Galeanu Mihai

Introduction & Investment Thesis

Workday (NASDAQ:WDAY) is a provider of enterprise cloud applications for finance and human resources. The stock has underperformed the S&P 500 and Nasdaq 100 YTD. The company released its Q4 FY24 earnings report last month, where revenue and earnings exceeded expectations. It is projected to grow its revenue by 15–16% to approximately $8.4B in FY25 as it continues to focus its efforts on expanding internationally while building its partner ecosystem in order to grow efficiently through referrals, co-selling, and building differentiated solutions in order to drive better business outcomes for its customers. At the same time, the company is also investing its resources in integrating AI capabilities on its platform, along with the announcement of its acquisition of HiredScore, in order to accelerate its AI product roadmap. Meanwhile, Workday’s profitability is growing along with expanding margins as it streamlines its operating expenses.

There is no denying that the company has superior fundamentals; however, when looking at the valuation, I believe that there is room for at most 12% upside from its current levels, which to me does not present an attractive entry point for long-term investors. As a result, I will stay on the sidelines, waiting for a better entry point to initiate a position, and rate the stock a “hold” at the moment.

About Workday

Workday is a cloud-based software company that provides solutions for financial management, spend management, human capital, planning, and analytics so that their customers can better plan, execute, and improve their business operations.

In terms of its business model, Workday targets medium and large businesses globally across different industries, where it derives its revenue from a combination of subscription and professional services. The company uses a “land-and-expand” go-to-market strategy, which allows it to sell subscriptions for additional product modules to existing customers as they expand their footprint with Workday’s products.

In FY24, the company generated $7.3B in revenue, out of which Subscription revenue accounted for 91% at $6.6B, while Professional Services accounted for the remaining 9% at $5.5B.

The good: International Revenue growth, Partner ecosystem, Product Innovation & Growing Margins

