Valeriy_G/iStock via Getty Images

I’ve been asked by acquaintances if I admire covered call ETFs, sometimes surprising them by saying that I do not. Many of my articles cover dividends, and many investors are drawn dividends after the Fed began hiking rates in 2022. I have also noticed rising interest in passive income among savers and investors. The Global X S&P 500® Covered Call ETF (NYSEARCA:XYLD) is one such example of a fund designed to supply income to its buyers through covered calls.

Common advice for people who want to invest without thinking too hard about it is to buy shares of the S&P 500, in order to get diversification and to let it grow over time. XYLD allows folks to buy the S&P 500 but with a more income-driven approach.

XYLD Prospectus

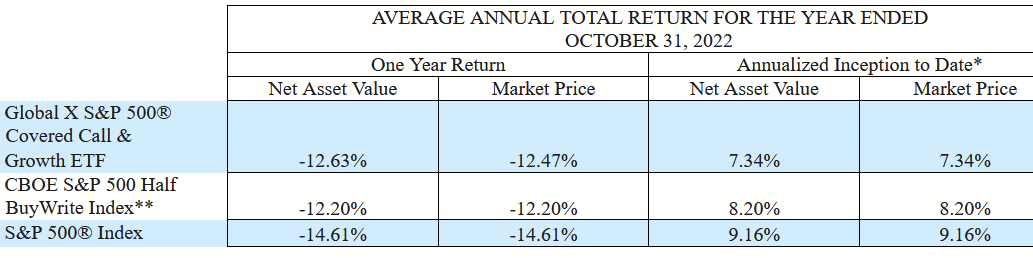

We see above that the S&P 500 has had a better return since XYLD’s inception, so that leaves open the question of why we might invest into it. I will make the case that the fund us okay to HOLD for the high yield of income, but folks should be aware of long-term factors that may demonstrate inconvenient.

Concept of the Fund

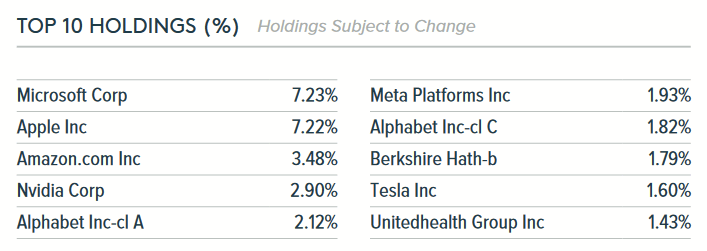

XYLD is invested passively to track the CBOE S&P 500 BuyWrite Index. In pursuit of this, it will invest 80% of its funds into the stocks of the S&P 500. Here’s a screenshot of the Top 10 holdings to remind you what kind of stocks are in the S&P 500.

Global ETF Fact Sheet (globalxetfs.com)

Being the S&P 500, these are America’s biggest companies. The other 20% of the fund is devoted to call options. Let’s talk about that.

Instead of writing covered calls on the stocks themselves, the fund writes them on the S&P 500 index. These contracts are ultimately settled in cash instead of shares. If the market goes above the strike price of the contract, the fund will have to pay the difference. As long as the premium is higher than this difference, it will be profitable and supply distributable income. As stated in the Prospectus:

Because of the Fund’s options-writing strategy, it forfeits potential profit when the Underlying Index rises above the strike price of the index call option.

Thus, while capital appreciation can occur, the fund itself points out that much of this is lost because upside (from market growth) results in XYLD having to pay the difference. Since the market has historically grown over time, the mechanisms of the fund mean that the capital gains of its stocks can be a source of friction that slows down long-term returns.

How Has the Income Done?

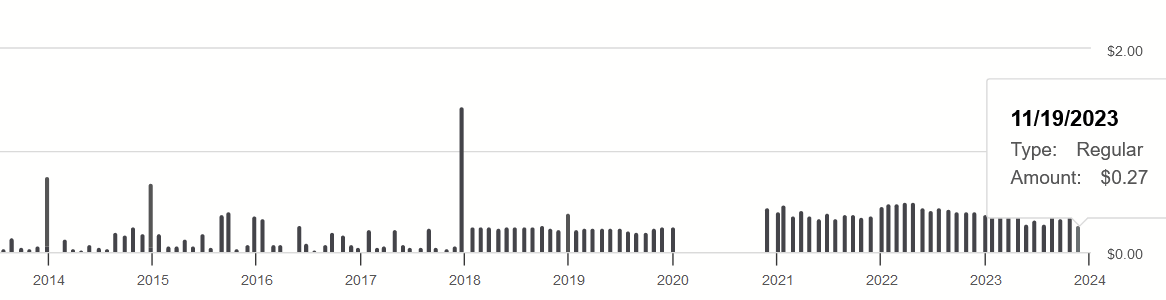

If XYLD doesn’t return as well (overall) as the S&P 500, we’ll at least want to see if we are happy with the income’s performance. The history of monthly payments will look odd to most. Here’s a snapshot:

