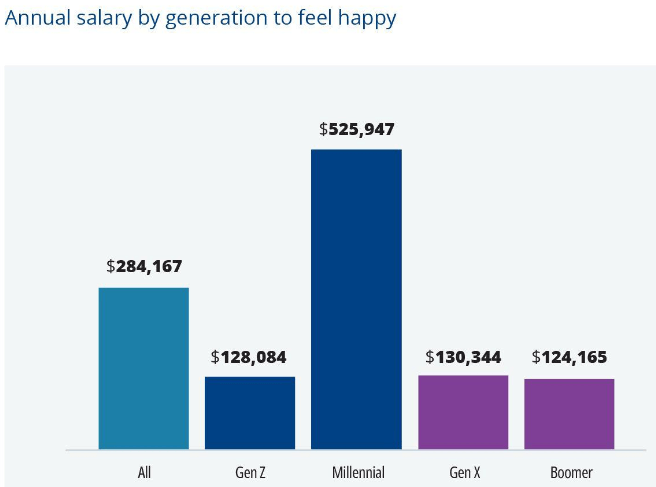

Empower surveyed 2,304 U.S. adults about financial happiness. And one of the most fascinating data points from the survey was that Millennials need to earn $525,000 a year to feel happy!

Although $525,000 isn’t a top 1% income ($650,000+ is in 2023), it’s a top 3% income. And if you need to earn more than 97% of the population to be happy, you might always be sad for the rest of your life!

The income figure across all age groups needed to be happy is $284,167 per year to be happy. Men say they need to earn $381,000 a year while women say they are happy with a much lower income of $183,000. Gen Z $128,000, Gen X $130,000, and Boomers $124,000, are much more realistic about their income needs for happiness.

Where did these surveyed Millennials come up with this $525,000 annual income figure? I think I know the answer.

Struggling To Keep Up On $500,000 A Year

Back in 2015, I wrote a viral post called Scraping By On $500,000 A Year: Why It’s So Hard To Escape The Rat Race. The post has been read or seen by just about everybody who is a personal finance enthusiast. We’re talking millions of views.

My goal for the post was to showcase how high-income households can often struggle to save for retirement due to lavish lifestyles, high tax rates, high housing costs, and the perceived need to keep up with the Joneses.

Back when I started Financial Samurai in 2009, most personal finance bloggers didn’t live in expensive coastal cities admire New York or San Francisco. Most still don’t. Therefore, I thought it would be worthwhile to supply insights into what potentially half the American population faces.

If you read the 600+ comments, you know the post generated a lot of backlash from readers who live on much less but save much more. They couldn’t believe how ridiculous some of the budget line items were. Most of the disgruntled commenters didn’t live in an expensive city. Nor did they have children.

However, eight years later, the backlash has died down because more people have realized the veracity of the post.

Raising children in a big city is expensive and energy-sapping. Tuition and housing costs have soared since 2015. Although the top federal marginal tax rate has declined from 39.6% to 37%, that’s still a lot, especially once you add on state taxes, city taxes, and FICA taxes.

Dear Millennials, My Bad For Making You Anxious!

My $500K post first created anxiety in readers because it made them fearful that what they are currently making might not be enough to retire comfortably. It doesn’t matter how much you make, you will never get ahead financially if you don’t control your spending and invest wisely.

My theory is that the post continues to be widely read and has created an expectation in the Millennial generation’s minds that earning $500,000+ a year is necessary to be happy.

While I tried to make amends with a new post that incorporated a more frugal budget, A $500,000 Redo: How One Couple Got Their Mojo Back, but by then, it was too late. It seems it wasn’t the high spending readers were mad about. Rather, it was their fixation on the $500,000 household income figure that was much harder to reach.

My bad folks!

I hope you achieve by now you don’t need to earn $500,000+ to be happy. You also don’t need generational wealth to raise a family either.

Instead, what you need is to earn enough to cover your basic living expenses while knowing that you are making financial progress in growing your net worth. Progress = happiness!

