JHVEPhoto

My Thesis

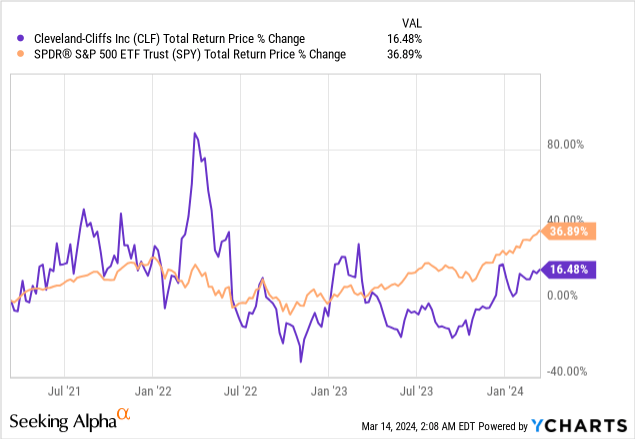

You are now reading my 15th article on Cleveland-Cliffs Inc. (NYSE:CLF) stock, which has been in a recovery trend since last September, but is still underperforming the S&P 500 Index (SP500) (SPX) when we look at the last 3 years:

Seeking Alpha, Oakoff’s coverage of CLF

Despite the medium-term underperformance, which is more likely due to the cyclical nature of the company’s industry, I still consider CLF to be one of the most promising companies in its niche. Despite CLF’s high volatility and the macro uncertainty surrounding the firm, I expect the stock to continue to go higher thanks to its relatively cheap valuation and the business expansion potential coming from strong financials and recent corporate developments.

My Reasoning

I suggest starting with a discussion of the latest financials, which I described as “strong” in the description of my thesis above.

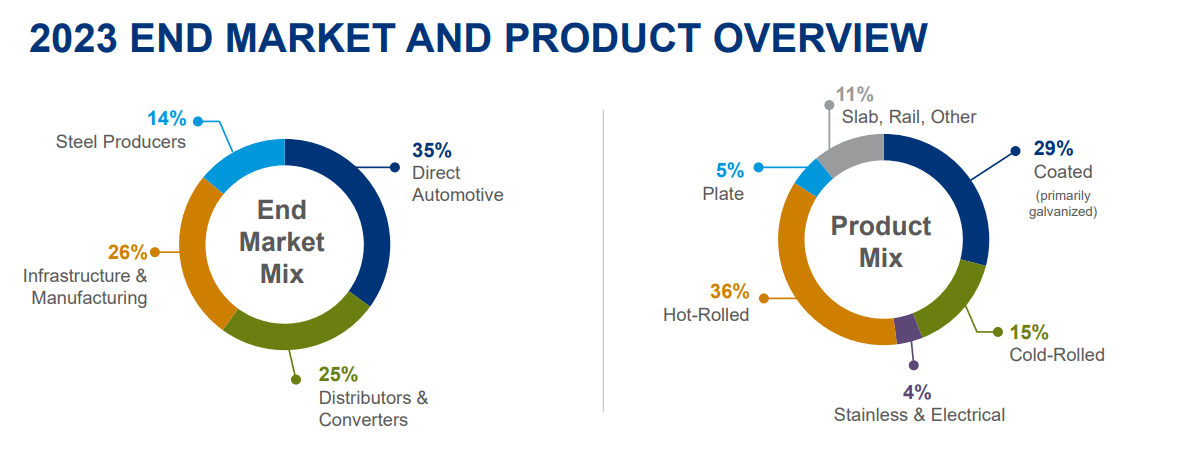

In Q4 2023, CLF’s external sales volumes reached 4.0 million net tons, showing a 5% YoY increase. The breakdown of steel product volume consisted of 29% coated, 36% hot-rolled, 15% cold-rolled, 5% plate, 4% stainless and electrical, and 11% other, including slabs and rail. Steel-making revenues amounted to $5.0 billion, with $1.6 billion from automotive sales, $1.3 billion from infrastructure and manufacturing sales, $1.3 billion from sales to distributors and converters, and $0.7 billion from sales to steel producers. That is, as we can see, CLF’s presence in different markets shows how diversified the company’s revenues are and therefore stable in the face of changes in demand in individual places. Cliffs’ sales mix and the distribution of sales in the end markets are best illustrated in the investor presentation for FY2023:

