valilung/iStock Editorial via Getty Images

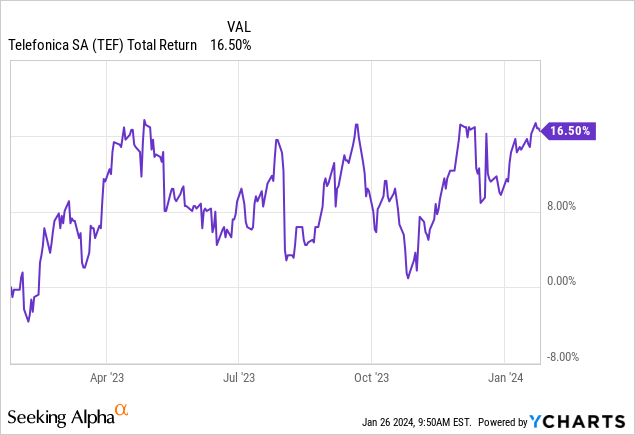

Shares of Spanish telecoms giant Telefonica (NYSE:TEF) have had a pretty solid 12 months, returning around 17% (with dividends) in that time amid stabilizing earnings in Spain and fresh medium-term financial targets that look to have been well-received by the market.

I think it is fair to say that Telefonica holds a mixed bag of assets overall. Its domestic Spanish business is the pick of the bunch alongside a much improved position in the U.K., offset by more so-so operations in Germany, Brazil and various other LatAm markets. While growth prospects are predictably modest here, these shares do look quite cheap on a rough sum-of-the-parts basis, and I would also suggest that the 8%-yielding dividend is quite a bit safer than the algorithms might imply. As such, I open on the stock with a Buy rating.

A Mixed Bag

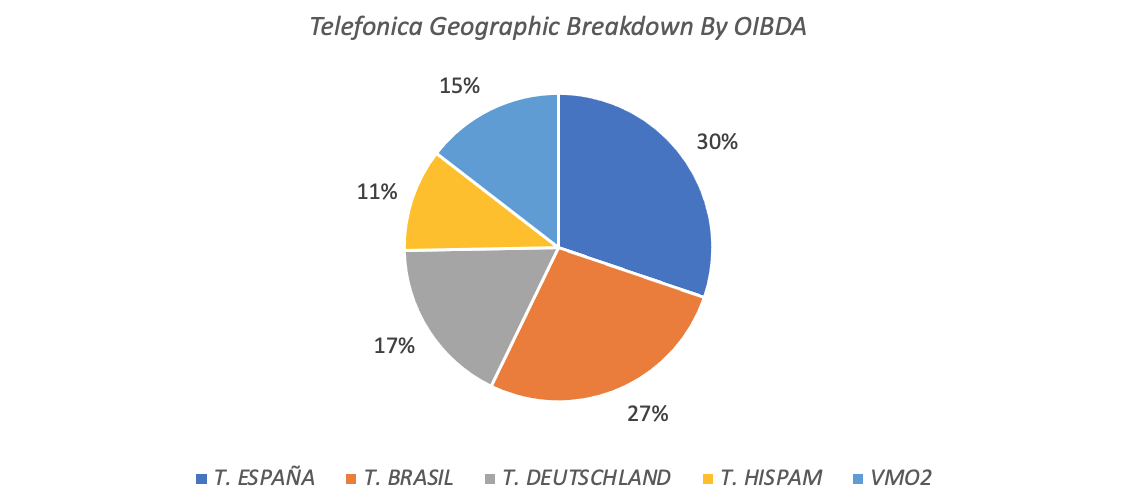

Telefonica offers investors exposure to telecoms markets in Spain, Germany, the United Kingdom, Brazil, and a collection of other LatAm countries. Spain accounts for the largest share of group earnings, with 9M2023 operating income before D&A (“OIBDA”) of €3.4 billion equating to circa 30% of the company’s total. Brazil (~27%), Germany (~17%), its share of the U.K. joint-venture (~15%), and Hispanic America (~11%)(“HispAm”) account for the remainder.

