company’s capacity for dividend increases in the coming years.

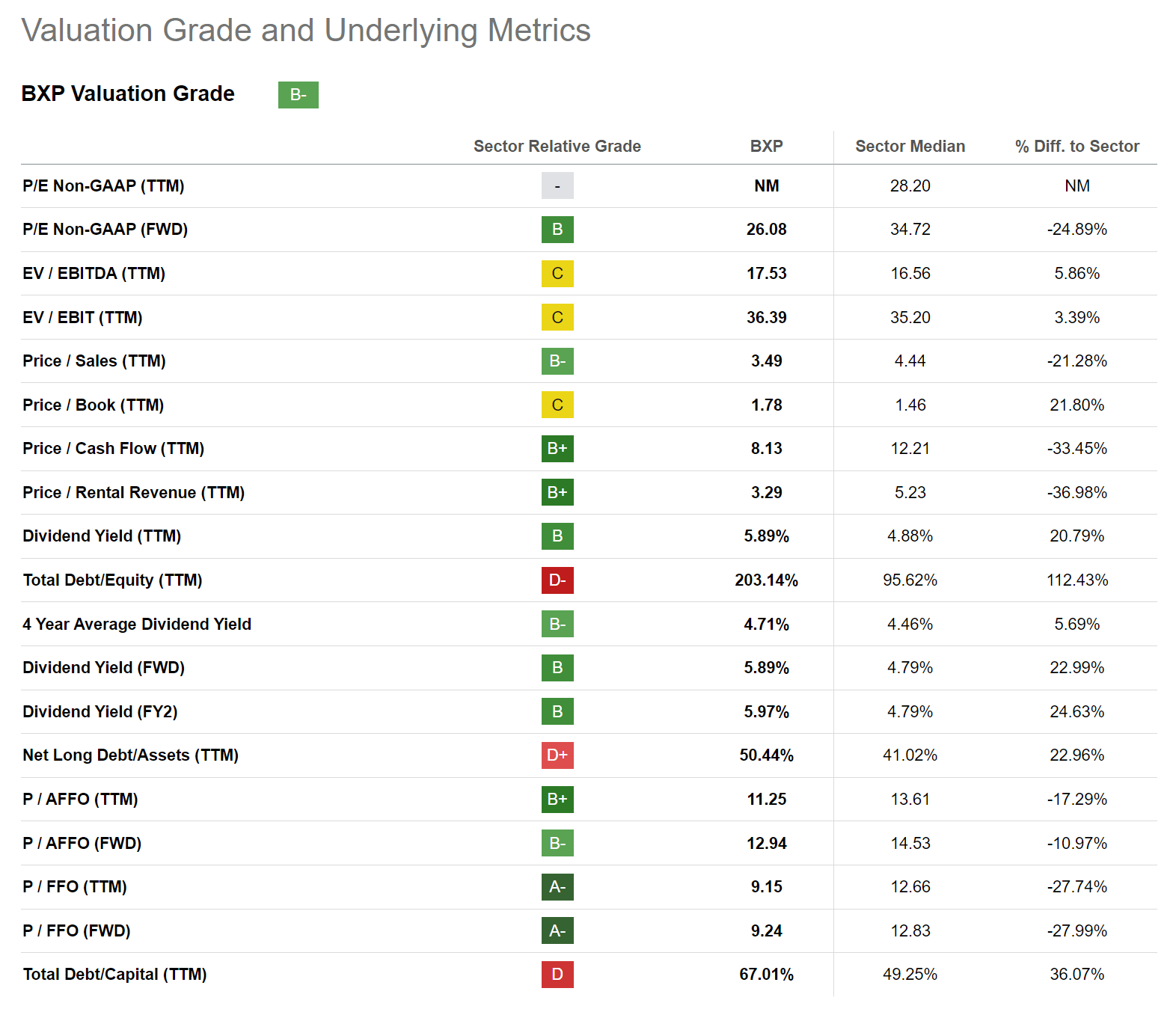

In addition to that, it can be highlighted that Boston Properties P/AFFO [FWD] Ratio of 13.92 stands 6.17% below the Sector Median, underscoring the thesis that the company is presently undervalued. This makes Boston Properties an attractive candidate for inclusion in a diversified dividend portfolio.