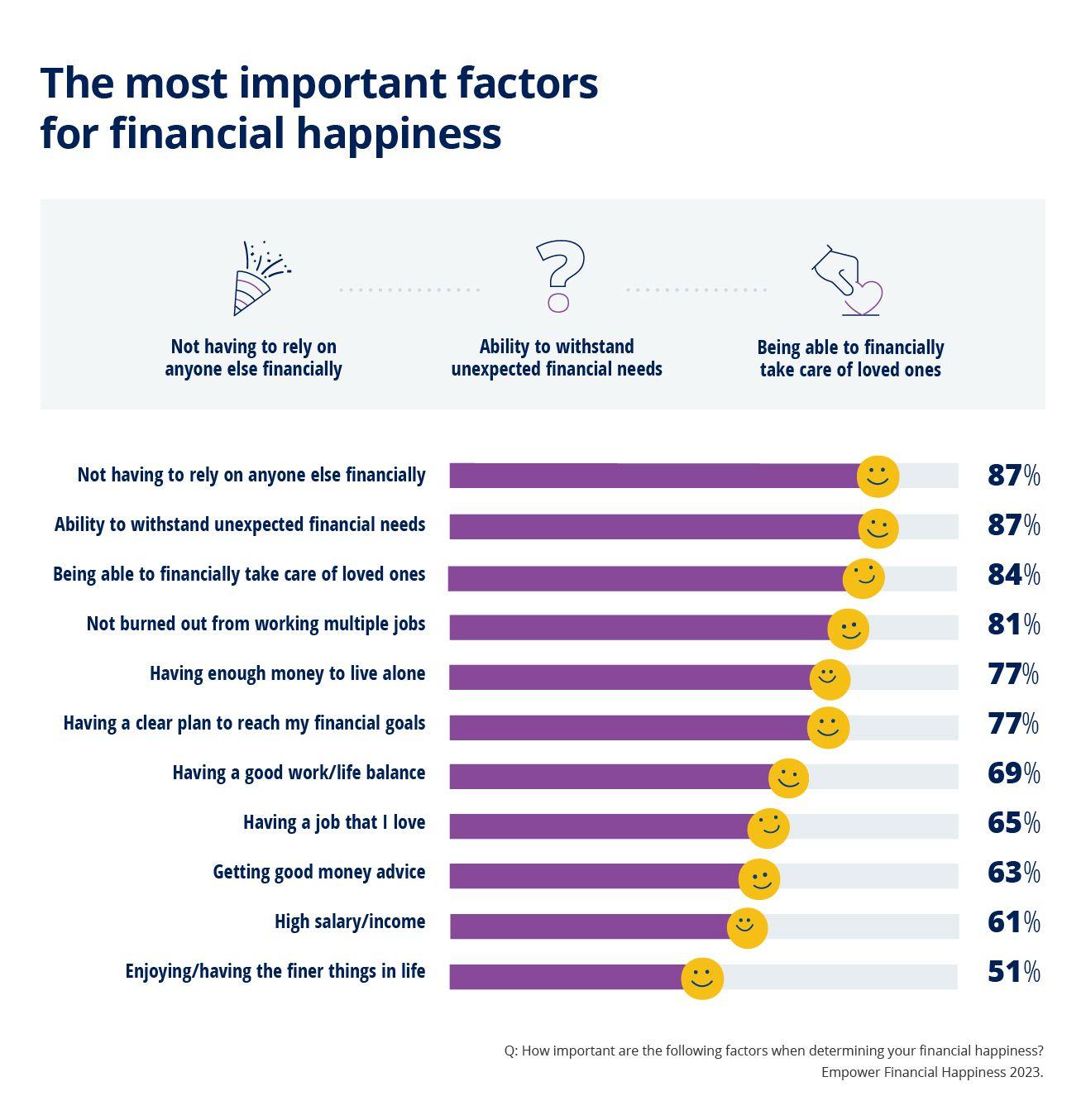

Here are the most important factors for financial happiness according to the survey.

Other Reasons For The Huge Income Requirement By Millennials

Why do millennials feel they need to earn 4X more money than Gen Xers ($130,000), Gen Zers ($128,000), and Boomers ($124,000) to feel happy? Besides Financial Samurai creating a warped sense of reality since 2015, here are some other reasons.

1) Perpetual economic crises

Millennials began their careers during the 2008 global financial crisis that resulted in millions of layoffs, a 50% refuse in the stock market, and a 30% refuse in the real estate market. Graduating during the deepest recession of our lifetimes can cause permanent damage to one’s earnings and career potential.