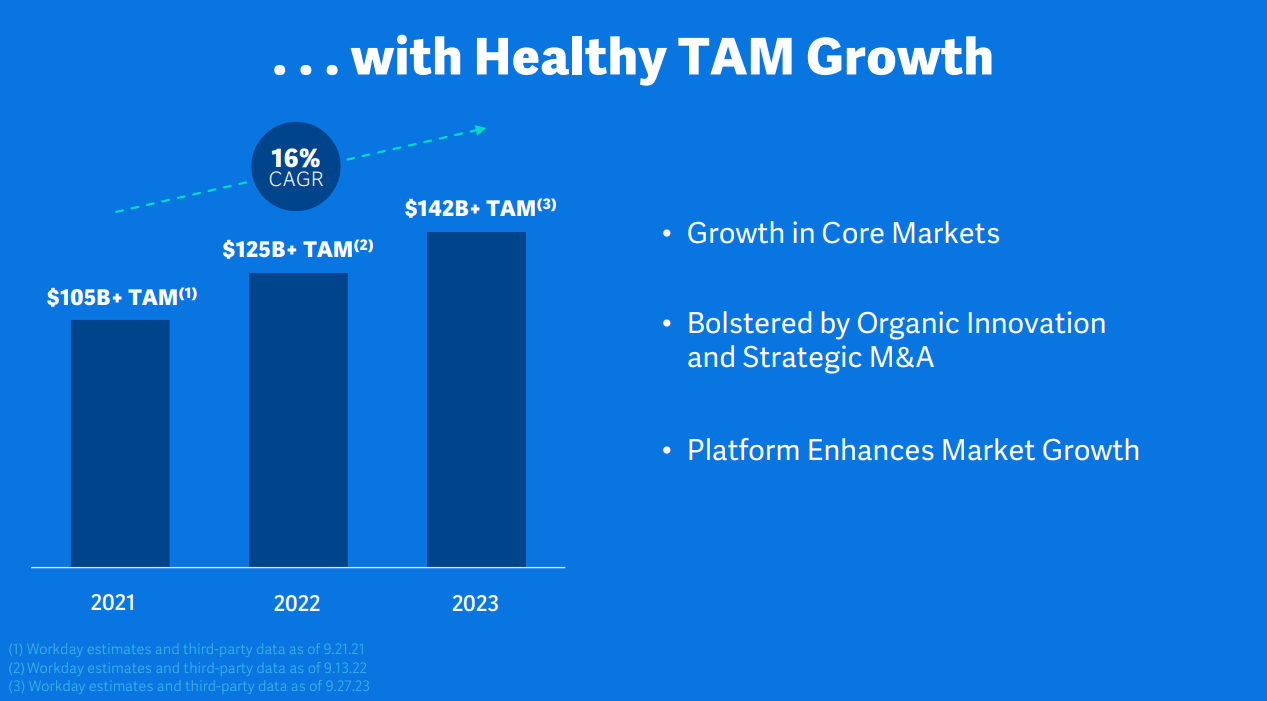

Workday operates in a large total addressable market (TAM) that it estimates at $142B in 2023, as per its Investor Day Presentation. The TAM is calculated by summing up the sizes of the following markets: 1) Human Capital Management (HCM) at $58B and 2) Financial Management at $84B. Given that the company generated $7.3B in revenue in FY24, it would mean that it has penetrated 5% of its market share. As per its Investor Day Presentation, Workday has thus far penetrated 50% of Fortune 500 companies and 25% of Global 2000 companies, which means it still has 50% of Fortune 500 and 75% of Global 2000 remaining as part of its target market that is left to be penetrated, thus presenting a large enough market opportunity. Simultaneously, Workday believes that it has potentially $2B of expansion opportunity within their existing Top 100 Accounts, as it continues to drive deeper adoption of its solution suite, thus allowing it to expand its Annual Contract Value (ACV) and harness economies of scale.

2023 Investor Presentation: Workday’s growing TAM

In FY24, the company generated $7.3B in revenue, up 17% YoY. Subscription Revenue contributed 91% to total revenue, growing 19% YoY to $6.6B. One of the ways the company believes it can spearhead its growth trajectory in the coming years is through international expansion, with a specific focus in Europe, Middle East and Africa, as it estimates its international TAM at $80B. For the full year FY24, international revenue totaled $1.8B, growing 17% YoY, while US revenue also grew 17% YoY to $5.46B. This would mean that Workday has just about 2.2% penetration of its solutions outside of the US, which makes it a highly strategic opportunity to expand into in order to drive revenue growth. During the earnings call, Carl Eschenbach, CEO of Workday, highlighted that they saw healthy growth in ACV across key markets that include the UK, Spain, and France.

Furthermore, Workday management also highlighted Japan as a key investment priority and has therefore hired a new leader, Chikara Furuichi, to drive growth in that region. In my opinion, this further highlights the management’s focus on driving growth in key regions outside of the US, especially as the US market has matured and growth will likely stabilize moving forward. As a result, if Workday continues to see success in gaining market share abroad, it will keep its growth story alive.

Aside from Workday’s strategic focus to drive growth internationally, the company is also focused on building its partner ecosystem, which I believe will allow it to grow more efficiently through referrals, co-selling, and building differentiated solutions in order to drive better business outcomes for its customers. This is what Carl Eschenbach, CEO of Workday, said during the earnings call, which demonstrates the company’s focus on driving growth through robust partner ecosystems.

“During Q4, we announced a strategic partnership with Insperity. Through this partnership, Workday will become the platform powering Insperity’s PEO service for SMB organizations, effectively opening up a new market opportunity for us. It’s a terrific example of how we’re innovating our go-to-market strategy to drive growth. Another great example is the Spark&Grow offering, which we launched with Kainos. It helps our emerging and medium enterprise customers to go live on Workday in less than 4 weeks. We’ve seen incredible demand for this offering, and we’re just getting started. These are 2 great examples of momentum that is building across our ecosystem, which I’m pleased to share now includes more than 200 partners that have been onboarded to refer new sales leads and co-sell with us.”