The Seeking Alpha Valuation Grade, which you can find below, underscores the company’s presently attractive Valuation.

Source: Seeking Alpha

Coca-Cola

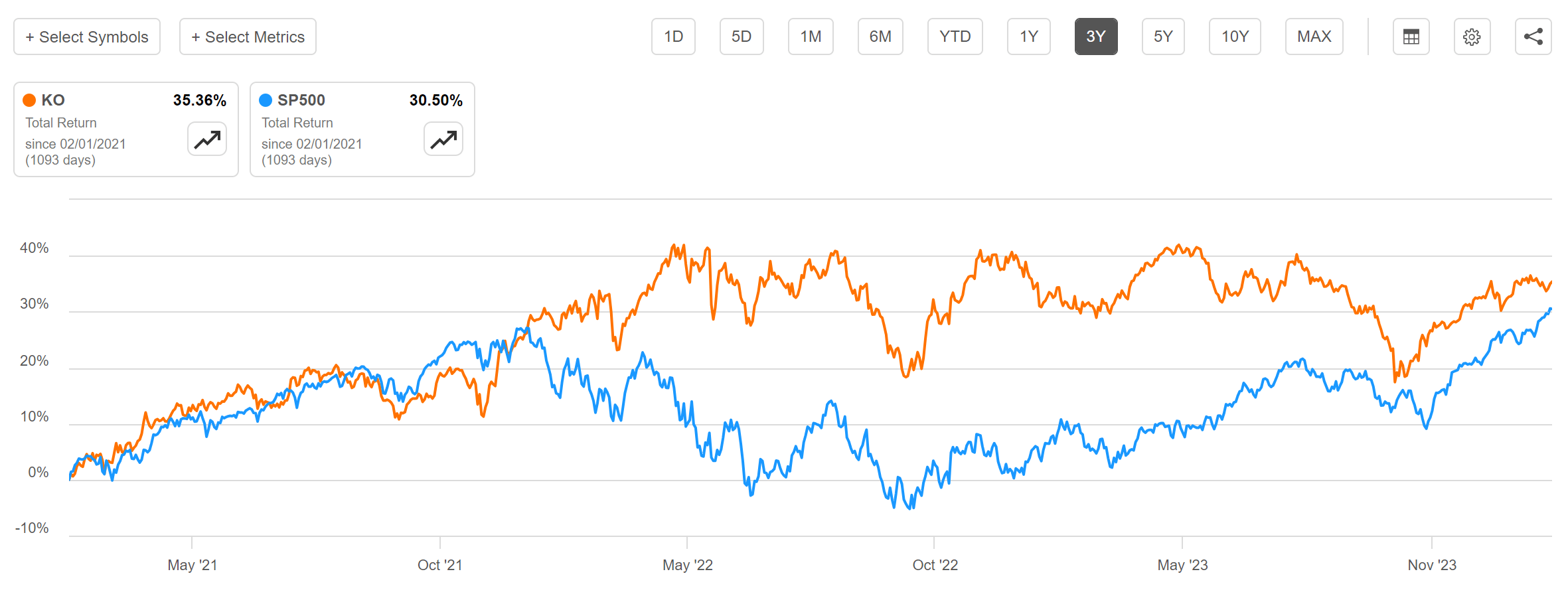

Considering the past 3 years, Coca-Cola has shown a Total Return of 35.36%, outperforming the S&P 500, which has shown a Total Return of 30.50% during the same time frame.

Source: Seeking Alpha

With a P/E GAAP [FWD] Ratio of 24.12, which lies 4.75% below its 5-year average, I believe that Coca-Cola is presently slightly undervalued. This suggests that the company might be an attractive addition to your dividend income-oriented investment portfolio at this moment in time.

Furthermore, it can be highlighted that the company’s dividend metrics are attractive to investors. Coca-Cola pays a Dividend Yield [FWD] of 3.07% while boasting a 10-year Dividend Growth Rate of 5.09%.