Data Source: Telefonica Q3 2023 Supplemental Data Release

In Spain, Telefonica is the incumbent player offering both fixed and mobile services, controlling around 35% of the fixed broadband market and 28% of the mobile market. It further reports around 4.5 million converged customers in the country. Benefits of a converged offering are numerous, but typically include lower churn rates, which in turn lowers customer acquisition costs as it is cheaper to keep hold of an existing customer than acquire a new one.

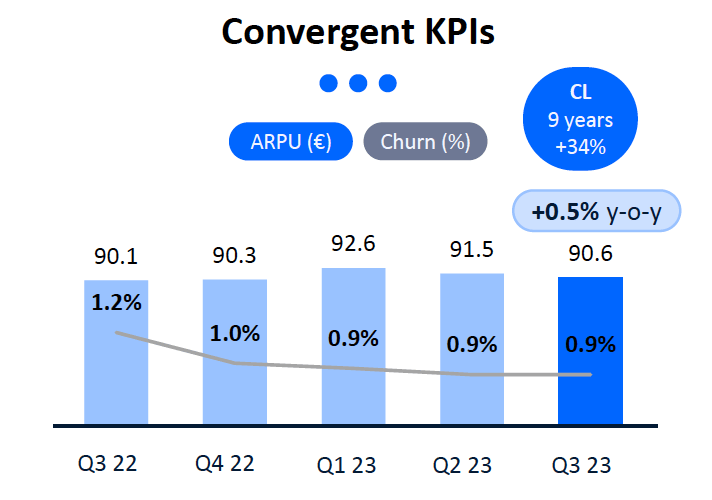

Telefonica currently generates average revenue per user of over €90 for converged customers in Spain, which is around 60% higher than the figure reported by Spanish number two player Orange (NYSE:ORAN). Further, Telefonica will generate around €4.5 billion in OIBDA this year in Spain, mapping to around €3 billion in operating free cash flow at a group-leading 25% margin. That would amount to around 35% of the group’s total – a higher figure than its EBITDA share, highlighting how relatively cash generative its Spanish business is.

Source: Telefonica Q3 2023 Results Presentation

Telefonica’s other attractive business is in the U.K., where it holds a 50% share in Virgin Media O2 (“VMO2”) alongside recently-covered Liberty Global (LBTYA, LBTYK, LBTYB). Previously, Telefonica-owned O2 operated as a mobile business only, with the U.K. mobile market not being especially attractive from a competitive position. Combined with Virgin Media’s cable network, VMO2 is now a converged fixed-mobile player, putting it in a much stronger position than before. Cable companies have also typically benefitted from less burdensome CapEx requirements compared to legacy telecoms providers, with the latter having to spend heavily to upgrade legacy copper networks to full fiber. As a result, I think this asset should command a higher multiple than Telefonica’s other telecoms businesses, which basically forms the crux of the value case (more on that later).

It is very much a mixed bag elsewhere. In Brazil, Telefonica owns circa 75% of listed Telefonica Brasil (VIV), and this segment is only a shade smaller than the Spanish business by OIBDA. While a converged operator, the company has been grappling with market share losses in broadband, investing heavily in full fiber to try to stabilize the situation. Capital intensive businesses usually represent a slightly bigger risk in emerging markets given the inflation/currency angle, so I’m not overly keen on this exposure. Ditto for HispAm, which is why the company is exploring strategic options for the segment. A spin-off probably represents the path of least resistance and would be my preferred option.

Finally, Telefonica’s German business, Telefonica Deutschland (OTCPK:TELDY)(OTCPK:TELDF), is also not great, with the company essentially a mobile only player there. While Telefonica Deutschland does offer fixed services, it doesn’t own a fixed network in the country, and the economics of renting will probably skew heavily in favor of the network owners. As such, Vodafone (VOD) and Deutsche Telekom (OTCPK:DTEGY)(OTCPK:DTEGF) are probably much better options for investors looking for exposure to that space.