CLF’s IR presentation

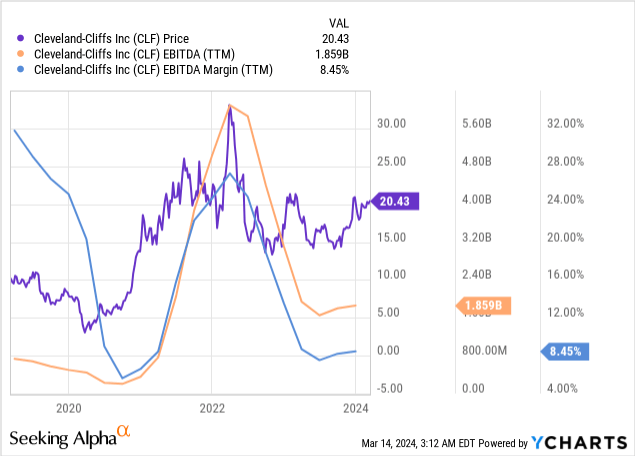

The average net selling price per ton of steel products in Q4 was $1,093, down 5% and 9% year-over-year and quarter-over-quarter, respectively. This explains why CLF’s revenue in Q4 grew by only 1.35% YoY. The downward trend in selling prices is particularly noticeable when comparing annual results: In FY2023, CLF’s total revenue from steel production decreased by ~5% compared to FY2022. Nevertheless, the management focused on cost control, according to the latest earnings call’s commentary, so the resulting adjusted EBITDA margin widened by 300 basis points YoY, reaching 5.5%. Even on an unadjusted basis, the EBITDA margin started to gradually recover; we saw roughly the same trend in 2021. Then the CLF stock responded with a sharp rise ahead of this financial improvement:

I think that CLF’s margins will improve in the future – in my opinion, today’s share price performance falls short of this possibility.

Why do I believe in margin expansion?

Firstly, Cliffs has a very strong presence in the automotive industry – it is thanks to this end market that the company’s shipments have grown as fast as we have seen in 2023. If we look at last year’s sales structure, we will see that it was the automotive segment that saved CLF’s growth rate during such a difficult time in terms of pricing.