Verizon

Verizon distinguishes itself not only through its impressive Profitability metrics: the company exhibits a Gross Profit Margin [TTM] of 59.53%, which is 20.94% above the Sector Median (48.81%), and a Return on Equity of 12.65%, which is 215.79% higher than the Sector Median, but also due to its compelling blend of dividend income and dividend growth. Verizon showcases a Dividend Yield [FWD] of 6.26%, alongside a 10-year Dividend Growth Rate [CAGR] of 2.34%.

Considering Verizon’s P/E GAAP [FWD] Ratio of 9.37, it can be stated that the company is currently undervalued. Its current P/E GAAP [FWD] Ratio not only stands 11.22% below its 5-year average, it also lies 46.19% below the Sector Median.

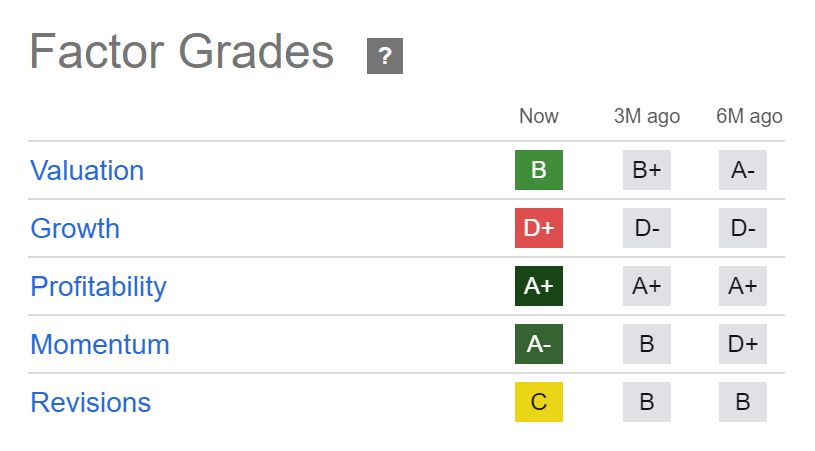

The graphic below shows the Seeking Alpha Factor Grades for Verizon, which further underscore the company’s presently attractive Valuation and excellent Profitability metrics.

Source: Seeking Alpha

AT&T

AT&T presently showcases a Free Cash Flow Yield [TTM] of 16.25%, indicating that it could be an attractive addition to your investment portfolio when considering that its current Valuation is not based on high growth expectations.

In terms of Valuation, it is worth noting that AT&T presently exhibits a P/E GAAP [FWD] Ratio of 8.40, which is 51.77% below the Sector Median and 23.18% below its Average from the past 5 years, reinforcing my investment thesis that AT&T is currently undervalued.

AT&T’s EBITDA Margin [TTM] of 34.17% (which is 76.59% above the Sector Median) and its Net Income Margin [TTM], which is 235.92% above the Sector Median, is a reflection of the company’s strong Profitability.

At its current price level of $18.04, the company pays a Dividend Yield [FWD] of 6.27%. This makes AT&T a compelling addition to any investment portfolio with a focus on dividend income.