Seeking Alpha

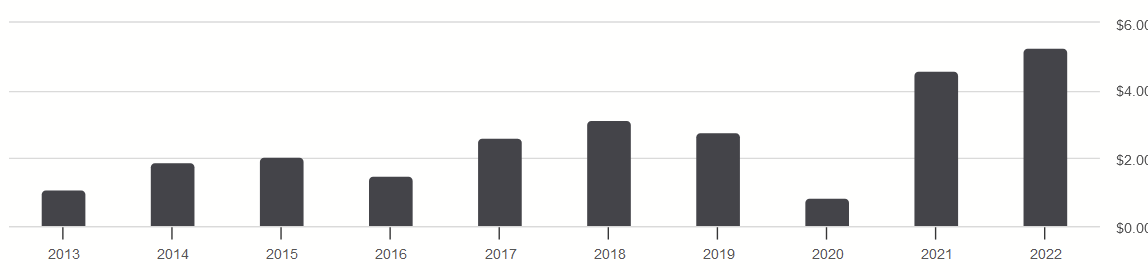

We see above that the dividend history is often not steady on a monthly basis. COVID disrupted market so much that dividends fell to near-zero and cannot be seen on the chart. Still, broken down yearly, we actually see that the dividend was up from the fund’s inception in June 2013:

Seeking Alpha

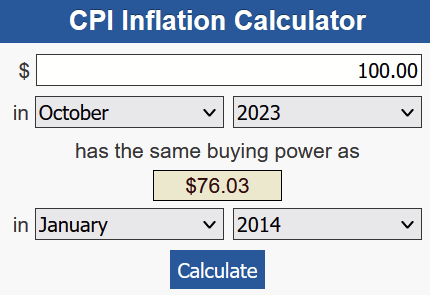

The first full-year dividend rate in 2014 amounted to $1.89. With $100K invested, that would have been $1,890 in annual income. Most of 2023’s monthly payments have been made, and if we assume XYLD’s December 2023 distribution will be at least $0.30 per share, then 2023’s income on that same capital will total $4,160.

Bureau of Labor Statistics

Based on the Bureau of Labor’s inflation calculator above, anyone who bought in January 2014 saw their purchasing power decrease by about 24% to the current day, so adjusting for that means real income grew to about $3,161.60, which is 1.67x. That isn’t bad per se, but we still need to grasp more than what the raw history tells us.

The Sources of the Income

XYLD is labeled a covered call ETF, but is that all there is to it and its monthly dividends? Global X indicates in its own fact sheet:

The Fund typically earns income dividends from stocks and interest from options premiums. These amounts, net of expenses, are typically passed along to Fund shareholders as dividends from net investment income. The Fund realizes capital gains from writing options and capital gains or losses whenever it sells securities. Any net realized long-term capital gains are distributed to shareholders as “capital gain distributions.” XYLD collects dividends from the S&P 500 Index companies and monthly options premium from selling single index options on companies in the S&P 500 index, and portions have been passed to shareholders as monthly distributions. Portion of the distribution may include a return of capital. These do not imply rates for any future distributions. The ETF is not required to make distributions.

This sheds a lot of light on the matter. In case folks had ever wondered what happens to the dividends the fund earns from its stock position, yes, those are passed through to shareholders, so part of XYLD’s income at any given point in time is from that.

Dividend Portion

So we know that XYLD’s income is based on the dividend distributions from its stock holdings and the premiums from its SPX call writing. Let’s talk about the dividends that XYLD receives first.

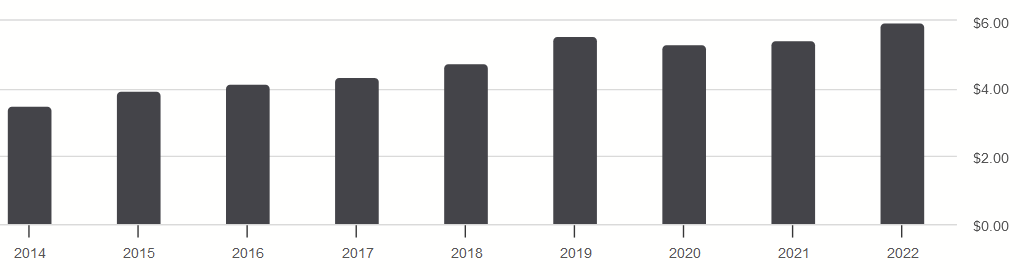

We can look at another fund that is modeled just on the S&P 500. I chose the Vanguard S&P 500 ETF (VOO). Its dividend rate has grown as well over this same time period.