Then the pandemic came along in 2020 for two-to-three years followed by the highest inflation figures seen in decades. Now there is war in Ukraine/Russia and growing conflict in the Middle East. As a result, it’s only natural for millennials to feel they need to earn far more than other generations to be happy.

2) Ever-rising housing costs

Once you can fix your housing costs, life gets much easier. Since 2009, I have recommended readers get neutral real estate by owning their primary residence. By owning your primary residence, you get to benefit from housing inflation. By renting, you are hurt by housing inflation due to ever-rising rents and prices.

Those who disagree believe they will be able to consistently “save and invest the difference” in stocks and other risk assets to keep up or outperform. Unfortunately, due to economic leakage and human nature, the vast majority of people are incapable of consistently doing so. Buying a house with a mortgage acts as a forced savings account.

An opportunity to buy real estate today

There are essentially two-to-five-year windows of opportunity to buy real estate at more affordable prices every seven-to-ten years. We’re in this window of opportunity now, which I think will end by the Spring of 2025.

If you don’t get neutral real estate during this window, I’m pretty sure that in 2035, if you end up taking this survey then, you will cite housing costs as one of your key stressors.

If you can’t afford to buy a house today, then you can invest in real estate ETFs, public REITs, or private real estate funds as a way to get neutral the market. While saving for a down payment, if the real estate market rebounds aggressively, you won’t fall as far behind.

Roughly 42% of homeowners don’t have a mortgage and 80% of mortgage borrowers have a mortgage rate below 5%. Rising rates, although bad for home prices, are not squeezing existing homeowners as much as some might think.

Both Millennial and Gen Z survey respondents say they stress most about high housing costs (67%, 46%) and rising rent prices (62%, 38%).

3) Childcare costs are out of control

As a father of two young children, because I own my primary residence, my greatest concern is the cost of childcare. First, there’s the cost of diapers, strollers, food, clothing, medicines, and healthcare costs. Then there’s the cost of paying someone to watch your child if you have to work or need a break. Then there’s private grade school tuition (if applicable) and college tuition costs.

I’ve already estimated by the year 2035, the all-in cost of a four-year private university will be about $750,000 per child. I can hope my child gets a scholarship, attends public college, or goes to community college for free. But I can’t count on it and neither should you.

Feeling the heat of paying for college tuition

The challenge of paying for my children’s education is one of the reasons why I feel I should go back to work once my daughter goes to preschool full time in fall 2024. Not only will I have to pay for her preschool tuition, but I might also have to pay even more than $750,000 for her college in 15 years since she’s still only three!

Alas, my master strategize is to encourage them to go to community college instead. I’ve heard a lot of good feedback from readers who went to community college so I don’t see why my kids can’t go the same route as well and do fine.

If you want one parent to stay at home and raise your children, I can also see why Millennials think they need to earn over $500,000 to be happy.

Why Boomers And Gen Xers Feel More Financially ensure

Boomers ($124,000) and Gen Xers ($130,000) need lower income levels to be happy because they are more financially ensure. They’ve simply had more time to save, invest, and benefit from a bull market.

When I was 38 years old and wrote the post about scraping by on $500,000 a year, a part of me was wondering if that’s how much I really need to feel ensure and happy. I didn’t have kids yet, so I was carefully planning for when I did. The responsibility to raise children in an expensive city seemed daunting.

As a 46-year-old Gen Xer with two kids, I’m wiser now. I clearly achieve earning $500,000 is not necessary for happiness. For a family of four, $300,000 should be good enough! I know some of you are rolling your eyes, but at least that’s 40% lower than what these Millennials expect they need to earn to be happy.

I’ve written follow-on articles such as, Don’t Make $400,000+ A Year, Look How Miserable GS Analysts Are, to make my claim explicit. I’d rather earn $100,000 in passive income or $150,000 at a job I love than make $500,000 at a job I hate.

