Oselote

This Analysis Suggests a Hold Rating for Fresnillo

Fresnillo plc (OTCPK:FNLPF) has been assigned a “Hold” rating, in the sense that retail investors should not buy this stock. Shares are expected to continue to perform in an uninspiring way in the OTC market, mainly reflecting a lack of bite in corporate profitability (usually a strong driver of stock price), which could be found if silver rises amazingly.

If the retail investor owns Fresnillo stock, there is a chance for him to make some profit by selling some shares in the future, but hardly from current levels. With this in mind, gold will likely furnish more maintain than Fresnillo’s mainstay silver to achieve the target, but that scenario is unlikely to materialize any time soon.

Stumbling Into Fresnillo Stock as Precious Metals Prices Offer Miners a Rosy Outlook

Retail investors who may be interested in expanding their portfolio exposure to the precious metals market as it continues to show good momentum have many opportunities to do so. They could invest in various securities that track the price movement of gold or silver, including publicly traded stocks of exploration and mining companies, but generally not directly in the physical metal. The latter investment solution would demand capital that private investors generally do not have access to, but to which only large companies such as institutional investors or banks have.

The industry of US-listed gold and silver stocks offers many opportunities at the moment. While going through the population of these companies I came across the Mexican explorer and producer of precious metals–FNLPF.

About Fresnillo plc as the World’s First Silver Mining Company

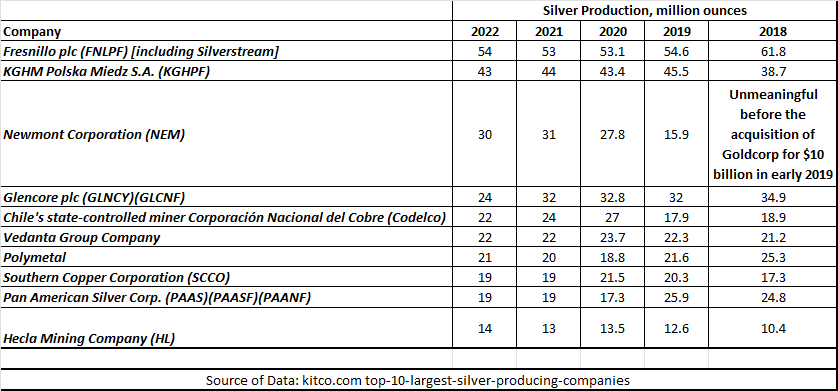

This company is probably still the largest in the world in terms of the annual production of attributable silver, after topping the ranking of the biggest silver miner in the world in past years. For the full year 2023, the company expects it should be able to produce between 57 million and 64 million ounces of attributable silver (including a silver stream business). The company will also mine gold and the resulting production is expected to be 590,000 to 640,000 ounces.

The company mined 54 million ounces of attributable silver in 2022 and 54.6 million ounces of attributable silver in 2022, significantly outperforming well-known miners such as Glencore plc (OTCPK:GLNCY)(OTCPK:GLCNF) or Newmont Corporation (NEM), though compared to 5 years ago the level now reflects a significant refuse.

Source of Data: Kitco.com

Despite still likely being the world’s largest producer of silver (in addition to significant annual gold production of approximately 610,000 attributable ounces), this analysis does not imply a rating higher than Hold for Fresnillo plc.

A Hold Rating: Reasons

On the US over-the-counter (OTC) market this stock has very limited trading volumes, which according to the statistics that you can find if you scroll down this page of Seeking Alpha until the “Risk” section, are indicated in 5,329 shares traded on

average over the past 3 months.

With such a low volume of shares currently traded, the share price does not have much chance of recovering well if gold/silver prices rise, which is more likely to be the case for other stocks with larger trading volumes.

Analysts at Trading Economics expect the price of silver to rise robustly to $27.65/oz from the current $24.20/oz within 12 months (representing an boost of 14.2% since the time of writing).

Against the subdued trading volume of Fresnillo shares in the US OTC market, retail investors can find instruments that offer better return prospects for their investment, given rising silver prices, but also the expected bull market for gold.

The shares of Fresnillo should also have some exposure to the gold price action. Analysts at Trading Economics also forecast a 6.6% rise to $2,163.75/oz of gold in 12 months as the yellow metal, more than silver, is seen as an ideal safe-haven place against the headwinds that could arise if the economy slides into recession. However, because Fresnillo does not appear to be as strongly positioned as other mining stocks to benefit from the expected rise in the yellow metal, currently the Mexican silver and gold mining company is not the best bet ahead of the gold price rally either.

