Hispanolistic

VistaGen Therapeutics, Inc. (NASDAQ:VTGN), established in 1998 and headquartered in South San Francisco, California, is developing a pipeline of Central Nervous System [CNS] drugs with the potential to innovate the treatment for serious anxiety, depression, and other CNS disorders. VTGN’s lead candidate, Fasedienol [PH94B], is progressing in phase 3 of the clinical trials, and it presents advantages over similar therapies as a non-systemic, low-abuse anxiolytic that aspires for Breakthrough Therapy Designation [BTD]. My valuation analysis has some important caveats that investors need to consider, but I overall deem VTGN a reasonably good “buy” at these levels.

Mental Health Focus: Business Overview

VistaGen Therapeutics, Inc. is a clinical-stage biopharmaceutical headquartered in California that focuses on developing novel treatments for psychiatric and Central Nervous System [CNS] disorders. Essentially, investing in VTGN is a bet on developing new-generation medicines for mental health disorders, and its key product candidates today are social anxiety disorders and menopausal hot flashes.

The company’s pipeline includes drugs in clinical trials, such as an oral antagonist of the glycine site of the N-methyl-D-aspartate receptor [NMDAR] and drugs belonging to the Pherines family. NMDARs are essential for synaptic transmission and brain plasticity, offering a therapeutic mechanism for treating depression, schizophrenia, and neurodegenerative diseases. Likewise, Pherines are new drugs that target nasal chemosensory receptors to modulate neurological functions with reduced side effects. This approach is relatively more promising than current market alternatives that tend to cause dependency or unwanted health concerns, so VTGN’s approach could prove more beneficial. However, as of today, only VTGN’s Fasedienol is the closest to FDA approval, so proving these potential benefits remains to be seen.

Source: VistaGen Corporate Presentation 2024.