CLF’s 10-K, Oakoff’s notes

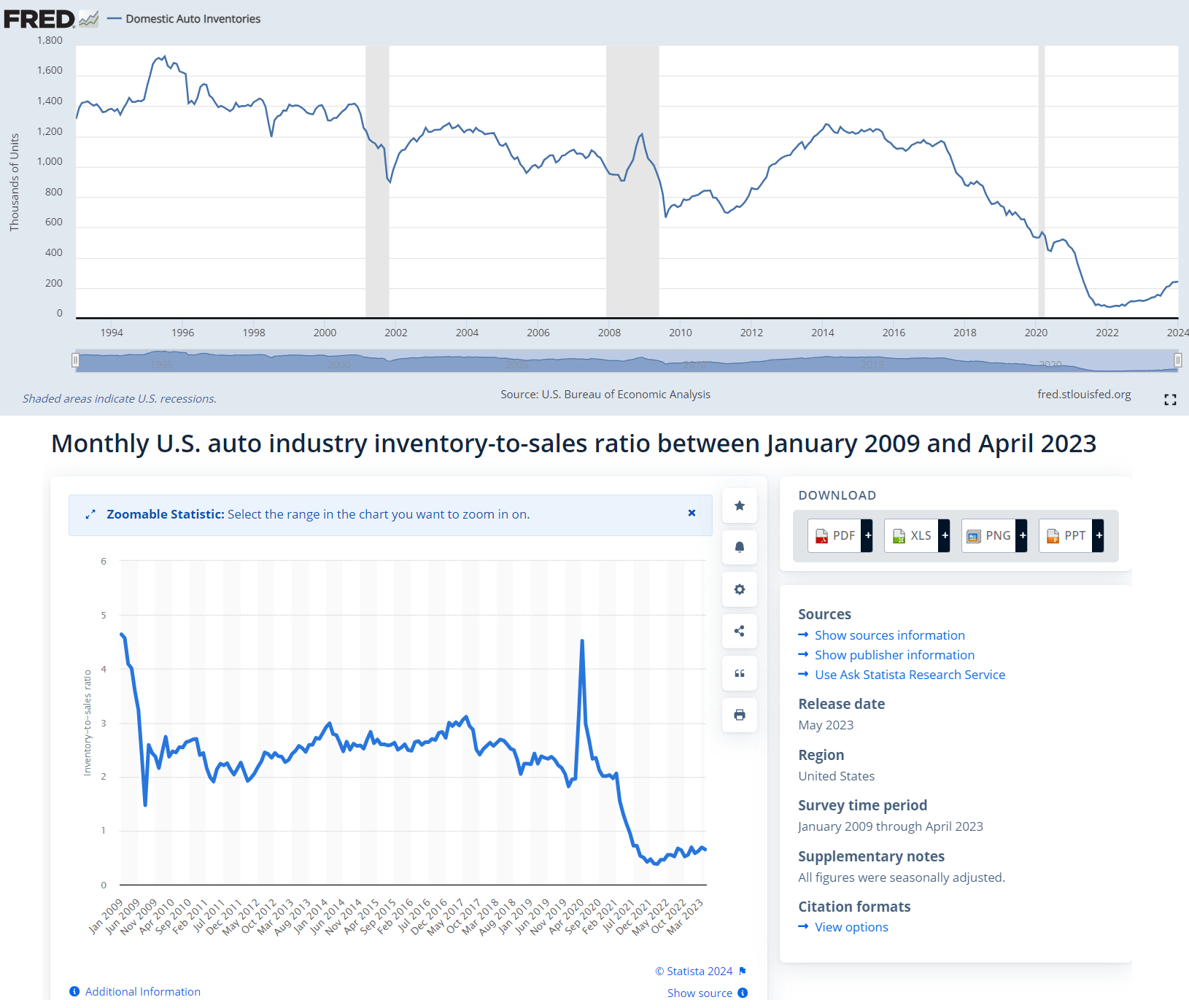

From a supply and demand perspective, auto sales in the US should only grow. I draw this conclusion from domestic auto inventory data (from FRED) and the inventory-to-sales ratio, which has been extremely low over the past year, and I expect the situation not to have improved significantly by March 2024.

FRED, Statista, Oakoff’s notes

Given the cyclical nature of other end markets that eventually start to grow, the strength of the automotive market should allow CLF to quickly recover lost gains in terms of growth rates and margins.