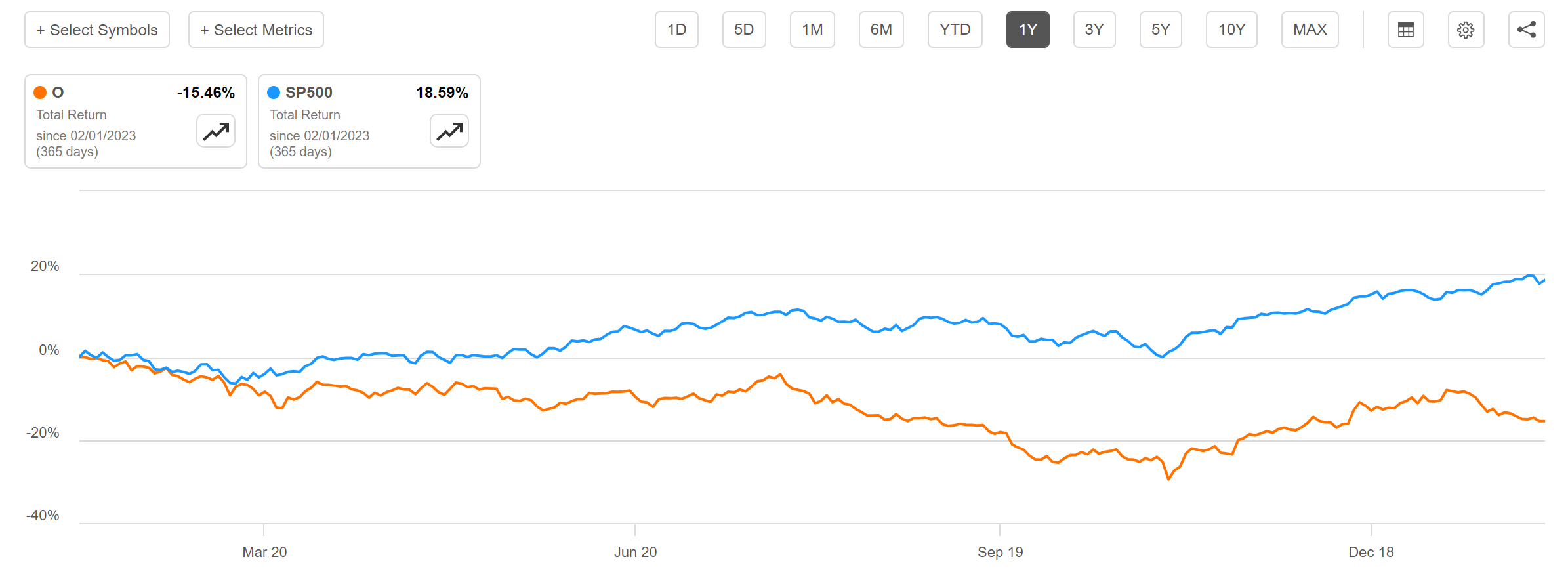

Realty Income

Over the past 12 months, Realty Income has experienced a negative Total Return of -15.46%, in contrast to the S&P 500’s positive Total Return of 18.59% during the same period.

Source: Seeking Alpha

Given its Dividend Yield [FWD] of 5.58%, 3-year Dividend Growth Rate [CAGR] of 4.16%, and FFO Payout Ratio of 73.89%, I believe that Realty Income is currently particularly appealing for long-term investors.

These metrics suggest that investors can not only anticipate an attractive dividend income in the present, but also the potential to significantly increase this income over the long term.

It is further worth highlighting that Realty Income has achieved 104 consecutive quarterly dividend increases, showcasing the company’s enormous capacity for delivering dividend growth to investors.

In addition to that, Realty Income’s EPS Diluted Growth Rate [FWD] of 20.90% underscores my belief that the company’s growth outlook is positive.

Realty Income presently boasts a P/AFFO [FWD] Ratio of 13.80, which is 7.00% below the Sector Median, strengthening my belief that the company is currently undervalued.

British American Tobacco

Given British American Tobacco’s currently attractive Valuation (P/E GAAP [FWD] Ratio of 7.07), which is 26.17% below its 5-year Average and 63.23% below the Sector Median, in combination with its appealing Dividend Yield [FWD] of 9.33% and 10-year Dividend Growth Rate [CAGR] of 2.85%, I am convinced that the company can be an attractive addition to your dividend portfolio.

Its attractive Free Cash Flow Yield [TTM] of 18.83% strengthens my belief that the company is attractive for those investors who aim to invest with a reduced risk level. This metric highlights that British American Tobacco’s stock price is not based on high growth expectations, thus providing investors with a margin of safety.

In addition, I believe that the company’s growth outlook is intact, given its EPS FWD Long Term Growth Rate [3-5Y CAGR] of 5.31%.

Altria

In 2023, Altria reported an adjusted diluted EPS of $4.95, which is an increase of 2.3% compared to the previous year, reflecting the company’s growth perspective.

Like British American Tobacco, Altria is particularly appealing for those investors that aim to blend dividend income and dividend growth: this thesis is underlined by Altria’s current Dividend Yield [FWD] of 9.69%, accompanied by its 3-year Dividend Growth Rate [CAGR] of 4.14%. The company’s strength of providing investors with dividend growth is further underscored by its 5-year average EPS Diluted Growth Rate [FWD] of 5.57%.

