HECTOR RETAMAL/AFP via Getty Images

Li Auto Inc. (NASDAQ:LI), through its subsidiaries, designs, develops, manufactures, and sells new energy vehicles in the People’s Republic of China.

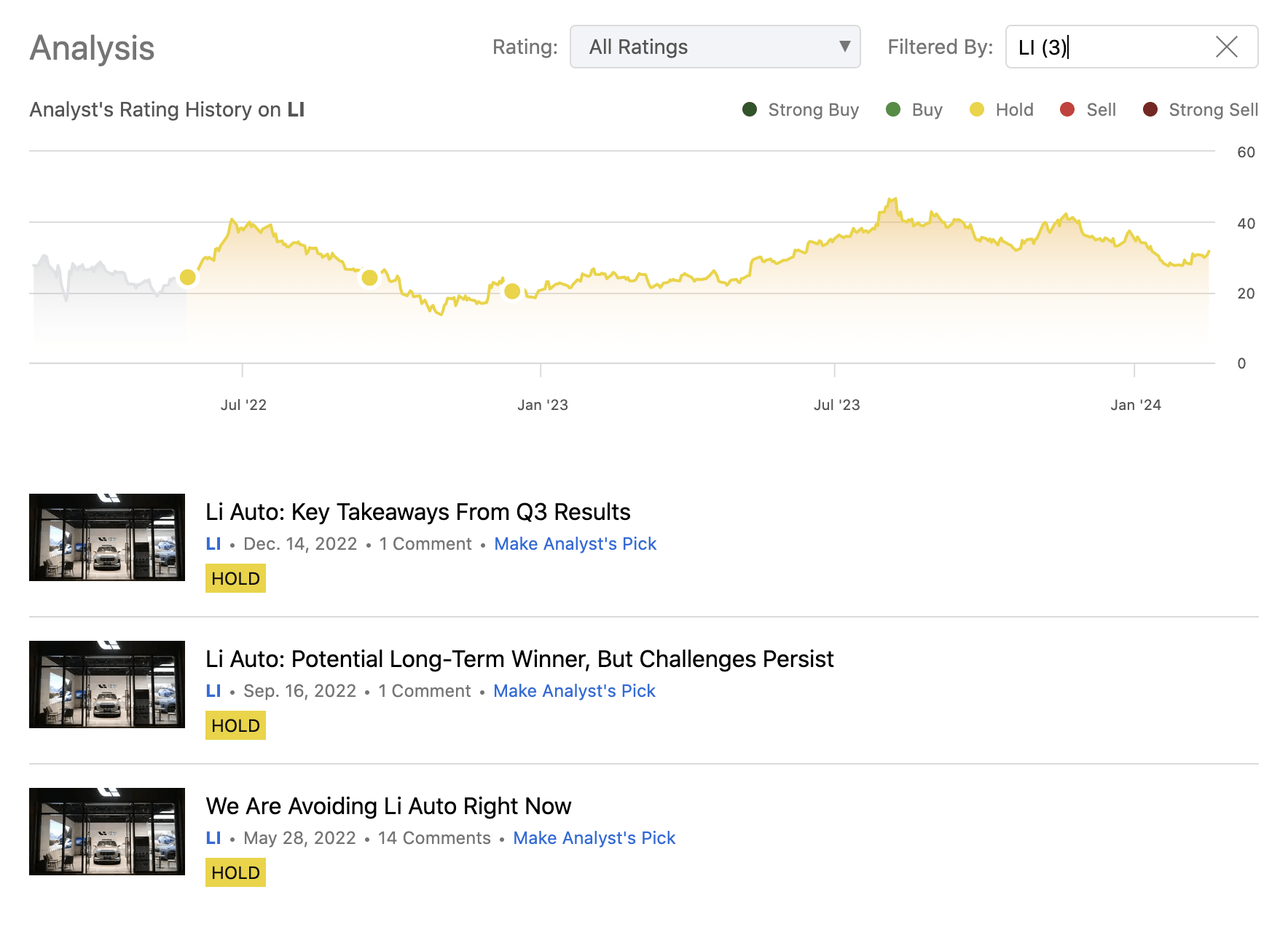

So far, we have published three articles on the firm, namely:

Li Auto: Key Takeaways From Q3 Results

Li Auto: Potential Long-Term Winner, But Challenges Persist

We Are Avoiding Li Auto Right Now

Analysis history (Author)

In each of these writings we have pointed out the attractive long-term potential of the firm, but every time we have believed that the uncertainty around the firm itself, around China, around the global macroeconomical environment is too high and therefore we have eventually never assigned a bullish rating to Li.