Earnings Outlook; Dividend Secure

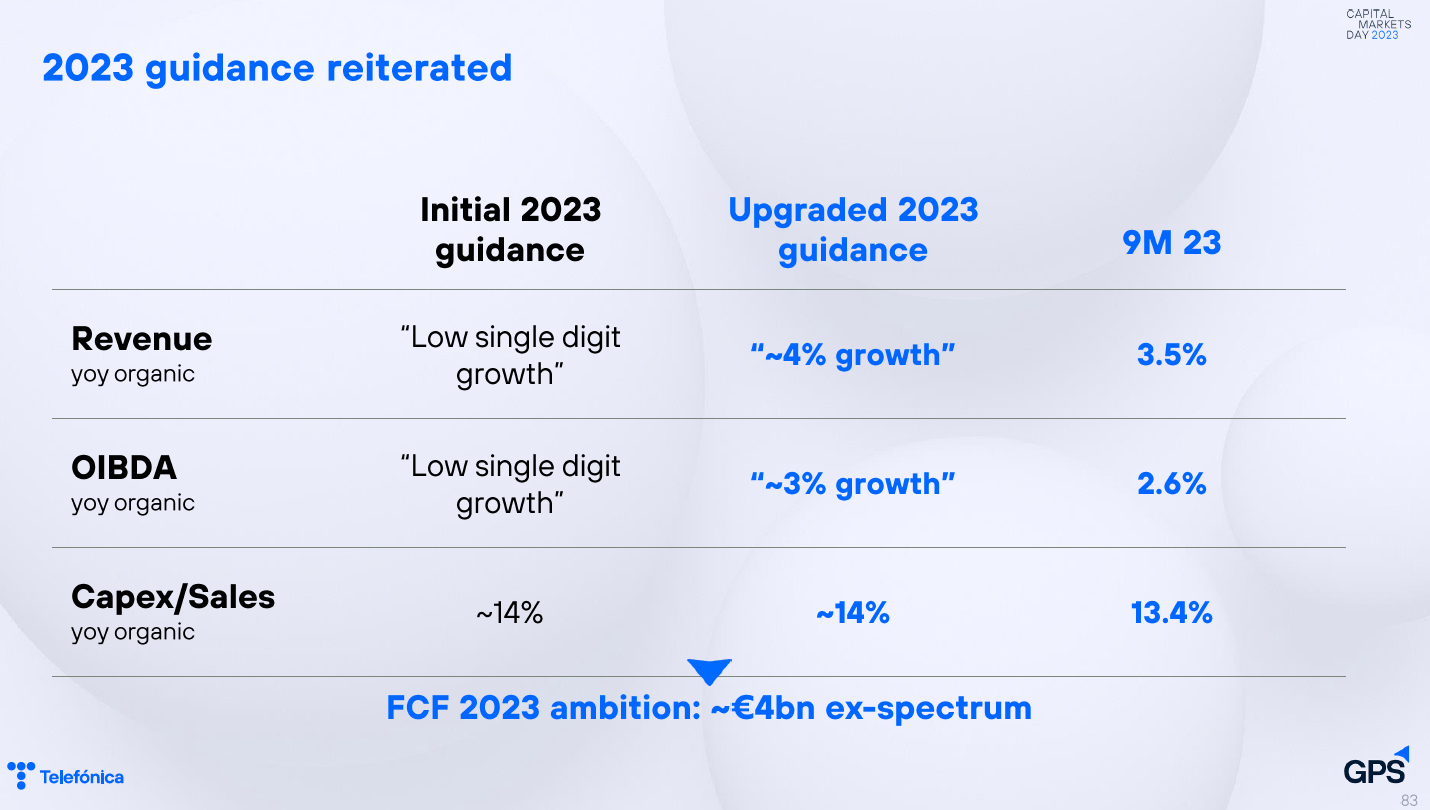

During its Q4 2023 Capital Markets Day, Telefonica released a fresh set of medium-term financial goals. These include a 1% top line CAGR for the 2023-2026 period, with EBITDA and operating free cash flow (“FCF”) seen growing at higher average annual rates of 2% and 5%, respectively, over the same period. For 2023, management targets include 4% organic revenue growth and 3% growth in OIBDA.