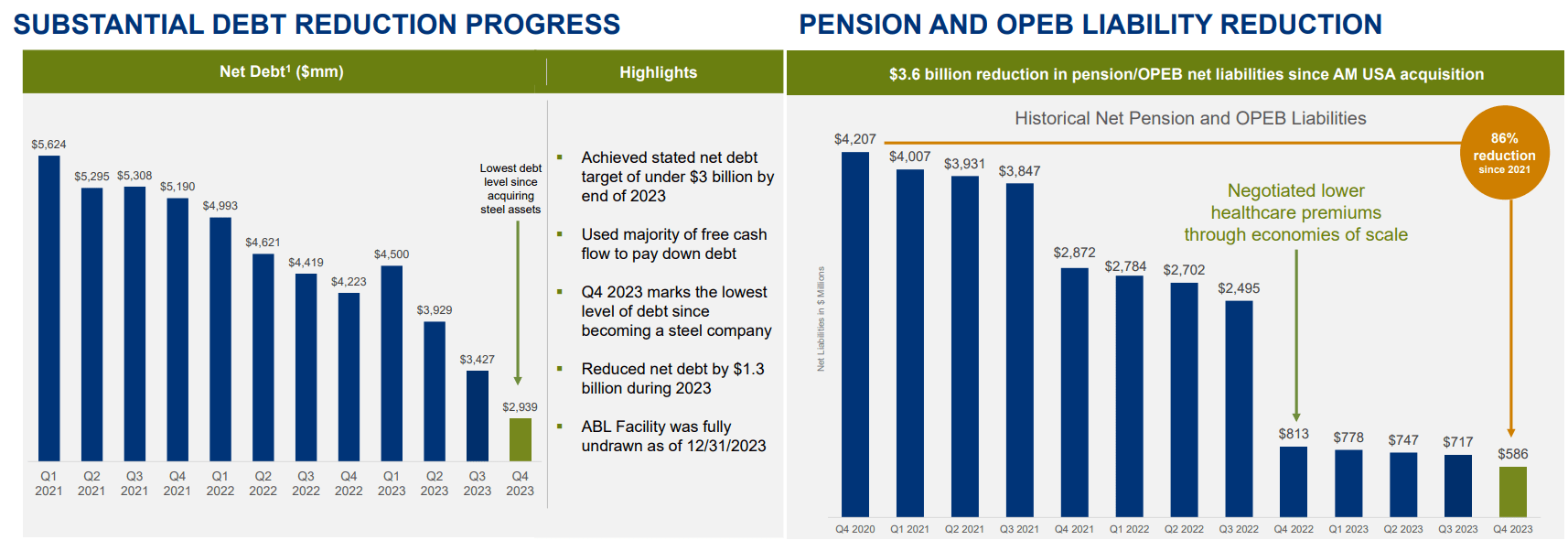

Second, CLF has a solid healthy balance sheet. Other authors, such as myself in my previous articles, have pointed out the rapid decline in the company’s leverage. 2023 was another year of deleveraging, with CLF reducing not only the “classic” debt but also net pension and OPEB liabilities:

CLF’s IR presentation, Oakoff’s notes

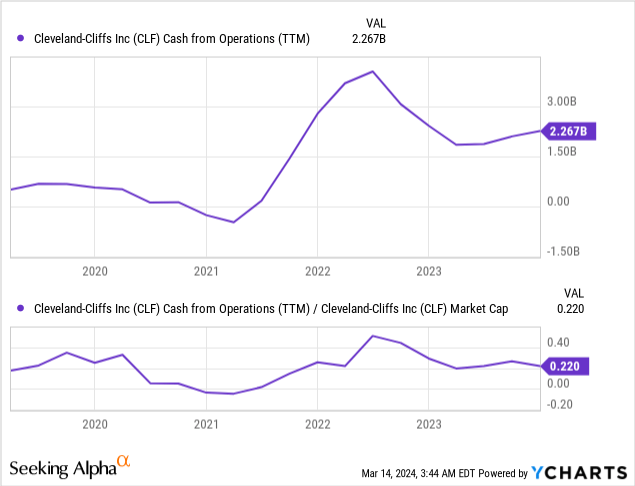

The company’s adjusted EBITDA covered interest expense in FY2023 by a factor of 6, while the total liquidity balance (including the ABL borrowing capacity which CLF didn’t even use in Q4 2023) amounted to $4,539 million (a record level) due to strong cash flow generation. The operating cash flow of almost $2.3 billion (TTM) represents ~22% of the company’s market capitalization and confirms my assumption that the market is lagging behind Cliffs’ potential.

I see no conditions for a deterioration in cash flows, and with lower debt, CLF should be able to recover its previous margins very quickly, so the stock should follow.

The third reason why margins will most likely continue to rise is the actions of management, which will not stop the cost-cutting efforts. The CFO Celso Goncalves noted during the earnings call that they expect to achieve another $30 per ton in cost reductions in FY2024, equating to ~$500 million in incremental EBITDA increase.