Now, since more than a year has passed, and both the company and the macroeconomic environment has gone through significant changes, we have decided to revisit Li Auto, and give our readers and update view.

To start our article, we will be focusing on the firm itself. We will be looking at profitability and efficiency measures and how they have changed over the past year. Alongside, we will be commenting on the broader economic environment and its likely impact on these measures. Finally, we will look at the development of the company’s valuation over the past year.

Deliveries

Let us first take a look at how the number of deliveries have changed year-over-year. According to the latest figures, released in early February, the number of deliveries have reached 31,165 in January, representing a 105.8% increase Y/Y. The aggressive growth of the firm is not only visible in the number of vehicles delivered, but also in their ambitions of expanding the model line up and the sales network.

2024 will be an unprecedented year of growth for us, and we will establish a portfolio of eight competitive models, […] A comprehensive upgrade of our sales and servicing network is also underway, with an aim of establishing 800 retail stores and over 500 Li Auto-authorized body and paint shops by the end of 2024.

All in all, we believe that Li Auto is making the right steps to capture market share and increase its customer base. But just as a year ago, there are external market forces that are creating significant headwinds not just for LI, but also for most Chinese EV makers. We have to highlight here the concern with regard to deflationary forces in China, the pricing battle between the largest competitors, apparent overcapacity of the EV makers. All of these factors can have a significant impact on Li’s top- and bottom-line results in the coming quarters.

For these reasons, based solely on the aggressive growth and expansion, we still do not feel confident allocating a meaningful percentage of our assets to Li’s stock.

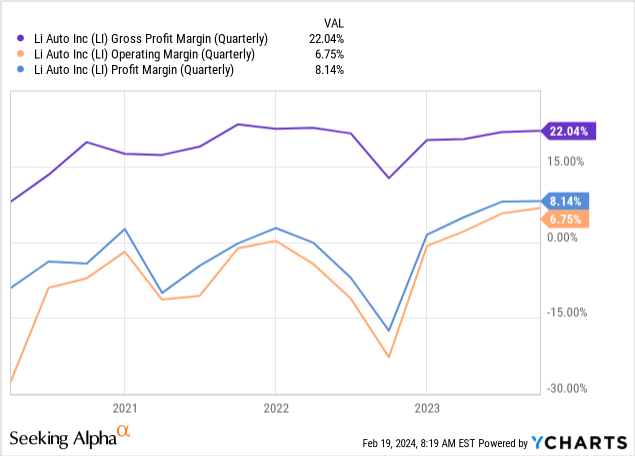

Profitability

The three most widely used profitability measures are the gross margin, operating margin and net income margin. The following chart depicts, how these margins have been evolving over the past years.

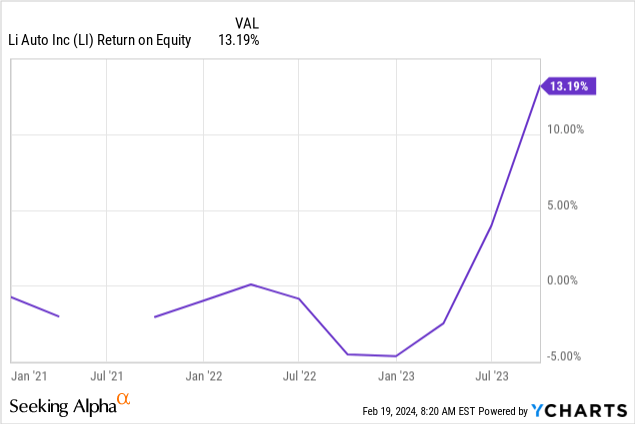

Despite the drop in the profitability around the end of 2022, Li Auto has continued to improve its profitability in the last four quarters. As a result, the firm’s return on equity measure has also started to improve significantly.