Source: Telefonica 2023 Capital Markets Day

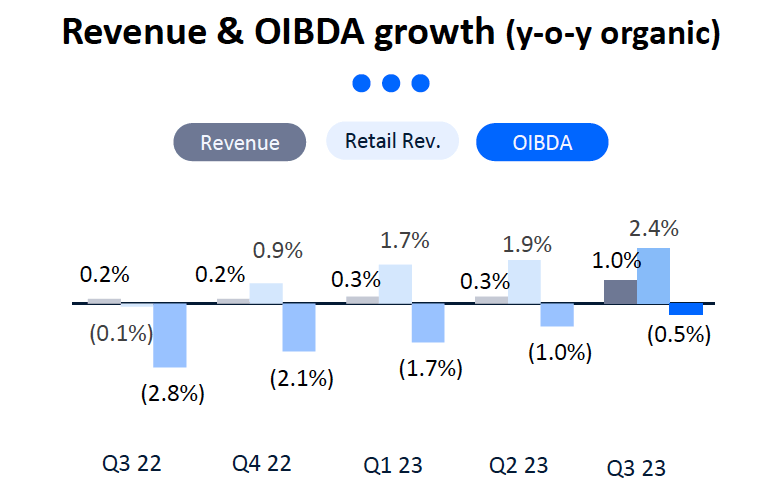

This does not look overly aggressive. Though the best part of Telefonica’s business, Spain has been registering modest declines in OIBDA in recent quarters due to inflationary pressures on the company’s cost base there. As the below graphic shows, the trend has been improving as inflation moderates, and I expect that to continue when the company posts full-year results in late February. That alone should put the company on track to meet total company-wide targets.

Source: Telefonica Q3 2023 Results Presentation

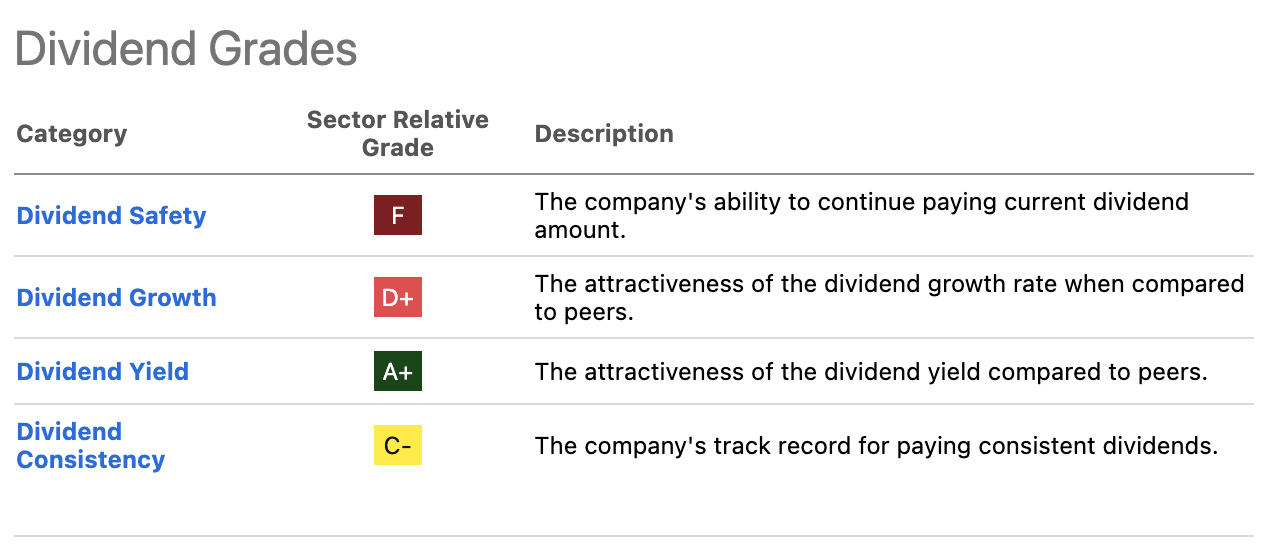

Similarly, the company’s much higher operating FCF CAGR target of 5% is largely a function of normalizing CapEx as fiber rollouts pass their peak levels. This also puts Telefonica’s dividend on firmer footing than it might currently appear, with Seeking Alpha’s Dividend Scorecard only grading TEF a lowly ‘F’ for Dividend Safety relative to the sector.