The Outlook for Silver and Gold

The trigger for an economic recession that seems very likely today is largely due to the Federal Reserve’s very aggressive hawkish stance in raising interest rates to cool core inflation, which last year reached its highest level in more than four decades. These factors try to impair the pillars of the US gross domestic product and direct economists, whose views recently welcomed the Swiss bank giant UBS Group AG (UBS), to believe that the downturn in the economic cycle is imminent and should occur as early as 2024.

The gray metal may benefit more from industrial demand than gold, mainly for reasons of affordability (an ounce of silver is 85 times cheaper than an ounce of gold), as the two metals otherwise share similar properties such as ductility and high electrical and thermal conductivity.

But even when it comes to industrial demand for silver, the near-term future isn’t as bright as many still believe. In recent times, governments’ resilience and economic programs have been the chance for industrial demand for silver, and there is no doubt about the boost this has given silver. Thereafter, the Fed’s signals of recession increased investment reluctance, and decarbonization and digitalization projects are now lagging behind the roadmap set by policymakers during the recovery from the COVID-19 virus. Because the precious metal is a central component of these projects, the long-term growth prospects for the silver price remain robust, albeit slightly lower than in the recent past.

Gold Seems to Help More than Silver in the Short Term

Therefore, this analysis assumes that momentum for Fresnillo stock may come more from gold than silver in the coming months. The room for silver price appreciation may be less than commonly believed, as silver is less of a safe-haven asset than gold in a recession, and the economic downturn is curbing industrial demand for silver. This is a scenario that bodes well for Fresnillo anyway, as gold accounts for 35 to 40% of total sales; But it still falls short of the impact that strong bullish silver sentiment can have on the stock, considering that the Mexican operator is the world’s largest producer.

What it Takes for Silver to Create True Bullish Sentiment around Fresnillo

Bullish sentiment for silver needs to be very strong, stronger than ever to create meaningful tailwinds for Fresnillo; Because the robust silver price conditions of recent years have not contributed much to the company’s profitability, resulting in subdued demand for Fresnillo shares in the US OTC market.

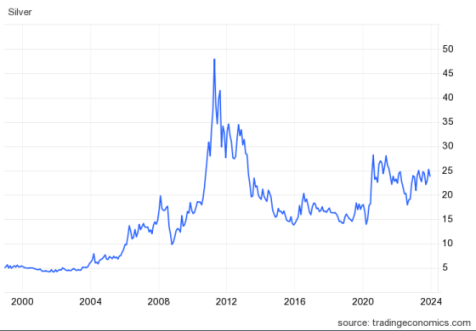

As history shows, between late 2010 and early 2013, the price of silver rose above $30 an ounce, reaching highs of $37, $44, and $48.50.

Source: Trading Economics

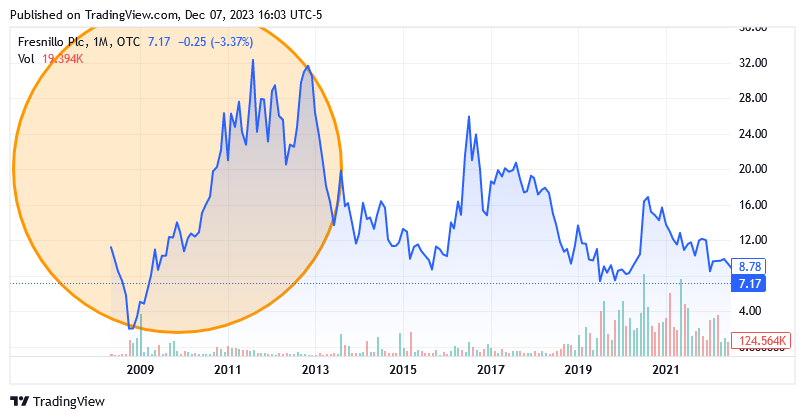

Along with this bullish momentum in silver, Fresnillo stock experienced a strong rally as the market welcomed the results that a positive correlation with the metal meant for Fresnillo’s business.

Source: Seeking Alpha

In a short period of time, Fresnillo probably managed to build a positive reputation in the US stock market among bullish traders, and not only because of its large silver production, but the price of silver had to rise insanely for the stock to merit the label.

