Shares of Dynatrace (DT -0.15%) dropped 13% last month, according to data provided by S&P Global Market Intelligence. Investors were disappointed by its quarterly-earnings report; sales, cash flow, and key performance metrics were generally solid, while the company’s forecasts and forward-looking commentary raised some concerns.

Investors are worried about weak revenue guidance

Dynatrace shares dropped after its Feb. 8 quarterly report and continued to slide lower throughout the month. The company narrowly beat Wall Street’s estimates, with 23% revenue growth and adjusted earnings per share (EPS) of $0.32.

Image source: Getty Images.

It’s hard to criticize those headline figures, but investors were focused on the company’s less impressive outlook. Dynatrace reduced its first-quarter subscription-revenue forecast, which is never good news for a growth stock. The company’s management team cited some large deals in its sales pipeline that were taking longer to close as the reason behind the forecast revision. If it’s truly a timing issue, then investors should expect a relatively quick bounce back when those large deals hit financial results.

However, longer sales cycles justifiably raise skepticism from investors. It could be competitive pressure, macroeconomic issues, or inefficient sales activities. Any of those factors could be serious trouble for a growth stock, so it’s easy to see why the market got hung up on those details.

Dynatrace’s valuation is now materially cheaper than some observability and security stocks with similar financial metrics. That gap is likely to close if their business fundamentals continue to trend similarly, which could create relative upside potential.

Dynatrace doesn’t garner quite the same hype as many of its peers

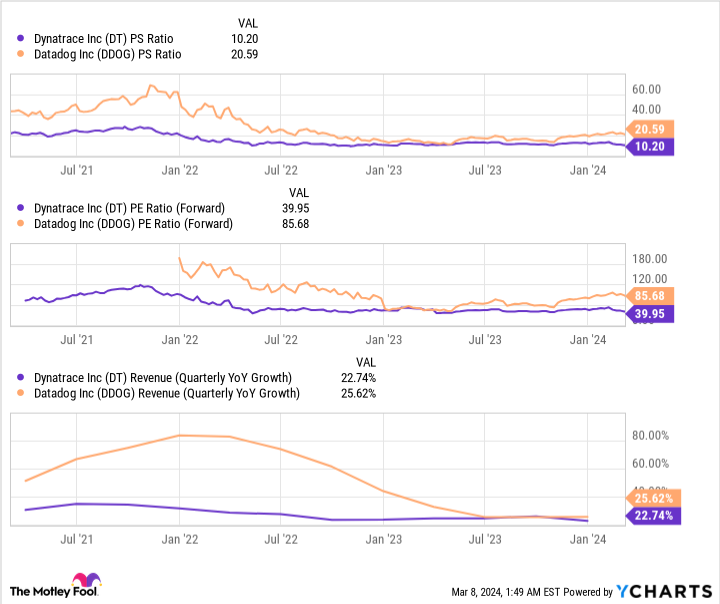

Dynatrace hasn’t enjoyed the same hype as its peers in the application-performance-monitoring and observability industry, such as the recently acquired Splunk (SPLK 0.03%) and DataDog (DDOG -0.64%). Dynatrace has consistently lagged DataDog’s valuation ratios in recent years. That was likely driven by DataDog’s higher growth rate in past periods, but that gap has closed.

DT PS Ratio data by YCharts.

Even after the downward revisions, Dynatrace is still expecting nearly 20% sales growth this year. That’s not the fastest-growing business on the market by any means, but it’s still an impressive figure. The company’s product suite is highly rated by Gartner and customers, which is important for competitive viability. That quality was corroborated by it’s impressive 113% net-dollar retention last quarter; Dynatrace is retaining customers upselling existing accounts. Unlike many growth-tech stocks, Dynatrace is profitable on a generally accepted accounting principles (GAAP) basis. It also produced $67 million in free cash flow last quarter, representing 17% growth over the prior year.

The stock’s price-to-sales ratio is over 10, and its forward price-to-earnings (P/E) ratio is roughly 37. Those are standard valuation ratios for a growth stock, and they are cheap enough to allow significant returns if the company meets its growth goals. There are valid reasons that this stock trades at a discount to many of its peers, but the valuation gap might be too wide to ignore.

Ryan Downie has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Datadog and Splunk. The Motley Fool has a disclosure policy.

Q2 2024 Earnings Call Transcript")