In addition to the company’s strong competitive advantages and its excellent Profitability metrics (underscored by its Gross Profit Margin [TTM] of 69.44%), Altria also showcases an attractive Valuation: the company presently exhibits a P/E [FWD] Ratio of 8.82, which stands significantly below the Sector Median (19.23) and significantly below its average from the past 5 years (12.17).

When comparing the company to its competitor Philip Morris International Inc. (PM), it is worth highlighting Altria’s superiority in terms of dividend income (with a Dividend Yield [FWD] of 9.69% compared to Philip Morris’ 5.72%) and dividend growth (Altria has a 3-year Dividend Growth Rate [CAGR] of 4.15% compared to 2.74%), in addition to a reduced Payout Ratio (76.77% compared to 84.60%) and a significantly lower Valuation (P/E [FWD] Ratio of 8.75 compared to 18.07). These metrics underline that Altria is presently the superior choice when compared to Philip Morris.

U.S. Bancorp

One of the most interesting aspects of U.S. Bancorp from the perspective of a long-term investor is its ability to provide an appealing mix of dividend income and dividend growth. While U.S. Bancorp’s Dividend Yield [FWD] presently stays at 4.52%, it has shown a 5-year Dividend Growth Rate [CAGR] of 7.57%.

The bank’s ability to provide your portfolio with dividend growth is further underlined by its 13 consecutive years of dividend growth and attractive Payout Ratio of 58.84%.

Today, the bank’s P/E [FWD] Ratio stands at 11.07, which is slightly below its average over the past 5 years (11.95). This metric suggests that the bank is undervalued at its current stock price.

With this in mind, it further strengthens my investment thesis that the US bank is an attractive addition to your dividend income portfolio at this moment in time.

U.S. Bancorp presently boasts a Market Capitalization of $64.72B, which is significantly lower when compared to JPMorgan Chase & Co. (JPM) $501.58B, Bank of America Corporation’s (BAC) $268.52B, or Wells Fargo & Company’s (WFC) $180.59B.

However, with its Dividend Yield [FWD] of 4.52% and its 5-year Dividend Growth Rate [CAGR] of 7.57%, U.S. Bancorp shows the most balanced mix between dividend income and dividend growth when compared to JPMorgan (2.41% and 8.55% respectively), Bank of America (2.82% and 11.24%), and Wells Fargo (2.79% and -4.51%).

These metrics indicate that U.S. Bancorp could be a potential candidate for inclusion into The Dividend Income Accelerator Portfolio.

However, I believe that an investment in U.S. Bancorp comes attached to a significantly higher risk level when compared to JPMorgan or Bank of America, given its higher Payout Ratio of 58.84% (compared to JPMorgan’s 25.28% and Bank of America’s 29.97%) and less diversified product portfolio. For these reasons, I would provide U.S. Bancorp with a significantly lower share compared to the overall portfolio in comparison to Bank of America or JPMorgan.

Conclusion

I am convinced that the high dividend yield companies I have discussed in today’s article can be excellent long-term additions to your dividend portfolio. This is especially the case when strategically complemented with dividend growth companies within a well-diversified investment portfolio.

Reaching a balanced mix between dividend income and dividend growth companies offers investors multiple benefits: it ensures a stable income stream from today on (with a significant contribution from companies with high dividend yields) and a dividend income that increases to a significant amount from year-to-year (with a significant contribution from dividend growth companies).

I personally employ this investment approach through the creation of The Dividend Income Accelerator Portfolio, and I firmly believe that it holds appeal for a wide range of investors, including both younger and older investors. This strategy is ideal for those looking to generate extra income while continuously raising their income year by year, and, simultaneously, investing with a reduced risk level.

This approach allows you to enjoy the immediate benefits from the dividend payments (for example, you could use the dividend payments for your next vacation), while, simultaneously, striving to reach an attractive Total Return with a high likelihood of success. So, how does that sound to you?

Author’s Note: I would appreciate hearing your opinion on my selection of high dividend yield companies to consider buying in February 2024. Do you already own or plan to acquire any of the picks? Which are currently your favorite high dividend yield companies?

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")