Seeking Alpha

This is just based on the dividends of the companies in the index that are distributed into the fund. We see that they rose during this period. It’s unsurprising, since earnings of the index generally grew during that period. Higher earnings means higher dividends for shareholders, after all.

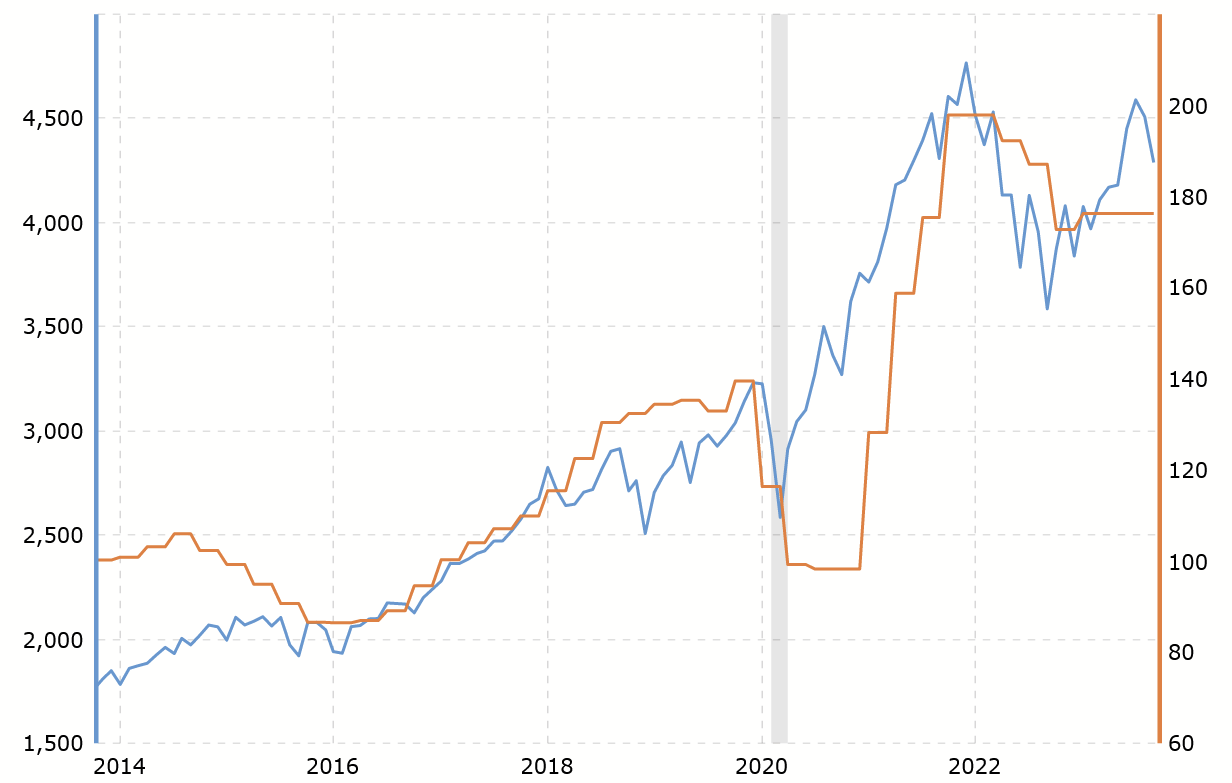

Macrotrends.net

Therefore, some of XYLD’s dividend growth will be a natural product of this. If earnings decrease, then it holds that dividends for the S&P 500 would also decrease, which would affect funds admire XYLD and VOO.

Covered Call Portion

Assessing this is trickier because it’s not income based on organic cash flow from the underlying companies in the index. Rather, it’s a consequence of trading. The premium of an options contract is a type of sale, and any income from this will depend on the fund’s ability to produce net-positive cash from these sales over the long run. That is going to depend on the price that traders are willing to pay for call contract.

Unlike earnings and dividends, this isn’t necessarily rooted in some kind of measurable, consistent business model or economic activity. It will depend a lot on the mood of traders in the short-term, but we’re trying to get a finger on whether or not XYLD is good for long-term income. I think we have one way of gauging that, though.

