Shares in industrial conglomerate 3M (MMM 0.22%) declined by 8.9% last year, according to data provided by S&P Global Market Intelligence. The move comes down to a combination of deterioration in the company’s end markets, costly legal settlements that will drain cash for many years, and another year of disappointing operational performance.

Deteriorating end markets

There’s little management can do about deteriorating end markets. Unfortunately, 3M’s exposure to consumer electronics, automobiles, home goods, and other interest rate sensitive areas of the economy meant it came under pressure last year.

For example, the table below shows how the healthcare segment (to be spun off later this year) is the only one to report year-over-year organic sales growth so far in 2023.

|

Business Segment Organic Revenue Growth (YOY) |

First Quarter 2023 |

Second Quarter 2023 |

Third Quarter 2023 |

Full-Year Guidance |

|---|---|---|---|---|

|

Safety and industrial |

(6%) |

(4.6%) |

(5.8%) |

Down low single digits |

|

Transportation and electronics |

(8%) |

(1.3%) |

(1.8%) |

Down mid-single digits to flat |

|

Health care |

1.4% |

0.1% |

2.4% |

Up low single digits to mid-single digits |

|

Consumer |

(6.8%) |

(2.2%) |

(7.2%) |

Down low single digits to flat |

|

Total |

(4.9%) |

(2.2%) |

(3.7%) |

(3%) |

Data source: 3M. YOY = year over year.

Legal settlements and management’s guidance

The highly public legal issues will result in a cash drain for over a decade. According to CFO Monish Patolawala at an investor conference in November, the combat arms earplugs settlement “is a combination of $5 billion in cash and $1 billion in stock,” which will be paid over six to seven years. Meanwhile, 3M aims for “a settlement of $12.5 billion — $10.5 billion to $12.5 billion with a present value of $10.3 billion” to be paid over 13 years for its previous manufacture and use of PFAS chemicals.

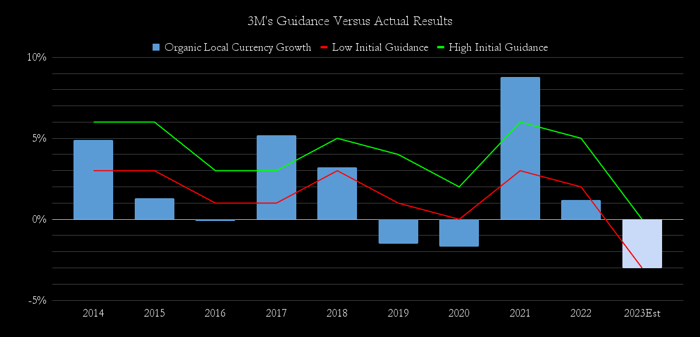

Lastly, 3M is on track to deliver organic sales growth right at the bottom of its initial guidance of flat to a 3% decline from 2022. As the chart below shows, this is not the first time management has disappointed investors. Indeed, a leading investor in the company wrote to 3M’s management in early 2023 expressing dissatisfaction.

Data source: 3M presentations. Chart by author.

3M in 2024?

With the negativity out of the way, it’s worth noting that there’s evidence that 3M’s restructuring actions are starting to improve its margin performance, and the stock trades on an excellent valuation, sporting a 5.5% dividend yield.

Image source: Getty Images.

That said, there are question marks around the sustainability of its dividend given the cash needed for legal settlements, the still weak end market backdrop, and the loss of cash flow from the healthcare spinoff in 2024. Cautious investors may want to hear from management on its 2024 outlook before buying in.

Q2 2024 Earnings Call Transcript")