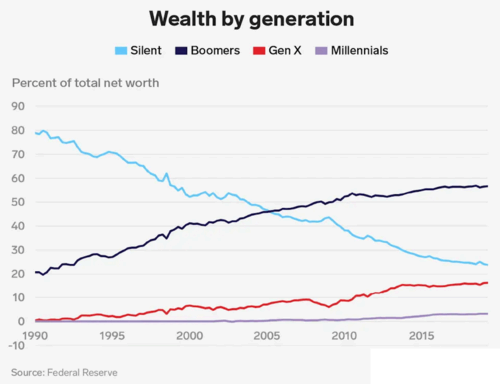

Given Boomers and Gen Xers have had a longer time to save and invest, of course we don’t need as high of an income to feel happy. Our net worths are much greater than the average net worth of a Millennial. Millennials only hold less than 5% of the total wealth.

Net Worths Required To Be Happy Don’t Make Sense

What I also find interesting about the survey is the net worth required by generation to be happy. The overall net worth desired is $1.2 million among all age groups. $1.2 million is close to the average American household net worth of $1.06 million according to the latest Consumer Finance Survey.

However, for Millennials, the net worth desired is only $1.7 million. I say “only” because $1.7 million is only 3.23X greater than the $525,000 in annual income required to be happy for Millennials.

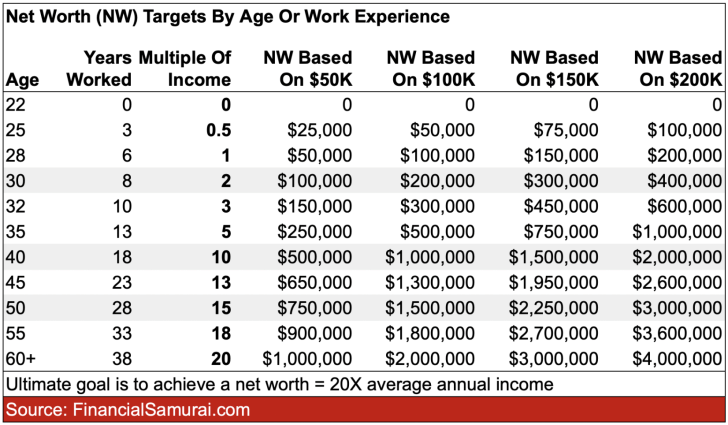

If you are to follow my net worth target by age guide, a 35-40-year-old Millennial in 2023 should aim to have a net worth equal to 5X-10X their average annual income. If you want to reach financial happiness in retirement, you must methodically grow your net worth over time.

Hence, the Millennials in this survey who desire $525,000 in annual income should also endeavor to have an ideal net worth of $2,625,500 to $5,250,000. But because Millennials say they only need a net worth of $1.7 million to be happy, this implies Millennials aren’t thinking properly about their finances.

Or maybe, Millennials have adopted the spending habits of the couple in my scraping by on $500K post and strategize to spend almost everything they earn. A double delusion that can only direct to unhappiness!

Having A Financial strategize Brings About Happiness

No matter what your ideal income or net worth is to be happy, 73% of the survey respondents believe having a financial strategize can contribute by bringing a sense of security. I agree with this.

Think about how much calmer you feel when you have a list of grocery items when entering the grocery store. differentiate this with the constant did I neglect something feeling if you didn’t have a list.

Having a financial strategize for retirement brings a sense of calm. When you know where your money is going and have a purpose for every dollar you earn and save, you will feel happier.

I’ve used Empower to track my net worth since 2012. As a result, I’ve felt much more in control of my finances. I got rid of expensive active mutual funds for index funds. I’ve also mapped out my expected retirement cash flow with its Retirement Planning tool.

Create a strategize on your own with the help of technology or seek out a fee-only financial planner. There is no rewind button in life. Hence, do your best to get your money right in the first place.

Reader Questions And Suggestions

Why do you think Millennials think they need to earn way more money than other generations to feel happy? What do you think is the ideal income to be happy? What about the ideal net worth?

Listen and subscribe to The Financial Samurai podcast on Apple or Spotify. I interview experts in their respective fields and converse some of the most interesting topics on this site. Please share, rate, and review!

For more nuanced personal finance content, unite 60,000+ others and sign up for the free Financial Samurai newsletter and posts via e-mail. Financial Samurai is one of the largest independently-owned personal finance sites that started in 2009.

Q2 2024 Earnings Call Transcript")