Fidelity.com

This shows the quote for calls at a strike price of $4,600 that expire Jan. 19, 2024. The premium is at $82, which is about 1.8% of the index value. When buying or selling calls, traders are essentially betting how much the underlying index will proceed, and they tend to do this based on percentages (since that’s how investment returns are measured). Therefore, as the underlying index grows, the premiums for its options contracts will grow. If the index doubles, then 1.8% goes from $82 to $164.

The Future of XYLD’s Income

I believe the historical data I’ve shown make the following assumptions valid:

- As the S&P 500’s earnings grow, so do the dividends of its companies.

- As its earnings grow, so does the value of the index.

- As the value of the index grows, so do call premiums.

- Long-term growth of the index leads to long-term growth of XYLD’s income.

- Similarly, long-term refuse or stagnation would mean long-term refuse or stagnation of XYLD’s income

If we accept those assumptions, we just need to carry out what’s more likely to happen, going forward.

I believe that a fund admire XYLD will most likely be stagnant, over the next 8 – 10 years. I don’t think 1.67x growth of real income is as likely as it was for someone who bought at the start of 2014. When we look at the context in which the S&P 500 grew (and thus XYLD’s income), it’s easy to grasp why.

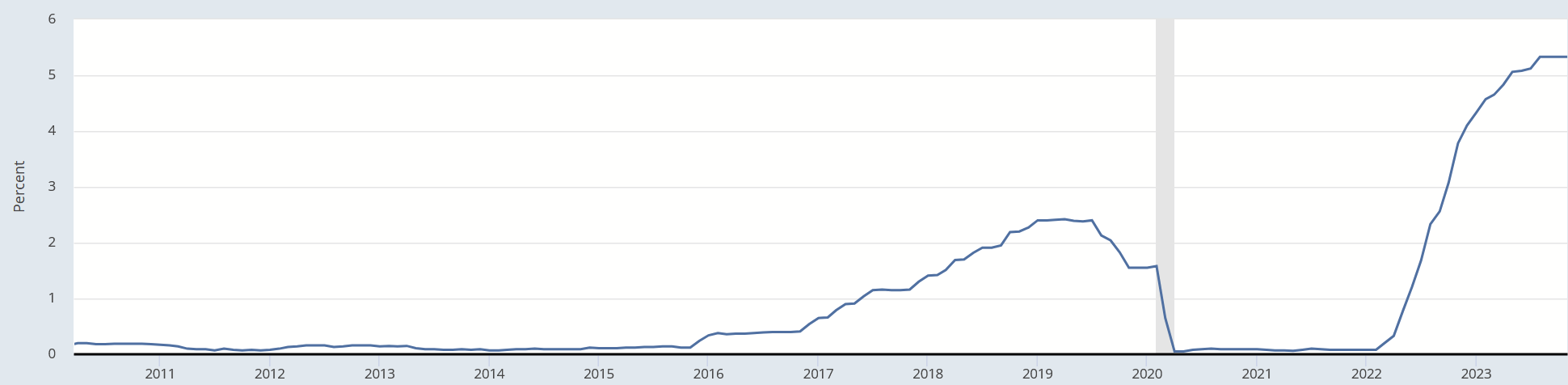

Federal Funds Rate History (fred.stlouisfed.org)

We can see that interest rates were near-zero for a very long time in the aftermath of the Great Recession. It was in that context of cheap capital that the S&P 500 was able to grow so much. As we have seen, interest rates are much higher now and were hiked at one of the fastest rates in history.

With higher rates for the foreseeable future, I think this is going to stagnate earnings, dividends, index value, and call premiums. A fund admire XYLD will become more attractive as we achieve the other side of that hump.

Then, of course, short-term aberrations (admire COVID in 2020), can cause XYLD’s monthly payments to collapse to near-zero for several months, so that’s still important to recollect.

Conclusion

With all that said, XYLD is not a bad ETF to hold, especially if investors have other income sources in their portfolio to balance the impact of higher interest rates to a fund admire this and provided that they are okay with purchasing power remaining flat or slightly declining down the road. In other words, I don’t think it’s an income fund that will completely dry up or become a 1% yield on cost (with the current yield being over 10%).

This also assumes that they are okay with the fact that it is not obligated to make distributions (which were heavily reduced during the COVID lockdowns).

Yet, those looking to enter an investment will probably want a more optimistic story than that, and with said interest rates making money market yields somewhat high in the meantime, it probably won’t hurt them to spend more time searching elsewhere for something more attractive.

Q2 2024 Earnings Call Transcript")