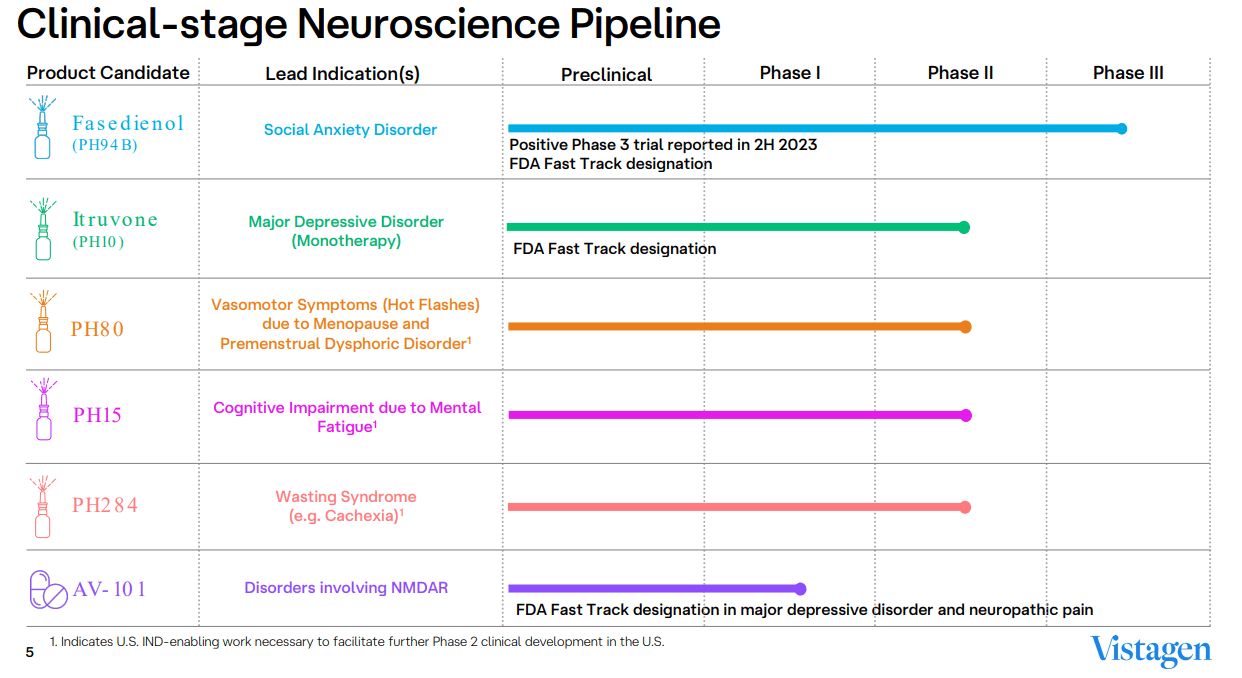

Therefore, VTGN is actively working on 1) Fasedienol [PH94B], 2) Itruvone [PH10], 3) PH80, 4) PH15, 5) PH284, and 6) AV-101. Fasedienol remains the most promising as it’s currently in Phase 3 with an FDA Fast Track Designation for treating social anxiety disorders [SAD]. Itruvone is in Phase 2 for treating major depressive disorder. PH80 treats menopause vasomotor symptoms, also in Phase 2, but currently needs further IND-enabling studies. PH15 targets cognitive impairment from mental fatigue, and PH284 targets cachexia. Both of these are also in Phase 2. Lastly, AV-101 treats NMDAR-related disorders but is still in early Phase 1 stages but with a Fast Track Designation for major depressive disorder and neuropathic pain. Overall, I think this is a diverse product portfolio pipeline, but from an investment perspective, the main value driver will likely be Fasedienol for the foreseeable future.

Source: VistaGen Corporate Presentation 2024.

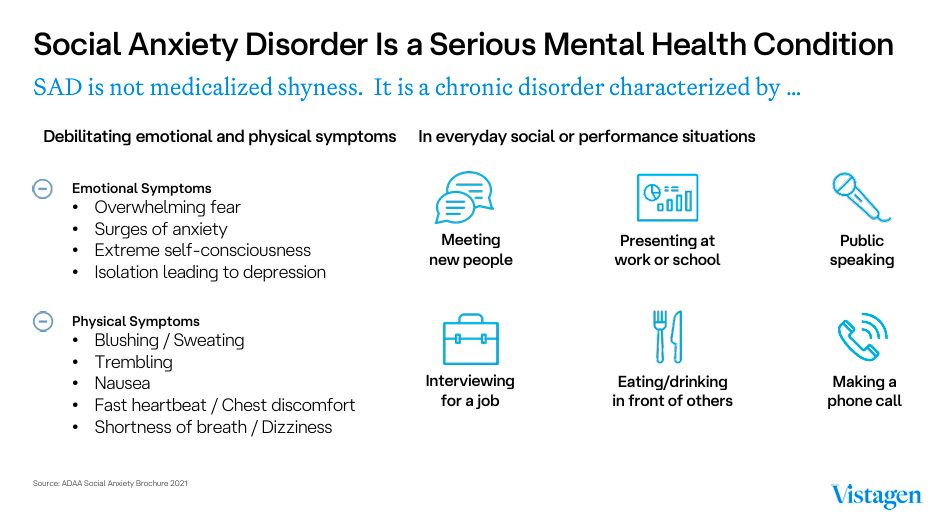

Moreover, VTGN’s Palisade-2 Phase 3 study of Fasedienol gave positive results for SAD treatment in 2H 2023. The drug is administered intranasally and connects to neurons in the limbic amygdala affected by the pathophysiology of SAD and possibly other mood disorders. The drug activates its action without systemic absorption to reach a rapid but short-duration anxiolytic effect. These aspects are useful in acute anxiety episode treatment as they provide quick relief without interfering with daily activities.

Fasedienol and Transformative Care

In the future, VTGN aspires to receive a Breakthrough Therapy Designation [BTD] for Fasedienol from the FDA, acknowledging it as a notable improvement over other therapies. This recognition will expedite the drug’s development and review process. Furthermore, Fasedienol’s non-systemic nature and low potential for abuse due to its action mechanism that doesn’t activate the brain’s reward system or potentiate GABA are important characteristics given the problems that medications like benzodiazepines have shown. With these antecedents and based on the data, Fasedienol may not need to be scheduled as a controlled substance, increasing patient accessibility.

This would have significant implications and give the medication an important market differentiation as an effective anxiolytic non-controlled substance. Correspondingly, the drug will not have to go through the complex and time-consuming scheduling process for controlled substances, leading to a faster path to market. In fact, because of its lower risk of abuse, Fasedienol would face fewer prescribing restrictions as well. These factors open and expand Fasedienol’s market access, likely leading to higher revenue potential if successfully developed and commercialized.

Source: VistaGen Corporate Presentation 2024.

