Celsius Holdings‘ (CELH -0.12%) financial performance over the last few years would make you think the whole company drinks copious amounts of its energy drink product. Over the last five years, there’s been epic sales growth — up nearly 2,000% to nearly $1.15 billion over the last 12-month reported stretch.

For all the knowledge we possess today about liquid chemical concoctions perhaps not being so good for us, the global energy drink market is still a growth market anticipated to outpace economic expansion by a wide margin. Constant “innovation” in flavors and ingredients is to blame. (Right now, I’m sipping a Coca-Cola (KO 0.08%) “made with AI” — such are the times we live in!) We young consumers like our variety and change.

And yet, energy drinks are a fiercely competitive field, dominated by big players Red Bull and Monster Beverage (MNST 0.33%). Celsius has some oddities in its history, and there have been plenty of doubts its epic rise was even possible. Despite some of my own doubts that it will continue, I recently bought a small starter position. Here’s why.

Consumer goods are not my typical cup of tea

Besides the whole secular growth trend favoring energy drinks and caffeinated beverages, there’s another simple reason I decided to buy a little Celsius. After holding Disney (DIS 0.09%) for well over a decade (around the time a younger and just-as-nerdy version of me was excited about the company launching a new era of Star Wars), it was high time to part ways.

I recently sold all my Disney stock. For a holding that old in my portfolio, it was an egregious underperformer. This was an exit I’ve been planning for over a year, and Celsius is but one consumer-facing stock I decided to buy as a replacement.

Consumer goods don’t exactly dominate my attention these days — semiconductors and accelerated computing do, thus the choice of a “Coke AI” as an afternoon pick-me-up. So, it was time to brush up on Celsius’ history again.

The last time I took a hard look was in 2022, when PepsiCo (PEP 0.80%) was investing in Celsius in exchange for becoming a distribution partner in the U.S. Pepsi scored a $550 million investment in brand-new convertible preferred stock that pays out a 5% annual dividend. We ordinary shareholders get no such dividend from Celsius. At the time, it seemed like Pepsi was landing a deal to scoop up most of the profitability from any future Celsius growth.

Now, what I do know is that marketing a hot consumer brand is key, but the food and beverage industry is also largely dominated by big distributors. After all, part of Monster’s wildly successful run (including a name change from “Hansen Natural” to Monster back in 2012) has been at least partly attributable to its distribution partnership with titan Coca-Cola. But Celsius signing on with Pepsi in exchange for a big equity slice didn’t excite me. I was wrong.

Celsius finds another gear

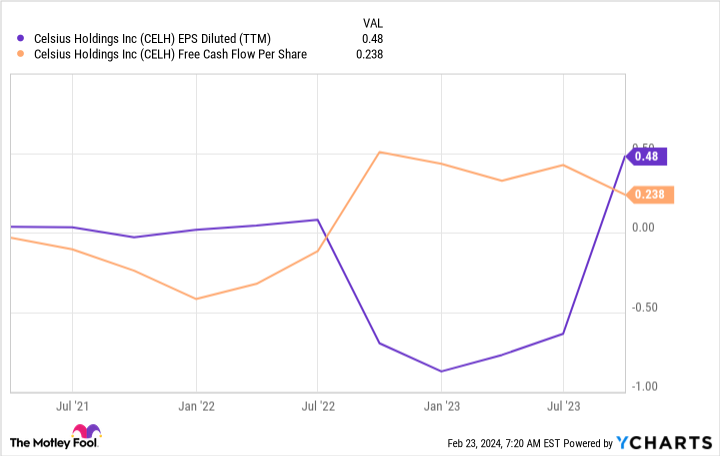

Plugging into PepsiCo’s distribution has worked wonders for Celsius — Pepsi has accounted for nearly 61% of Celsius’ distribution through the first nine months of 2023 (versus 12% in the comparable period in 2022). Revenue soared, and profits have begun to rise as well. Earnings per share and free cash flow per share muted — at best — since the Pepsi agreement might be starting to turn higher.

Data by YCharts. EPS = earnings per share. TTM = trailing 12 months.

Additionally, Celsius is only just beginning to tap into the global energy drink market as it signs new distribution deals overseas. To be sure, managing this expansion will be expensive. But if management (including a new CFO installed in 2022 after some accounting question marks in prior years) executes well, Celsius could be on the cusp of lots more sales growth in the coming years.

GAAP net income was $143 million through the first nine months of 2023, up from a loss of $171 million the year prior. I’d like to see more of that profitable growth continue, and if it does, I’ll buy more Celsius stock.

Granted, this is an “expensive” stock at over 40 times one-year forward expected earnings per share. A lot is riding on Celsius continuing to expand at a voracious pace. (Wall Street analysts have nearly 40% sales growth penciled in for 2024, building on the expected doubling in revenue in 2023.)

This is why I started with a small position and plan on building it larger over time if the story stays energized. But after watching from the sidelines for some time, Celsius seemed like a decent place to stash some long-term money in the consumer brands space. Time will tell.

Nick Rossolillo has positions in Celsius. The Motley Fool has positions in and recommends Celsius, Monster Beverage, and Walt Disney. The Motley Fool has a disclosure policy.

Q2 2024 Earnings Call Transcript")