In the latest quarterly earnings report, the firm has elaborated on the margin expansions:

Gross margin was 22.0% in the third quarter of 2023, compared with 12.7% in the third quarter of 2022 and 21.8% in the second quarter of 2023. The increase in gross margin over the third quarter of 2022 was mainly attributable to the increase of vehicle margin.

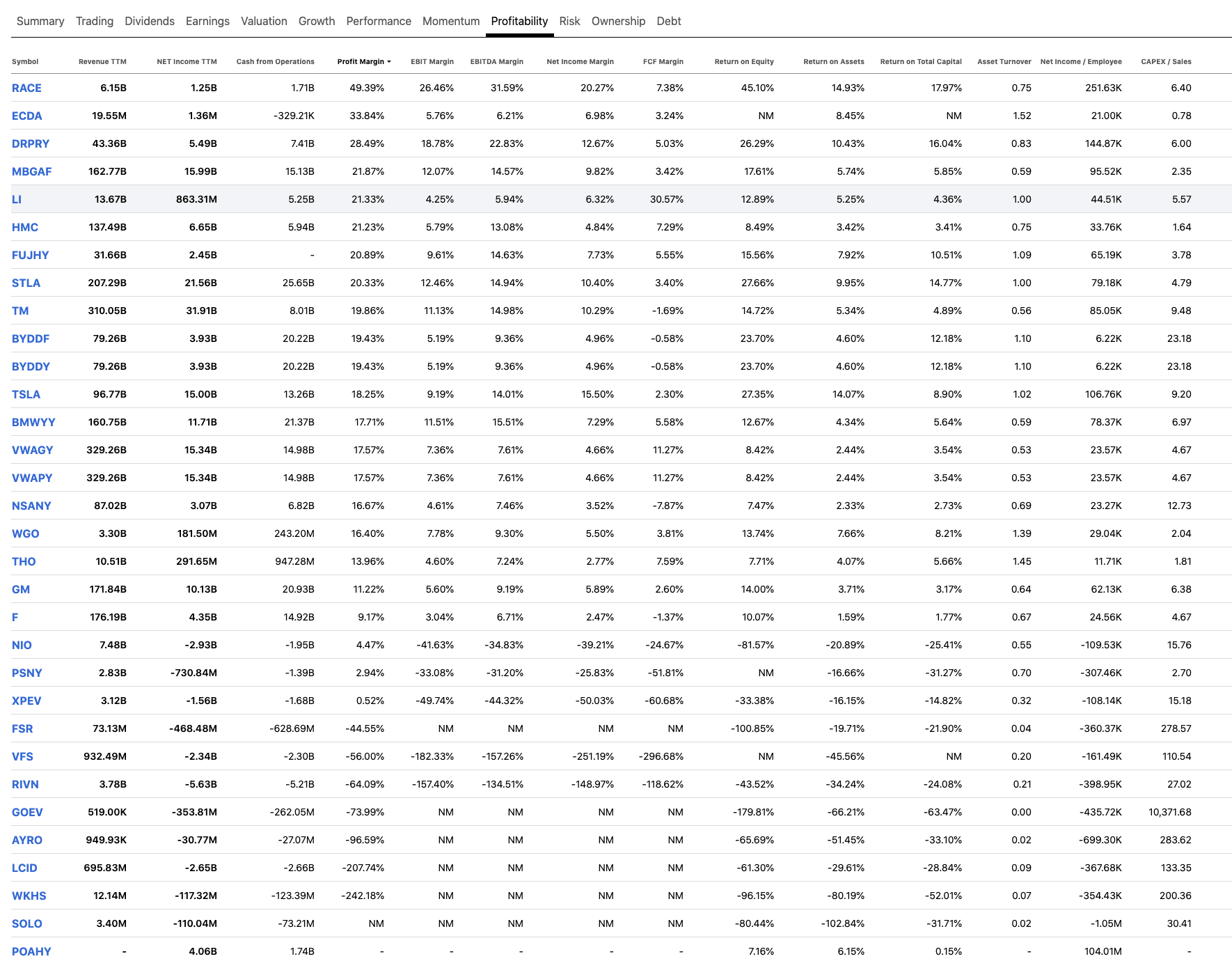

The following table shows how LI’s profitability measures compare with those of companies in the same industry.