At the same time, Workday remains committed to driving robust product innovation in order to continue to drive new customers as well as deepen adoption among its existing customer base. So far, Workday has introduced Workday Skills Cloud, which uses AI to gain insights into an organization’s current skills in order to enable managers to effectively lead and foster the career growth of their team members based on skills and interests. They further announced their acquisition of HiredScore in order to accelerate their AI product roadmap so that they can deliver insights in order to improve recruiting and internal mobility within an organization.

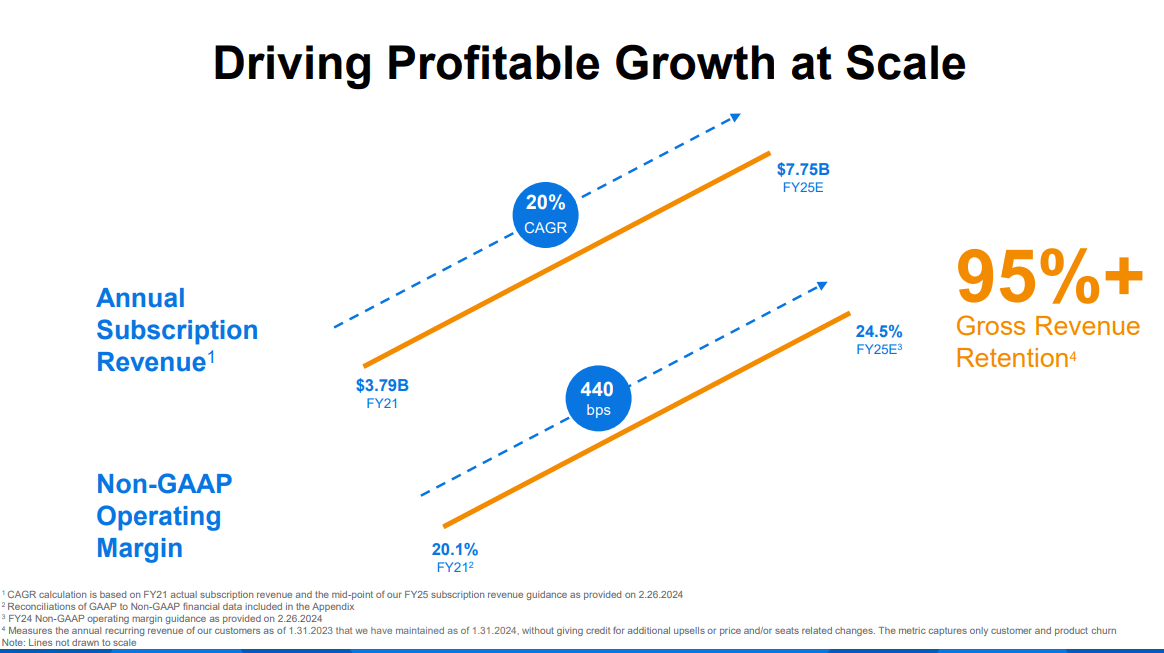

Shifting gears to profitability, Workday generated $1.7B in non-GAAP operating income in FY24, which grew 42% YoY at a margin of 24%, compared to a margin of 19.5% from the prior year. One of the reasons for the expansion in margin can be attributed to the streamlining of operating expenses that grew 10% YoY, relative to revenue that grew 17% YoY, which demonstrates the company’s growing operational efficiency. At the same time, Net Retention rate (NRR) is above 100%, which means that the company is continuing to see success in driving deeper adoption of its solutions across its existing customers, helping it unlock economies of scale.