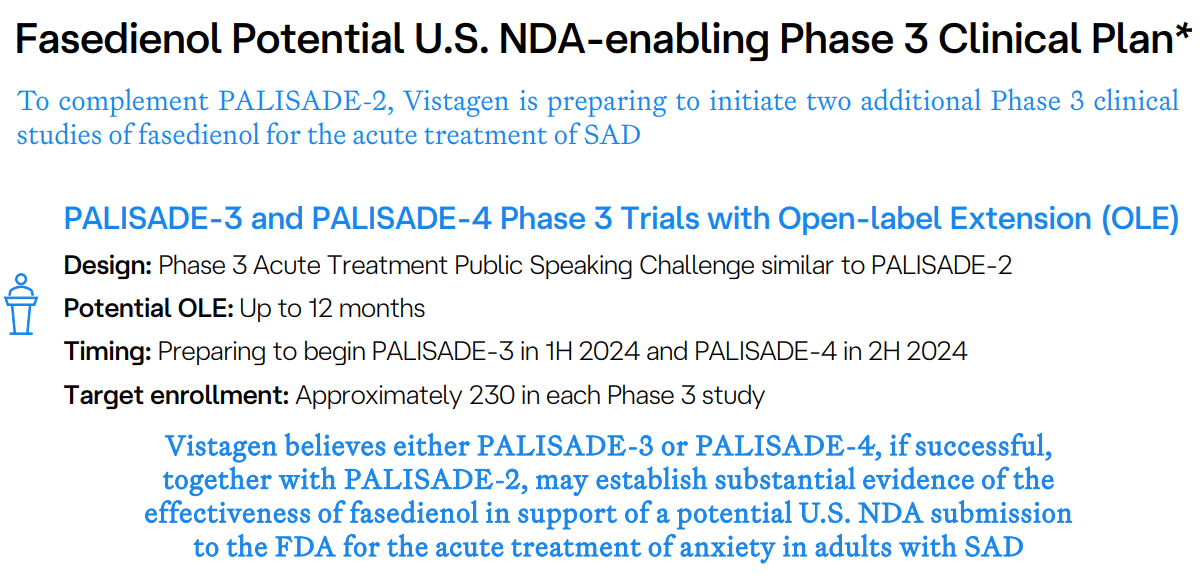

Palisade 2 was a clinical trial in Phase 3 for Fasedienol. It achieved its primary, secondary, and exploratory endpoints. In the primary point, the treatment was more effective, with fewer subjective units of distress scale [SUDS] than placebo. The secondary point was also met, with the Clinical Global Impression Improvement scale [CGI-I] proportion of more participants less anxious from visit 2 to visit 3. This evaluation serves to rate the seriousness of the illness and the changes it has over time.

In total, the exploratory endpoints that were satisfied were the Patient’s Global Impression of Change [PGI-C] to indicate the proportion of responders versus placebo that felt much less anxiety. Palisade-3 and Palisade-4 are planned for 2024. The results for Palisade 2 are leading to a successful pathway to regulatory approval, which enhances investor confidence and gives a strong foundation for the clinical and commercial future of Fasedienol.

Source: VistaGen Corporate Presentation 2024.

During the last earnings call, VTGN’s executives noted that the financial results show a strong cash position, decreased R&D expenditures, and increased general and administrative expenses due to compensation-related expenses. They also highlighted that VTGN is focused on advancing its clinical trials. Overall, Fasedienol remains the main R&D focus touchpoint of R&D expenditures, as SAD has significant market potential if addressed correctly.