Comparison (Seeking Alpha)

All in all, we are pleased with the significant expansion of the margins and the improved profitability. However, as mentioned earlier, the pricing battle between the largest competitors and the apparent overcapacity of the EV makers in China, could rapidly change this picture. At this point, we believe it is difficult to assess the likelihood of a government intervention to moderate overcapacity, therefore, despite the strong and steadily improving profitability measures, we cannot forecast the margin development over the near term with any certainty.

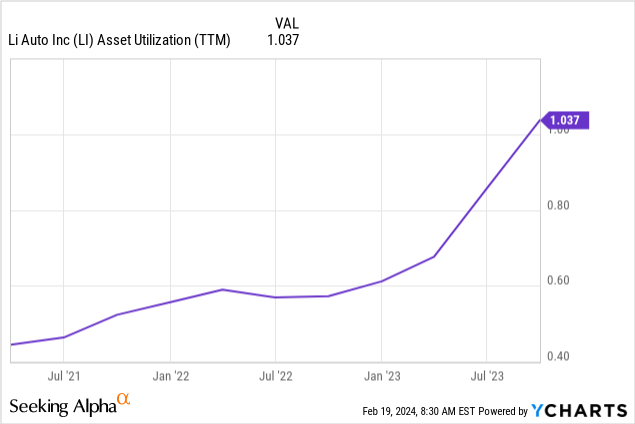

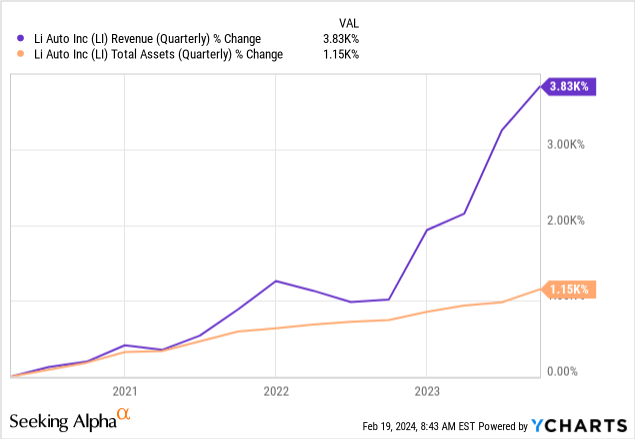

Efficiency

One of the most popular efficiency measures is the asset turnover/asset utilization. It is defined as sales divided by total assets. The following two charts show how the asset turnover has developed over the past years and how the sales growth has significantly outpaced the growth in total assets.

Just like from a profitability point of view, we also like the company’s development and improvement from an efficiency point of view.