Source: Seeking Alpha

The €0.30 annual payout (~$0.33 per ADS) equates to around €1.7 billion in cash terms, swallowing most of the €2 billion in FCF the company expects to report for 2023. As the CapEx/Sales ratio declines to around 12% over the next couple of years, that will free up an extra €800 million or so in annual surplus cash flow before considering organic growth. Leverage is around 2.5x OIBDA-aL (i.e. after leases), and management is targeting modest reduction to 2.25-2.5x by 2026. That leaves little room for dividend hikes over the next few years, so while the yield looks reasonably secure at around 8% right now, I don’t see much growth on top in the near term.

Shares Look Around 25% Undervalued

Telefonica’s ADSs trade for $4.18 apiece at time of writing, with the Madrid-listed ordinary shares at €3.82 each. That implies an enterprise value of around €57 billion (~$63 billion) based on circa 5.7 billion shares outstanding and around €35 billion in total net debt (including lease liabilities).

The way I see it, that basically accounts for Telefonica’s consolidated businesses, leaving the VMO2 J.V. to drive significant upside. Now, Telefonica’s Brazilian and German businesses are listed on their respective stock exchanges, so gauging their value is relatively straightforward as the market has already provided a view. Telefonica Brasil trades for around 4.7x forward EBITDA as per Seeking Alpha, while Telefonica Deutschland trades on a multiple of around 4.2x. This accounts for just under 40% of Telefonica’s total enterprise value after adjusting for minority stakes. Attaching a 4.7x multiple to the HispAm segment, in line with Brazil, captures another ~13%, leaving around 50%, or ~€28 billion, for the Spanish business. That equates to a multiple of around 6x OIBDA, which looks reasonable for a market-leading incumbent with solid profitability. The best incumbent telecoms businesses in Europe, KPN (OTCPK:KKPNF)(OTCPK:KKPNY) and Swisscom (OTCPK:SCMWY)(OTCPK:SWZCF), trade in excess of 7.5x, so 6x for the Spanish business does not look expensive.

With the above accounting for Telefonica’s enterprise value, this leaves VMO2 to drive upside to fair value. Cable companies typically trade on higher multiples for the reason I set out earlier, namely that they have less onerous CapEx requirements in terms of upgrading their networks. VMO2 is also a converged player, bringing additional benefits described above. A multiple in line with U.S. cable companies like Comcast (CMCSA), Charter (CHTR) and Altice USA (ATUS) would not be unreasonable, which as per Seeking Alpha trade in the 7-8x EBITDA region. At the lower-end of that range and adjusting for net debt and Telefonica’s share of the JV, the equity would be worth an extra ~€0.90 per share (~$1 per ADS) to Telefonica. Adding that to the current stock price gets me to a fair value of just over €4.70 per share (~$5.15 per ADS), implying around 25% upside to fair value. As a result, I attach a Buy rating to Telefonica stock.

Risks

Telefonica’s business comes with numerous risks. Currency is perhaps the most obvious, with the ADSs priced in dollars but the business generating sales and earnings in EUR, GBP, BRL and various other LatAm currencies. Its emerging markets operations arguably present extra currency risk though inflation and currency depreciation, and this represents a material part of Telefonica’s overall business. Furthermore, the telecoms sector is typically highly competitive and tightly regulated, both of which can materially affect profitability. As telecoms services are largely commoditized, there may be little that Telefonica could do to offset pressure to its earnings power should it encounter these headwinds.

Q2 2024 Earnings Call Transcript")