Robust Silver Prices, But Still Not Enough

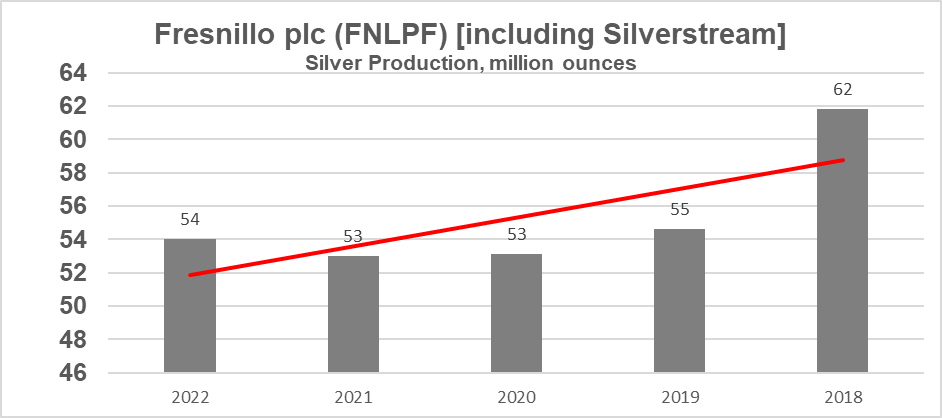

While Fresnillo still reigns as the largest silver mining company in the world, the same cannot be said for its ability to create returns with its current production level, which, among other things, is well below where it was five years ago.

Source of Data: Kitco.com

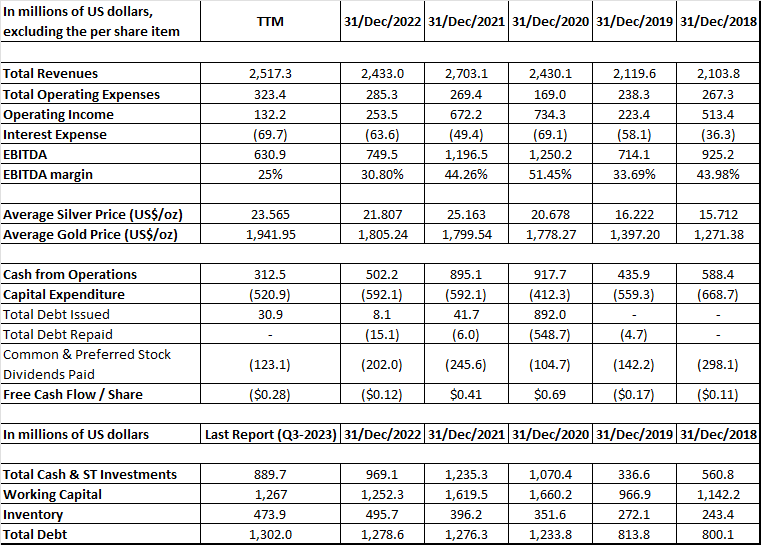

The company’s key profitability metrics could be better than the following.

Although the price of silver remained in a robust range (say well above the 5-year average of $20/ounce), the EBITDA margin – a profitability metric highly regarded by investors in capital-intensive industries such as mining companies – fell sharply from its peak in 2020 to 25% for the last 12 months up to the third quarter of 2023.

This refuse in corporate profitability occurred despite attributable production of silver and by-products (direct and zinc) in the first 9 months of 2023 performed better than the same period in 2022: Year-over-year, silver (including a silver stream business) rose 2.2% to 42.121 million ounces, while by-product direct rose 4.3% to 41,938 tons and by-product zinc rose 3.6% to 78,861 tons.

Source of Data: Seeking Alpha

The ramp-up of the Juanicipio underground mine (7 km southwest of Fresnillo, Zacatecas, and 10-year mine life), coupled with higher grades in the underground San Julián veins (170 km NE from Guamúchil, Chihuahua, Mexico, and 3-year mine life ) and higher volumes of ore material processed at the Fresnillo underground mine (near Fresnillo, Zacatecas, 3-year mine life), is proving to be insufficient to offset some operational headwinds and macroeconomic headwinds.

Nor is the Herradura open pit (83 km northwest of Caborca, Sonora, and 9-year mine life), with its lower production costs compared to other expensive underground mining operations, really effective as a hedge against headwinds. Thus, higher grade ore/larger volume of ore processed at the Herradura open pit is not enough either.

Silver prices, but not even gold prices, have proven sufficiently supportive to help the company’s profitability improve under pressure from an underperforming gold business and other exogenous factors such as the appreciation of the Mexican peso against the U.S. dollar and inflationary pressures on production input costs. The latter two factors are likely to continue to impact the company in 2024, as will the refuse in gold ounces production at Noche Buena. This open-pit mine (55 km northwest of Caborca, Sonora) is nearing the end of its operations. The remaining gold will be recovered from leaching activities after reserves are fully depleted.

On an annual basis, attributable gold production fell 2.2% to 458,042 ounces in the first nine months of 2023.

