Sergey_P/iStock via Getty Images

Brookfield Asset Management (NYSE:BAM) used to be my favorite overall alternative asset manager due to its phenomenal long-term track record of generating outsized total returns, its sticky earnings stream from having almost entirely long-dated and permanent capital in its assets under management, formidable competitive advantages, an asset-lite business model that also benefits from co-investments from Brookfield Corporation (BN), debt-free and cash-rich balance sheet, and strong long-term growth potential.

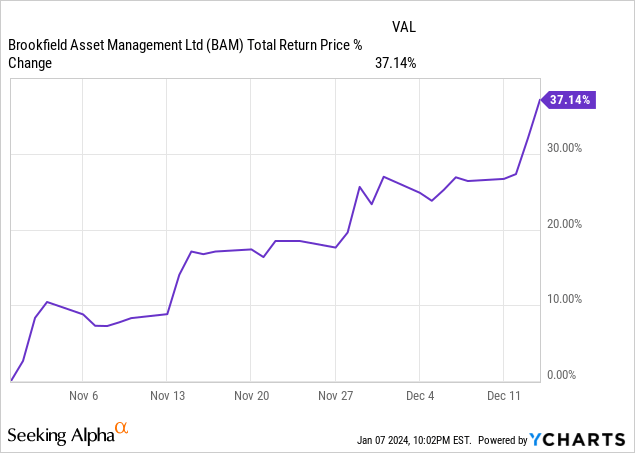

In fact, my conviction was so strong that – at a time when many Seeking Alpha analysts and commenters were growing increasingly bearish on BAM stock due to momentary steep declines in the unit price of Brookfield Infrastructure (BIP)(BIPC), Brookfield Renewable (BEP)(BEPC), and Brookfield Business (BBU)(BBUC) – I doubled down on my position and labeled it a Strong Buy.

That conviction paid off, as the stock shot over 37% higher over the next month-and-a-half, at which point I decided to sell my shares:

In this article, I will detail three reasons why.

#1. Recession Is Likely On The Horizon

One reason why I felt that the risk-reward in continuing to hold BAM was not attractive is simply that the odds of a recession hitting the U.S. economy in the near future are quite high in my opinion. While the Federal Reserve and the Treasury will likely do everything they can to prop up the economy and drive a bullish narrative during the election season, it is likely that a recession will hit sooner rather than later.

Notable financial experts, including Ted Oakley and several prominent economists, have expressed pessimism about the near-term health of the U.S. economy and Buffett’s Berkshire Hathaway (BRK.A)(BRK.B) has sold substantial stock holdings in recent months (which is noteworthy given that Berkshire is almost always a net buyer of stocks and already has a huge cash pile). Moreover, leading business and investing figures like Michael Burry, Elon Musk, and Peter Lynch, among others, have shared concerns about the near-term outlook for the economy and stock market. Additionally, indicators such as the Yield Curve Inversion Model and State Coincidence Indicator Model further imply a high recession probability. This convergence of expert opinion and analytical models seems to be pointing to a high risk of recession ahead.

A recession would likely be bad for BAM stock for a number of reasons:

- Many of its underlying businesses would likely see their earnings suffer, resulting in lower performance-based fees for BAM.

- Fee-based earnings could also suffer if the valuation of its underlying assets is repriced lower, leading to a lower enterprise value (from which most of its fee-based earnings are determined).

- It could weaken fundraising momentum, as some nervous investors may pull back from deploying funds into investments until the economic clouds clear.

- It would likely have a negative impact on BAM’s stock price because (1) a lot of growth is currently priced into BAM’s stock price and – as already mentioned – this growth would likely not materialize as quickly as expected in a recessionary scenario and (2) this is a historical pattern for BAM stock. In both the 2008 and 2020 recessions, BAM’s stock sold off significantly more aggressively than the broader market did.

#2. BAM Stock’s Significant Office Real Estate Exposure

Another reason why I sold BAM when I did was because it has significant exposure to office real estate. While BAM itself has an asset-lite balance sheet and does not own any office real estate directly, nearly one-quarter of its fee-bearing capital is invested in real estate, of which a significant portion is invested in retail and office real estate and these assets have a considerable amount of leverage attached to them.

Yes, Brookfield is an expert at using non-recourse leverage on its assets in order to protect its corporate balance sheets from distress, but that does not matter to BAM either way. BAM’s value is tied to the fees it generates from its assets, and if it is forced to default on several of its office and even retail assets during a meaningful recession and/or in the event that it has to refinance debt at much higher interest rates than it originally contracted at when it leveraged up these properties, it could see a meaningful bite taken out of its management fees from its real estate portfolio.

While I do not see this as a huge risk to BAM’s earnings stream due to its diversification and the overall high quality of its assets, the stock has gotten to a point where it is pricing in a near Goldilocks scenario for the business and no risk at all of the distress in its real estate portfolio. As a result, the risk-reward no longer seems particularly attractive here.

#3. BAM Stock’s Valuation Has Gotten A Bit Rich

This brings me to the final – and biggest reason – why I sold BAM stock recently: the valuation is no longer compelling. While I have already downgraded BAM’s peer Blackstone (BX) because of its rich valuation, I am now downgrading BAM stock to neutral as well for the same reason. While interest rates remain at elevated levels and the aforementioned recession and office real estate risks remain very real, BAM’s NTM price-to-earnings ratio has soared to 26.33x and its NTM dividend yield has fallen to 3.57%, neither of which looks cheap in any way. Yes, if the economy has a soft landing and interest rates plunge, BAM’s growth could take off and justify its rich valuation, but there is still a high chance that this does not happen in our view. As a result, the upside potential appears a bit limited in our view, while the downside risk is quite substantial.

Investor Takeaway

BAM is a great company and has a bright long-term outlook. However, as Buffett says: price is what you pay and value is what you get. In our opinion, now is not the time to be buying BAM, and – given the plethora of undervalued high-yield stocks that were available in mid-December (and still are available) – we decided to sell our position and lock in phenomenal gains, especially since we doubled down on our position in late October.

We would be happy to buy back in if the stock pulls back into the low $30s, but until then, we will be on the sidelines and be invested elsewhere.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")