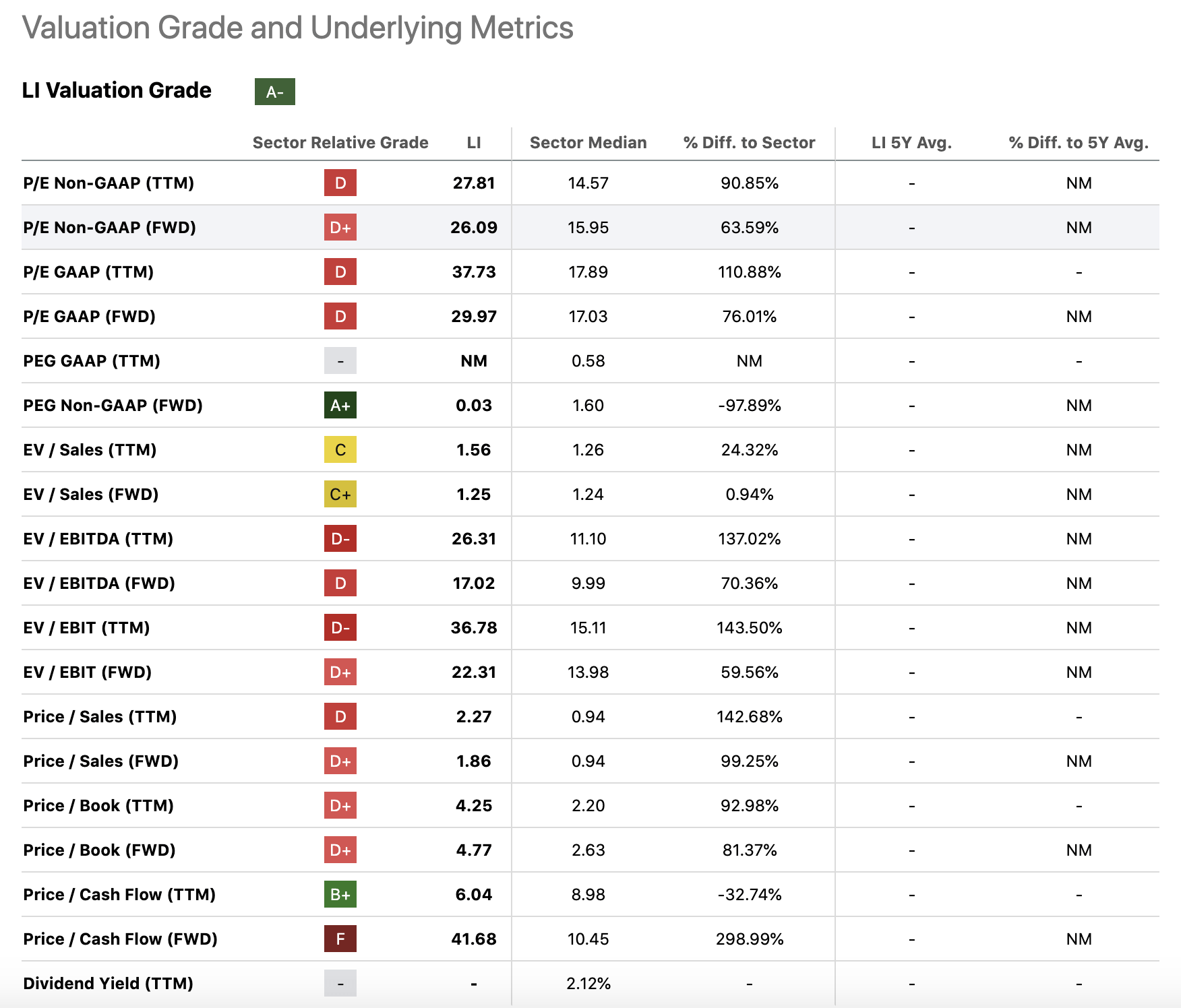

Valuation

Today, we will be using a set of traditional price multiples to determine, whether the current stock price could be an attractive entry point or not. The following table summarizes these metrics.

Valuation (Seeking Alpha)

