Don’t count on the roughly $6 trillion wall of cash sitting in money-market funds to bolster the stock market, according to Joseph Kalish, chief global macro strategist at Ned Davis Research.

Kalish thinks the popular argument that “cash on the sidelines” can be bullish for stocks sounds more like “propaganda” at this point, especially when looking at 40 years of historical data for the money-market industry.

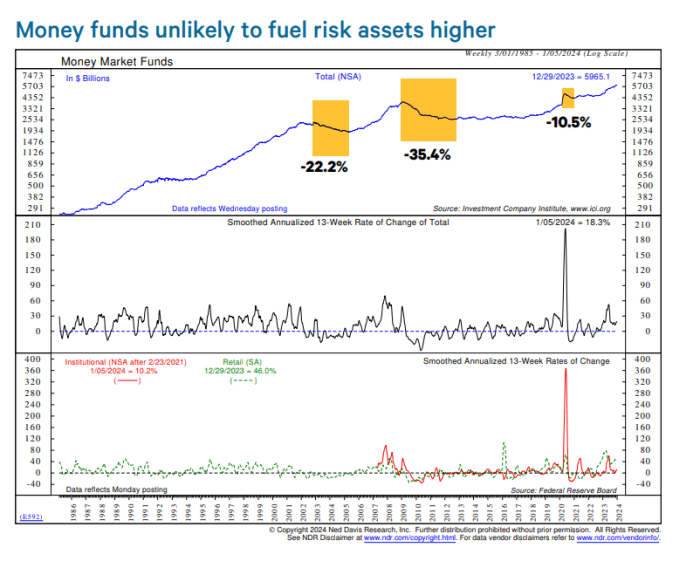

“Has anybody bothered to check the record?” Kalish asked, in a Thursday client note. “We have and here’s what we found.”

The NDR team found three meaningful declines in money-market fund data in the past four decades, with the biggest drop of 35.4%, or $1.4 trillion, unfolding a dozen years ago in the post-global financial crisis era.

Don’t count on the surge in assets into money-market funds to prop up stocks, according to Ned Davis Research

Ned Davis Research

Other significant periods of declines for money-market assets were the 22.2% drop following the technology stock bubble bursting in the early 2000s and the 10.5% decrease in 2020 during the pandemic.

Of note, all three past periods of declines coincided with Federal Reserve moves to ease monetary policy while bolstering the economy, motivating investors to move money out of cash into higher-yielding assets, according to Kalish.

Money-market funds raked in roughly $1.4 trillion over the past year, according to NDR data.

Importantly, these past declines in money-market assets came after big bear-market moves in equities that enticed investors back into stocks and out of cash.

“Neither condition is present today,” Kalish wrote, especially with money-market funds kicking off 5% or more, and equities near record highs.

The S&P 500 index

SPX

on Thursday briefly traded intraday above its prior closing record set roughly two years ago. After big gains in the fourth quarter, the Dow Jones Industrial Average

DJIA

also rose to a series of record closes.

See: S&P 500 briefly flirts with first record close in over 2 years. What’s next?

A resilient economy and a sharp retreat in the 10-year Treasury yield

BX:TMUBMUSD10Y

in the final months of 2023 provided a strong catalyst for stocks to rally. The benchmark rate, which finances much of the U.S. economy, briefly traded above 5% in October, but has since retreated to about 4%, providing a reprieve for borrowers needing to raise fresh debt or refinance.

“There are reasons to be bullish equities and even credit as we have

discussed in recent publications, but the pile of cash is a weak one,”

Kalish said.

Q2 2024 Earnings Call Transcript")