The lower ore grade in the disseminated body ore for the flotation facility at the San Julián underground mine, along with lower production from the Ciénega underground mine (203 km northwest of Durango, Durango, and 2.5 years of mine life) and lower production from the Saucito underground mine (9 km southwest of Fresnillo, Zacatecas and 6 years of mine life) despite the development of underground infrastructure at Saucito in recent years to improve the speed of mining operations and the yield of the processing plant.

The heavy reliance on underground mining techniques puts a major strain on the company’s profitability, as this production currently requires much higher extraction efforts, as well as frequent maintenance interventions and streamlining of activities, compared to open pit or surface mining.

Thus, the metal price, although remaining at historically high levels, did not allow positive free cash flow except in 2020 and 2021, but in these 2 years only after a capital injection through additional debt. This debt ($1.3 billion as of Q3-2023) incurs a total of $70 million in annual interest expense, but operating income is approximately 1.8 times higher. The company is still able to cover the costs of its outstanding debts, although the situation is currently very close to a limit, since for investors 1.5 times is the minimum threshold that the indicator should have.

The Financial Condition

At nearly $890 million including short-term securities, liquidity has deteriorated somewhat over the past two years. However, if precious metals trade higher as forecast, inventories could offset much of the refuse.

Overall, the current financial situation keeps the risk of bankruptcy at bay, as shown by the Altman Z-Score of 3.33 (on this page of Seeking Alpha page, scroll down to the “Risk” section to find the information).

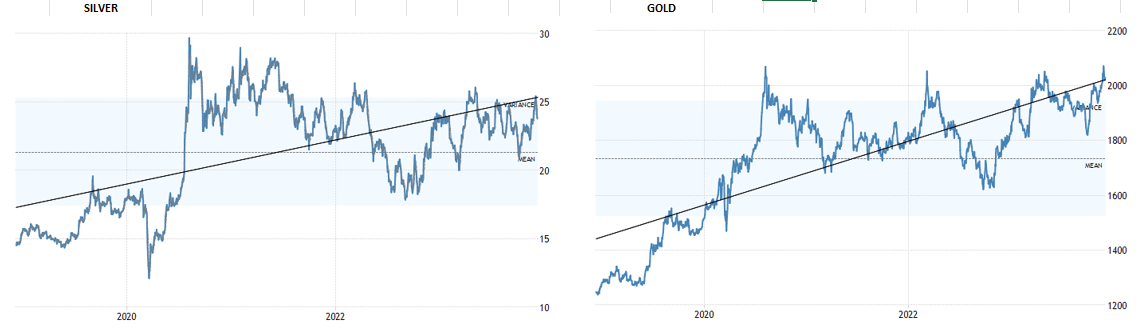

Market Implications: Fresnillo Stocks in the US OTC Market vs. Gold and Silver Prices

Retail investors should not hold a position in Fresnillo hoping to benefit from the long-term, albeit cyclical, upside potential of silver and gold prices.

While silver and gold have a positive underlying trend although not steadily but through cyclical swings, Fresnillo’s stock has generally not increased in value when held in the portfolio for an extended arch of time.

Silver and gold prices in the London gold markets over the last 5 years:

Source: Trading Economics

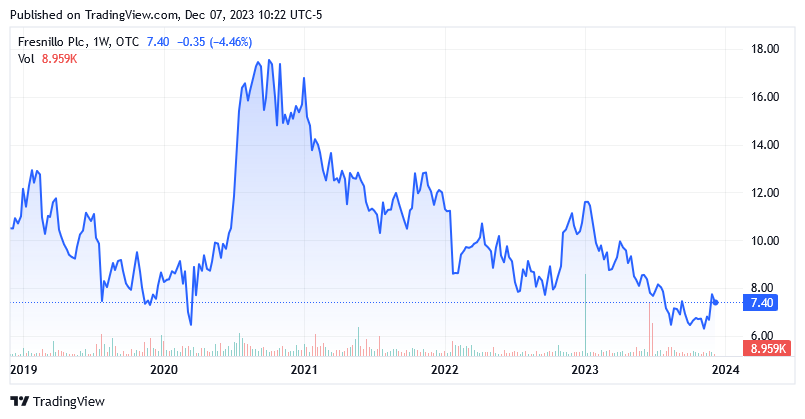

Fresnillo’s stock prices in the US OTC market over the last 5 years:

Source: Seeking Alpha

Neither should the retail investor buy shares of Fresnillo because of the dividend as despite the dividend yield of 2% vs. S&P 500’s yield of 1.51% as of this writing, the annual payout ratio (TTM) is just $0.15 per share. The company has reduced its payout ratio by 18.38% over the past five years, reflecting the need to fortify its balance sheet.