Q4 FY24 Earnings Slides: Workday’s growing revenue and profitability

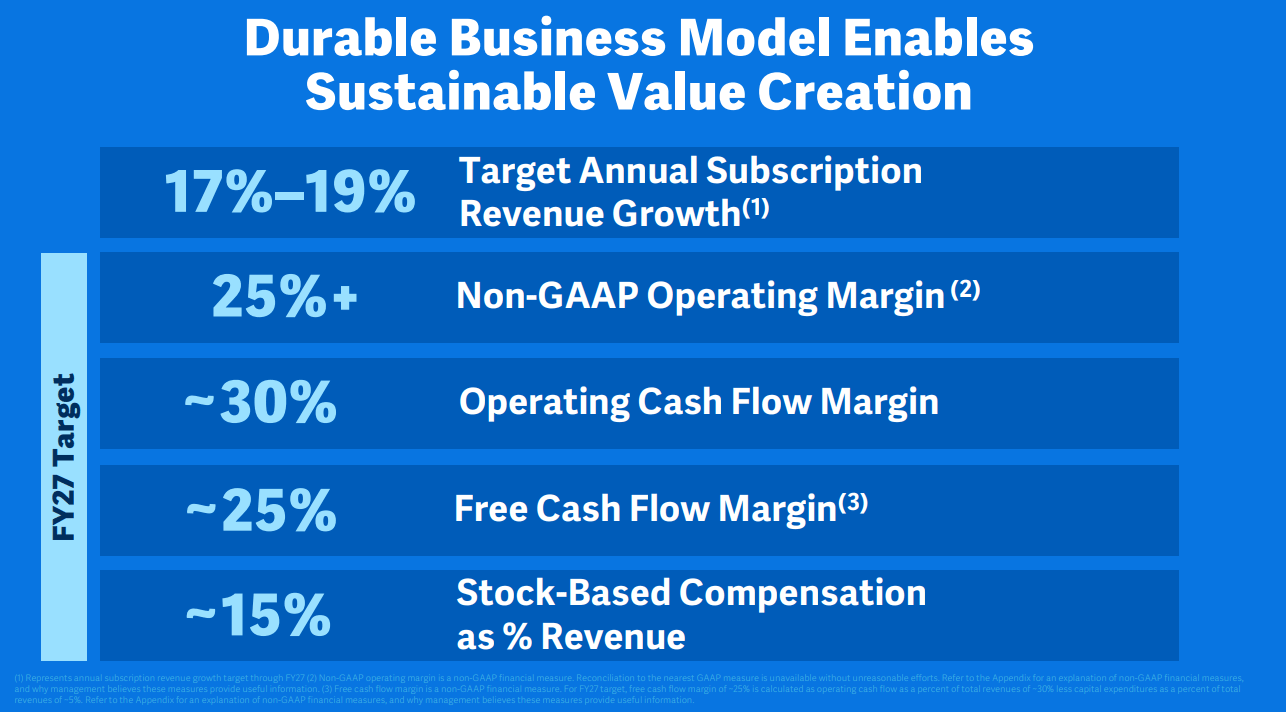

Looking forward into FY25, the company is expected to grow its revenues between 15 and 16% YoY to $8.35-$8.41B, with Subscription revenue projected to grow slightly faster between 17 and 18% YoY to approximately $7.74B. Meanwhile, the non-GAAP operating margin is expected to grow slightly to 24.5%, which would translate to a non-GAAP Operating Income of $2.04B. During the Investor Day presentation, the management further outlined that it expects subscription revenue to grow annually between 17 and 19% until FY27, while generating a non-GAAP operating margin of 25%. I believe that so far, the company has executed well, and if it continues to drive deeper market share internationally with the help of its partner ecosystem while investing in innovation to deepen adoption of its solution among its existing customer base, it should be able to achieve both its revenue and profitability targets.

The bad: Large players and an uncertain global macroeconomic environment

So far, Workday has very well navigated a tough macroeconomic environment; however, with inflation above the Fed’s 2.2% and interest rates at 5.25-5.5%, there is a growing chance of a broader slowdown, which may tip the US economy into a recession. Meanwhile, we have already seen parts of Europe falling into a recession, along with Japan. This may hurt Workday’s growth trajectory, especially its plans for international expansion, if we see companies cutting down enterprise spending in order to protect their margins.