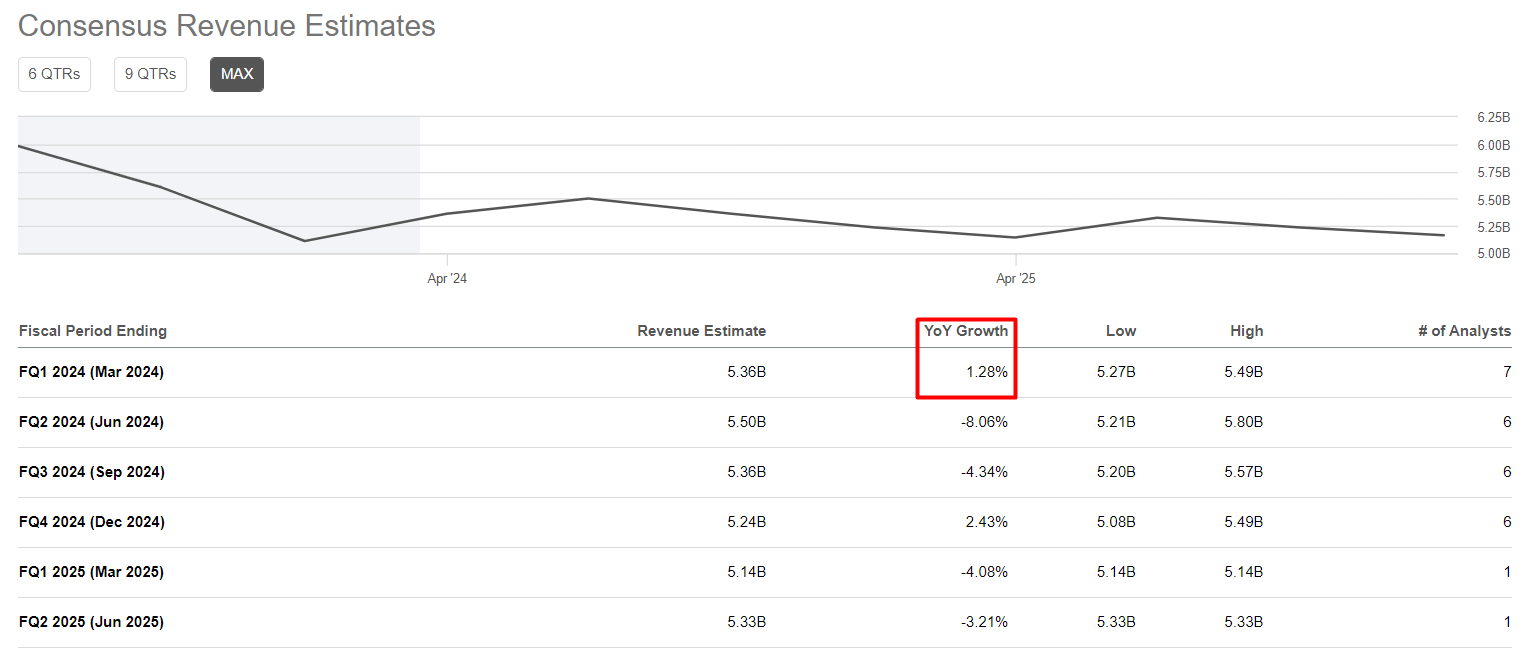

During the Q&A session, Celso Gonçalves made it clear that the company expects a slight increase in shipments in Q1 compared to the fourth quarter, with roughly the same sales mix. In addition, the Cliffs expects the average selling price to increase by ~$60 per ton as it benefits from delayed index pricing and other factors. We should wait for meaningful cost savings from lower commodity and coal prices until the second quarter of 2024, but with what we have on hand now, we can conclude that the consensus forecast for Q1 2024 may be somewhat underestimated:

Seeking Alpha, Oakoff’s notes

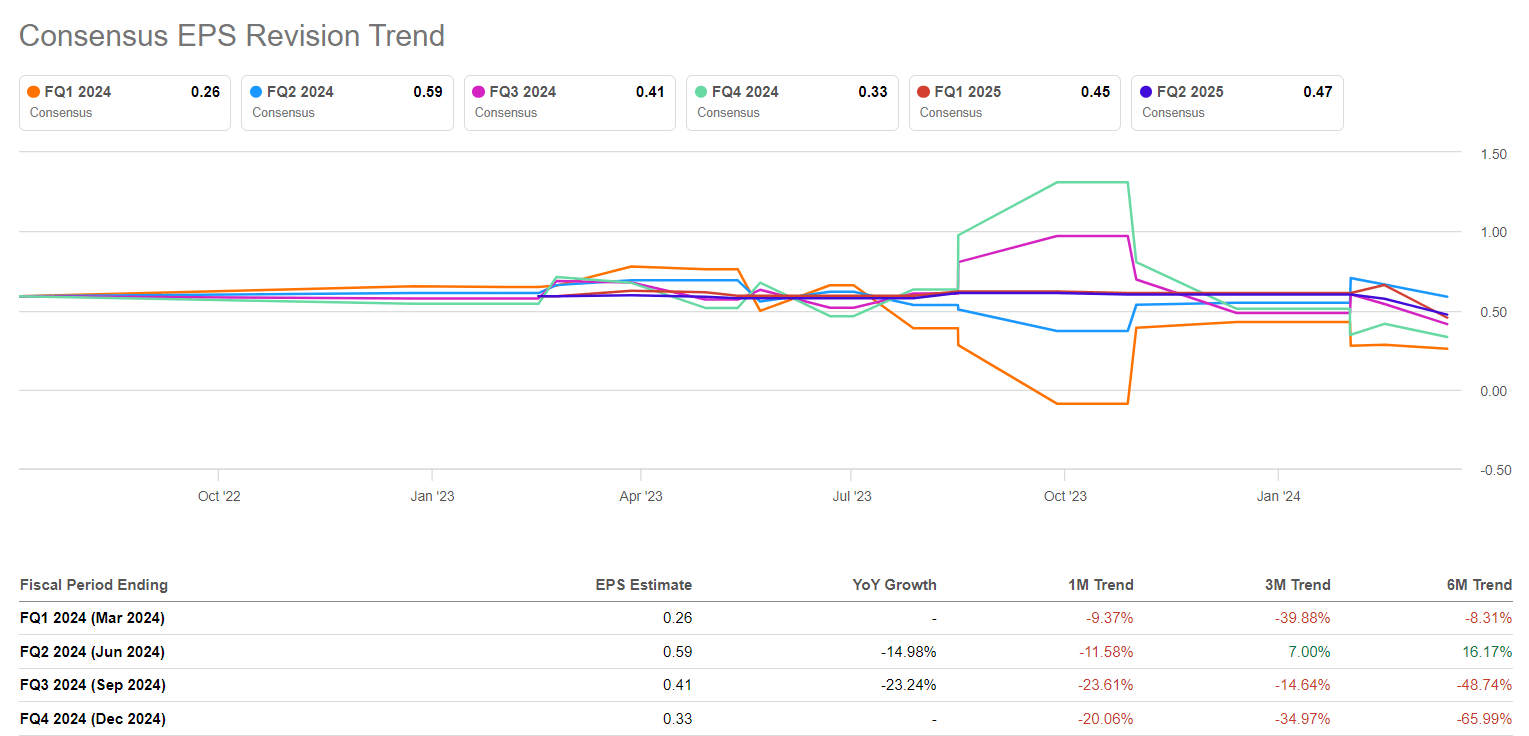

After CLF’s Q4 2023 results disappointed Wall Street in terms of revenue and GAAP EPS numbers, analysts have sharply reduced their expectations for several quarters ahead. In my opinion, this is something of an overreaction, as I don’t see any overtly negative premise for such a decision.