A dividend cut could imply greater uncertainty about the company’s future profitability, and this should actually raise some concerns about this stock as the outlook for silver and gold prices, on the contrary, does not warrant similar action.

The Valuation of this Stock

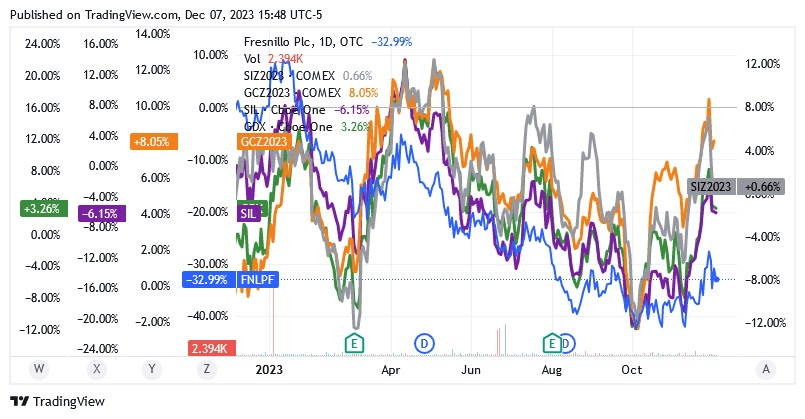

Retail investors could use Fresnillo to take advantage of significant short-term price movements in precious metals, but the stock is currently not as well suited as other mining stocks for this purpose either.

Fresnillo shares have lost almost 33% over the past year, while 2023 has been a fairly positive year for gold (GCZ2023) +8.05% and silver prices (SIZ2023) are on track to close the year slightly in the green. As a benchmark for publicly traded silver miners, the Global X Silver Miners ETF (SIL) was down 6.15%. As a benchmark for publicly traded gold miners, the VanEck Gold Miners ETF (GDX) gained 3.26%.

Source: Seeking Alpha

In the wake of the strong price rally in gold (+13.6%) and silver (+26.8%) from early March 2023 to early May 2023 – as investments in the precious metal were widely sought as a hedge against headwinds due to the failure of some regional banks in the US – many US-listed gold/silver stocks delivered a hefty return within a few weeks that could certainly maintain a position in one of these stocks.

The same didn’t really happen for Fresnillo’s shares, which instead posted significantly smaller gains of 17% from March to April and 7% from March to April, respectively, during the best sub-period of 2023 for silver and gold prices.

FNLPF shares are trading at $7.25 per unit giving it a market cap of $5.36 billion as of this writing. Shares are below the middle point of $9.055 in the 52-week range of $6.16 to $11.95, and they are trading in between the 50-day simple moving average of $6.70 and the 200-day SMA of $7.86.

Furthermore, the stock doesn’t look cheap compared to the industry either, as Fresnillo stock has an EV/EBITDA ratio of 9.55, versus the industry median of 8.60, assuming it had interesting growth prospects or more in line at least with other stocks.

Conclusion

Fresnillo has a portfolio of silver and gold mines, as well as direct and zinc by-product productions, all in Mexico. These businesses have not performed well, as evidenced by declining profit margins and negative free cash flow, even as silver and gold showed robust prices.

This is most likely related to the costly operations involved in mining underground deposits, which demand more effort than open-pit or surface mining. The unfavorable exchange rates between the Mexican peso and the US dollar as well as inflationary pressures on production inputs are also causing major headwinds. Investors should not rely on the temporary nature of these exogenous factors. Rather, he should be aware that the environment is becoming increasingly volatile and uncertain. Macroeconomic and geopolitical issues boost the likelihood that exogenous factors affecting the company’s profitability will become more common in the future.

With this in mind, Fresnillo’s balance sheet looks a little more solid after reducing dividend spending, but this suggests, among other things, that the board now sees greater uncertainty about the company’s profitability. And that is the situation at present, even though silver and gold prices are robust. This should be a reason to proceed with caution even if Fresnillo remains the leading silver producer in the world.

Investing in Fresnillo doesn’t seem very attractive overall, which likely explains the lack of enthusiasm for the stock in the OTC market.

There are better solutions on the market to profit from the rise of the precious metal than the US-listed stock of Fresnillo. So, this analysis believes that the retail investor should not buy this stock. If the retail investor owns shares, there is a chance for him to make some profit in the future (as the shares could rise slightly if the price of silver and especially gold increases), but not in the near term.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")