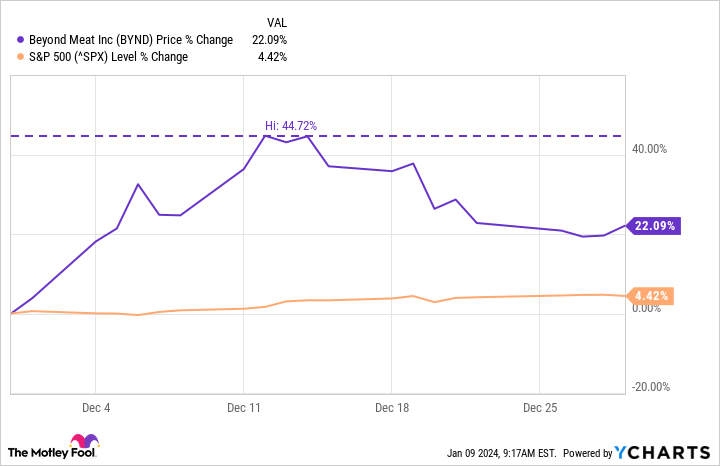

Shares of plant-based meat company Beyond Meat (BYND -4.91%) gained 22.1% in December, according to data provided by S&P Global Market Intelligence. The stock was up close to 45% in mid-December before slowly drifting back down, showing that most of the action for Beyond Meat was early in the month.

During December, Beyond Meat didn’t issue any press releases to investors. And the only filings with the Securities and Exchange Commission (SEC) pertained to stock trades from insiders — extremely common for all publicly traded companies at the end of the year. Therefore, there wasn’t any material news that would account for such a sudden upswing in the stock price.

This leaves a short squeeze as the most likely explanation for the big gains with Beyond Meat stock in the first half of the month.

For clarity, an extraordinary amount of investors are executing a trade that will profit only if Beyond Meat stock goes down — this is called shorting a stock.

In December, over 40% of Beyond Meat shares were sold short — that’s extremely high. When these investors want to get out of this trade (perhaps to take profits before the end of the year), they have to buy shares. If many investors decide to do this at the same time, that buying pressure can send the stock up in a hurry. This appears to be what happened in December.

Beyond Meat stock dropped fairly quickly in the second half of December, which again suggests that its first-half gain was the consequence of a short squeeze.

Why are so many investors betting against Beyond Meat?

A large number of investors are betting against Beyond Meat stock because the last couple of years have been bad for the company. And many believe that things will only get worse.

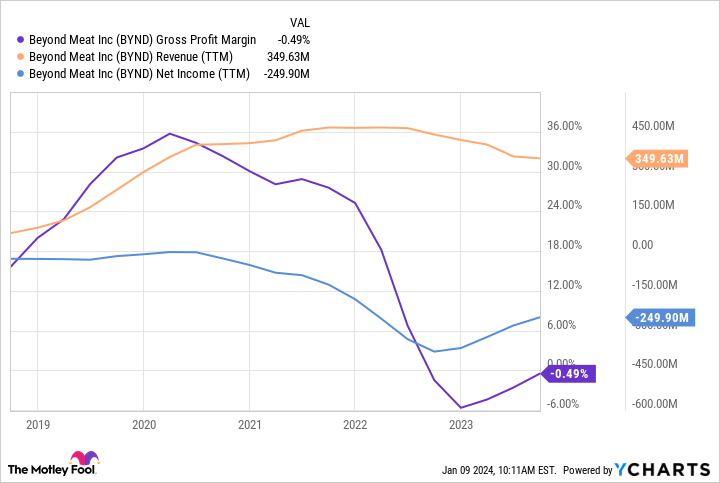

At the risk of oversimplifying things, Beyond Meat had a good gross margin for a food company when revenue was growing fast. And it operated close to breakeven. However, the company expanded its product lineup, and it wasn’t met by strong demand. Revenue growth consequently stalled. And to stimulate sales, management tried lowering prices, hitting margins and exacerbating losses.

BYND Gross Profit Margin data by YCharts

What’s next in 2024?

Beyond Meat’s management has implied that it will be raising prices in 2024. On the surface, that plan is sensible. After all, if the company has a gross loss, its prices are far too low.

However, Beyond Meat’s ultimate business vision was to siphon off a percentage of the trillion-dollar meat market by getting everyday consumers to eat plant-based meat at least some of the time. Gaining a significant number might have allowed it to manufacture its plant-based patties at a sufficient scale to lower its manufacturing costs and achieve profitability that way.

In short, Beyond Meat hasn’t quite found the audience it needed to have that advantage of scale. So now it’s forced to raise prices. That risks pushing more consumers away.

Jon Quast has positions in Beyond Meat. The Motley Fool has positions in and recommends Beyond Meat. The Motley Fool has a disclosure policy.

Q2 2024 Earnings Call Transcript")