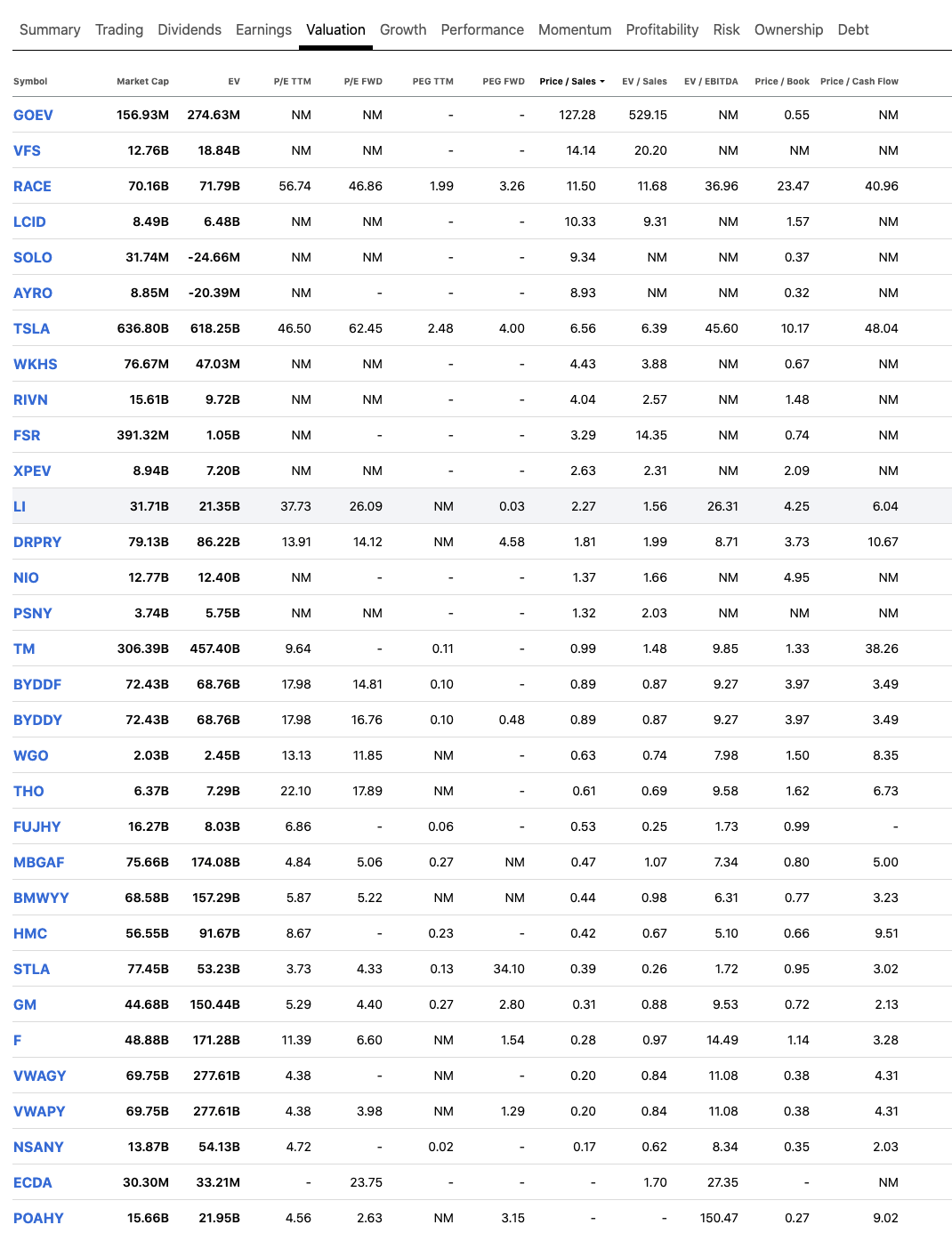

When looking at the table first, one may think that LI’s stock is significantly overvalued. However, before jumping to conclusions too quick, we have to understand that the comparison to the consumer discretionary sector median may not be the most appropriate choice, as it contains companies whose businesses are significantly different from LI’s. Therefore, it is important to narrow our peer group to the automobile manufacturers industry. The following table summarizes the valuation of the firms in the industry.

Valuation (Seeking Alpha)

As many of the EV makers are not yet profitable, we have decided to sort the firms by their price/sales ratio. Based on this list, LI appears to be more attractively priced than most of its direct competitors, including Tesla (TSLA), Lucid (LCID) or Rivian (RIVN).

Considering the firm’s aggressive growth, its outstanding profitability and rapidly improving efficiency, we believe that the valuation is reasonable and justified. On the other hand, despite the attractive valuation, we would only start a small speculative position, due to the high uncertainty surrounding the macroeconomic environment in China.

Conclusions

The firm has remained committed to its aggressive growth strategy and, as a result, deliveries have increased significantly year-over-year.

The profitability of the firm has also improving meaningfully, along with its efficiency as measured by the asset turnover.

The valuation of the firm in relation to those of its direct competitors seems reasonable and justified.

The macroeconomic situation in China, including the deflationary forces, the overcapacity of the EV makers and the pricing battle between competitors, are likely to create headwinds and potentially downward pressure on the margins in the coming quarters.

For these reasons, we do not feel comfortable improving our previously established rating. We maintain our “hold”.

Q2 2024 Earnings Call Transcript")