Seeking Alpha

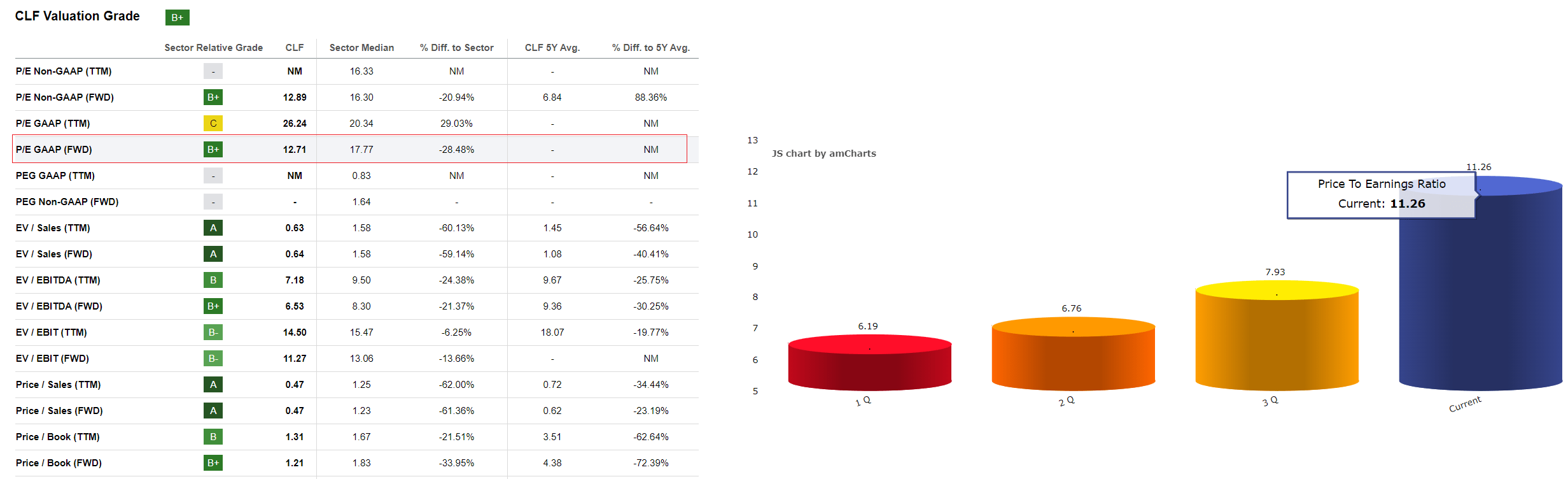

Looking at the current valuation of the CLF stock, it appears to be slightly above the current industry norm with a FWD P/E ratio of 12.71x (GAAP).

SA data, CSIMarket, Oakoff’s notes

It should be noted, however, that this forward-looking P/E ratio is based on the forecasts mentioned above. I have already noted that I think they are underestimated – so the most likely P/E ratio should be lower in my opinion, which is a reason for the stock to adjust higher.

Risks To Consider

I may be wrong and the CLF stock is already at around its fair value. This was the conclusion reached by the analysts at Argus Research (proprietary source) following the publication of the company’s Q4 2023 results. They downgraded the stock from ‘Buy’ to ‘Hold’ seeing a continuation of the down cycle in terms of pricing:

We view Cleveland-Cliffs as a well-run company with a strong track record in its industry. However, earnings are in a down cycle due to pricing. Current valuations to earnings appear reasonable, given the company’s long-term track record against the broad market. From a technical standpoint, the shares have been in a bearish pattern of lower highs and lower lows that dates to March 2022, which also gives us pause. We may look to get this well-managed company back on the BUY list if steel pricing does in fact improve, or if the share price falls back toward the $14-$15 level for nonfundamental reasons.

We must not forget that the steel industry is indeed very cyclical, and if you suddenly find yourself on the wrong side of the cycle, your long position can suffer badly. So far, prices have indeed fallen – I hope this will stop sooner than expected by the market today, but I could be wrong here. One can avoid risk either by placing stop-loss orders or by taking a longer-term position. I recommend the second option.

Your Takeaway

Despite the existing risks in terms of pricing and cyclicality, I think CLF has much more reason for margin growth in the medium term. In my opinion, the company is driven by strong management that prioritizes buybacks (10.4 million shares were repurchased in 2023 alone) and debt reduction. Combined with cost-cutting initiatives and a strong presence in the recovering automotive end market it should ultimately lead the company to super-strong financial results.

I keep holding CLF in my personal long-term portfolio and recommend you buy it too.

Good luck with your investments!

Q2 2024 Earnings Call Transcript")