Shares of Devon Energy (DVN -0.80%) slumped 26.4% in 2023, according to data provided by S&P Global Market Intelligence. Several factors weighed on the oil company, including lower oil prices. That impacted its cash flow, which affected its variable dividend.

Devon ran low on fuel to pay dividends

Oil prices slumped last year. West Texas Intermediate (WTI), the primary U.S. oil price benchmark, fell 10.7% in 2023, ending at $71.65 per barrel. That was the first down year for crude oil since 2020.

Falling oil prices weighed on Devon Energy’s cash flow. On top of that, service cost inflation forced the company to increase capital spending last year. With cash flow falling and spending rising, Devon produced a lot less free cash flow in 2023. The company generated $1.8 billion in free cash flow through the third quarter of last year, down from nearly $4.9 billion through the same period in 2022.

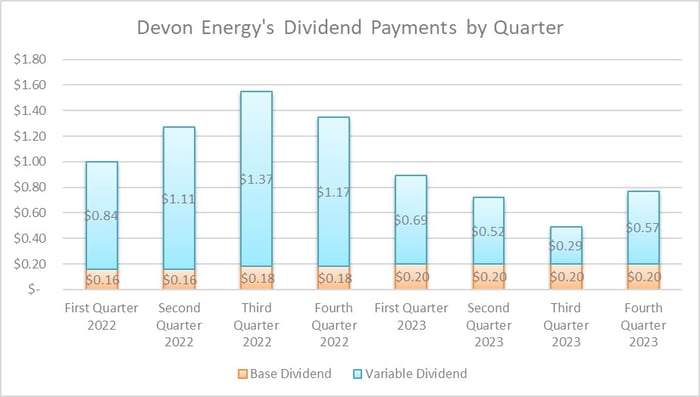

Devon Energy’s falling free cash flow directly impacted its variable dividend. Last year, the company set a target to pay up to 50% of its excess free cash flow in variable dividends each quarter (after paying its base dividend). With its oil-fueled cash flows retreating, Devon Energy’s variable dividend payments declined compared to the prior year:

Data source: Devon Energy. Chart by the author.

The oil dividend stock made $2.87 per share in payments last year ($0.80 in base dividends and $2.07 in variable dividends). That was 44.5% less than its total outlay in 2022. While Devon’s base dividend payments were 17.6% higher than the prior year, it paid 53.9% less in variable dividends.

On a more positive note, Devon Energy anticipates that one of the headwinds weighing on its cash flow will fade in 2024. It sees capital spending declining by about 10%, driven by lower service costs and a narrower investment focus on its highest-return regions. That would fuel a 20% improvement in its free cash flow, assuming WTI averages $80 per barrel this year (crude’s price point in early November when Devon provided its 2024 outlook). Higher free cash flow would give Devon more money to return to investors, including paying variable dividends and repurchasing its beaten-down shares.

Is Devon a buy after last year’s slump?

Devon Energy believes the steep slump in its share price is a buying opportunity in 2024. That’s driving the oil company’s plan to shift its capital return strategy. It’s targeting to return up to 70% of its free cash flow to shareholders this year. However, it plans to prioritize repurchasing its shares over paying variable dividends in the near term because it believes they trade at an attractive value. That strategy could pay off if oil prices cooperate this year by helping drive the stock price higher.

Matthew DiLallo has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Q2 2024 Earnings Call Transcript")