Looks Reasonable: Valuation Analysis

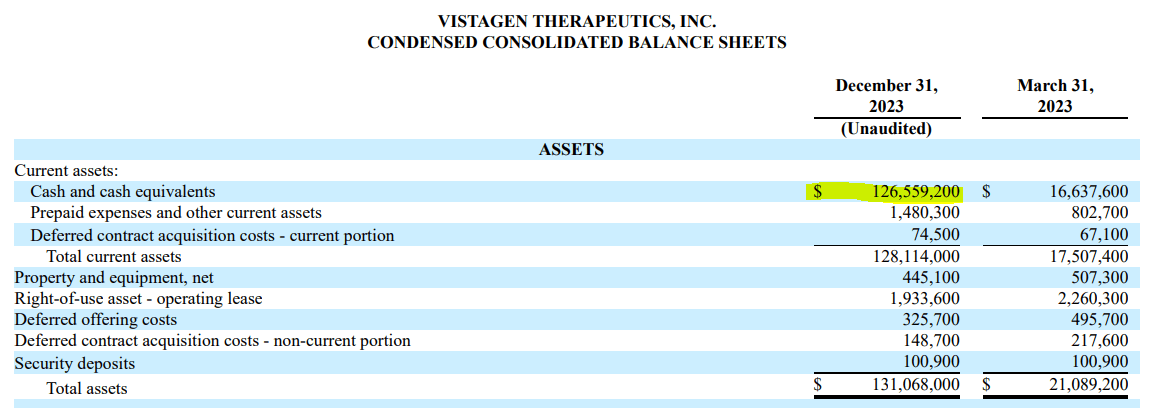

From an investment perspective, I estimate that VTGN burned through roughly $4.5 million in Q4 2023. I obtained this figure by adding up its latest CFOs and Net CAPEX. If we annualize this burn rate, we get a yearly cash burn of $18.0 million. VTGN holds $126.6 million in cash and just $2.3 million in debt today. So this implies a cash runway of about $7.03 years at the current cash burn rate, which should be more than enough to get through with all the necessary FDA trials for Fasedienol, at the very least. Moreover, assuming the company obtains the required FDA approvals, I imagine that financing will become much easier if needed for VTGN. Thus, I believe the company has enough resources to see through with its current product portfolio.

Moreover, after the recently filed S-3 document, VTGN appears to be gearing up to raise additional funds. I speculate this is a preliminary move to finance its IP commercialization initiatives as soon as it gets FDA approval. The terms are flexible, such as equity, preferred stock, debt, or a mix of these. Plus, to the extent that dilution happened, it also seems to be priced into the stock to some extent. The filing occurred on February 13, 2024, and the shares traded at $4.90 that day. Today, the shares trade at $4.05 per share, but the shares have traded in the $4 to $5 price range since December 2023, so I don’t think the market is too concerned by this filing. Personally, I don’t believe dilution is imminent as debt is a perfectly viable alternative mentioned in the document (assuming FDA approvals occur). This seems like a reasonable interpretation based on the overall market’s reaction to the announcement.

Source: VTGN’s latest 10-Q report.

Hence, today’s most interesting aspect of the stock’s valuation is that it trades below its latest reported cash value! Its market cap is roughly $106.0 million, trading at 83.7% of its latest reported cash balance. Naturally, the latest report was for Q4 2023, so it’s likely that the company holds less cash than that figure today. Still, it’s fair to say that its market cap is roughly in line with its current cash value. In my view, this excludes all the potential value that can come from its promising intellectual property, so I believe it’s fair to say VTGN is a reasonable buy at these levels on that argument alone. I think its current valuation simply does not fully account for VTGN’s potential.

Investment Caveats

Naturally, my “buy” rating on VTGN has some caveats. Concretely, I think that 1) regulatory risks remain, 2) market adoption is still speculative at this early stage, and 3) the S-3 filing could indeed lead to stock dilution if management chooses that financing alternative. Nevertheless, I believe that, for the most part, these risks are already priced in. After all, the market has been aware of VTGN’s regulatory risks for years, so this is not surprising for investors. As for market adoption, I would argue that to the extent that these risks become relevant, it also means that FDA approvals occurred because today, the main concern revolves around actually getting FDA approvals before proceeding with commercialization efforts.

Lastly, even if the S-3 filling leads to stock dilution, current investors would become owners of a smaller equity percentage of a highly capitalized entity with ample cash resources to proceed with commercialization efforts of any of its potentially approved IPs (likely Fasedienol). This is because I doubt the company will proceed with a significant cash raise just to finance ongoing cash burn, as they already have an ample liquidity runway today. If they raise additional funds, it’ll likely be used to finance production and commercialization efforts.

Source: TradingView.

Conclusion

Overall, VTGN looks like a well-positioned company that is quickly getting closer to pivoting into production and commercialization efforts after getting FDA approval on its product pipeline. Fasedienol in Phase 3, with promising results, could promptly become its flagship product. The valuation equation is nuanced, as we have to acknowledge the possibility of stock dilution in light of the recent S-3 filing. However, since the stock already trades today below its latest reported cash value, and considering that any dilution will likely be to fund commercialization efforts, it overall seems to justify a “buy” rating today. Naturally, some investors might prefer to wait until after dilution occurs (if it happens). Still, I suspect this would only ensue after meaningful regulatory approvals are obtained because VTGN already has more than enough cash runway at the current cash burn rate. Hence, I think that, on balance, VTGN is a good “buy” at these levels for investors who are aware of the ongoing dynamics at play.

Q2 2024 Earnings Call Transcript")