At the same time, Workday also faces competition from deep-pocketed players such as SAP (NYSE:SAP), Oracle (NYSE:ORCL) in the mid-market and large enterprise market that Workday operates in. While product innovation pertaining to generative AI can play as a major differentiation factor, I would note that Workday is smaller in size compared to these larger players in the industry, which could prove to be a competitive disadvantage.

Tying it together: Workday has a 12% upside from its current levels.

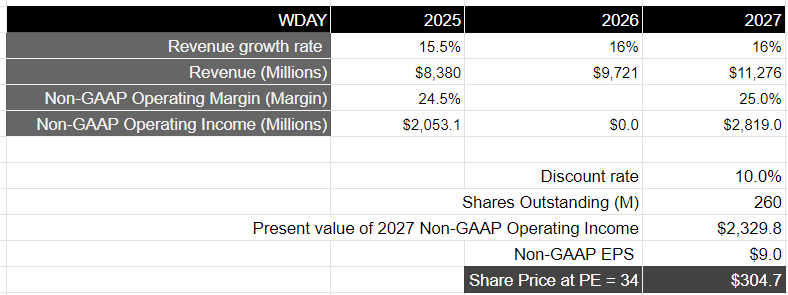

Assuming that Workday continues to grow its total revenue by 16% annually until FY27, it should generate approximately $11.3B in revenue. I believe Workday will be able to achieve their projections, given the management’s focus to drive growth internationally, while building its partner ecosystem and investing in its product innovation at the same time. In terms of profitability, Workday management believes it should be able to maintain a non-GAAP operating margin of 25%. Given that Workday’s current non-GAAP operating margin is between 24-25%, it should be able to maintain that until FY27, per management’s expectation, as it continues to unlock operating leverage, as it drives deeper adoption of its solutions among existing customers, while streamlining operating expenses. At a non-GAAP operating margin of 25%, it would translate to a non-GAAP operating income of $2.8B by FY27, which is equivalent to $2.3B when discounted at 10%.

2023 Investor Day Presentation: Workday’s long-term financial model

Taking the S&P 500 as a proxy, where its companies grow their earnings on average by 8% over a 10-year period, with a price-to-earnings multiple of 15-18, I believe that Workday should trade at twice the multiple, as I believe it will grow its earnings at twice the rate of the average S&P 500 company over the next 3 years. That would translate to a price-to-earnings multiple of approximately 34, which is twice the PE ratio of the S&P 500, or a price target of $304, as can be seen in the valuation model below. This represents an upside of 12% from current levels.

Author’s Valuation Model

However, looking at the S&P 500, its current forward price-to-earnings ratio stands at 20.9, which is above its 5-year average of 19.1 and 10-year average of 17.7. This means that in the shorter time frame, we could see a sizable pullback in the S&P 500 of at least 10% to revert its PE ratio to its 10-year average. This could take place, in the event of inflation coming in higher than expected, or Q1 earnings coming slightly below expectations. Given that Workday has a beta of 1.33, a decline of 10% in the S&P 500 can translate to a 13% decline in Workday’s stock price, in which case, there would be no net upside at the current stock price level, given the 13% margin of safety. As a result, I will rate the stock a “hold” at the moment.

Conclusion

Workday has solid fundamentals and great growth drivers that include its partner ecosystem, international expansion, and rapid product innovation. At the same time, the management remains focused on improving profitability. However, based on my valuation, I believe that there is approximately 12% upside from where the stock is currently trading, which I believe does not present an attractive entry point for long-term investors. As a result, I will be waiting for a better opportunity to initiate a position in the company and, in the meantime, rate the stock a “hold” at the moment.

Q2 2024 Earnings Call Transcript")