Equity bulls banking on a soft landing for the economy appear to be taking comfort in market-based expectations for the Federal Reserve to cut its key lending rate by around 1.5 percentage points in 2024.

Here’s the rub.

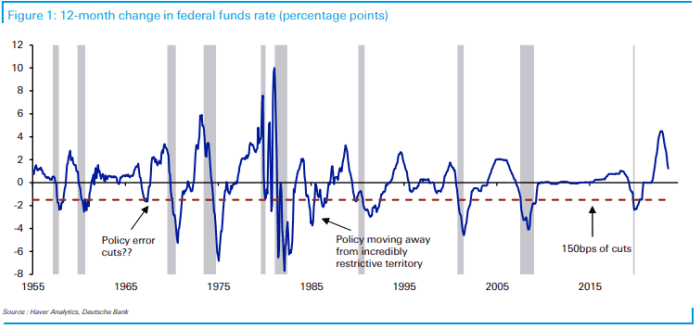

History shows the majority of the time the Fed has delivered 1.5 percentage points, or 150 basis points, of interest rate cuts within a year, “it’s been because of a recession,” observed Jim Reid, strategist at Deutsche Bank, in a Tuesday note (see chart below).

Blue line tracks rolling annual change in the federal-funds rate. Red dotted line equal to 150 basis points of cuts. Shaded areas mark U.S. recessions.

Deutsche Bank

Stocks staged a strong rally into the end of last year, with the Dow Jones Industrial Average

DJIA

scoring a number of record closes, while the S&P 500

SPX

saw a total return of more than 26% and ended the year just 0.5% away from its Jan. 3, 2022, record finish. Stocks have pulled back modestly to begin the new year.

The 2023 rally accelerated as investors priced in a Fed policy pivot to lower interest rates. Rates traders have scaled back expectations for cuts in 2024, but fed-funds futures still reflect a 53.8% probability the fed-funds rate will fall 150 basis points or more by December, according to the CME FedWatch tool.

As the chart shows, there was an exception to the recession outcome in the 1980s, when the Fed was headed by Paul Volcker. But, Reid notes, it came after the Fed had hiked rates into “super-restrictive” territory, which means it isn’t really comparable to the present situation.

The other exception came in the late 1960s, but was alongside a sharp rise in public spending due to the Vietnam War, he noted, with inflation picking up again shortly afterwards in what was seen in retrospect as a policy error. Moreover, “that’s precisely what the Fed wants to avoid happening again,” Reid said.

“So the historic precedent leans heavily towards the sort of rate cutting environment currently priced in being more associated with a recession than a soft landing,” he wrote. “If you don’t get a recession, history suggests the hurdle to 150bps over 12 months is high.”

Q2 2024 Earnings Call Transcript")