It’s the home where you watched your children grow up, celebrated those milestone birthdays – and the one you fine-tuned over two or three decades into the best property you’ve ever owned. Filled with family heirlooms and fond memories, your forever home can be hard to surrender.

Yet leave it too late and you’ll struggle to manage the stress, the logistics and the whole admin process involved – I know only too well after managing the process for parents in their late-80s.

So when is the ideal age to give up the forever home and downsize? Or, to remove the negative implication of the word: to ‘right-size’.

While everyone faces different life-stage triggers – or obstacles – the country’s financial landscape is persuading some to consider it sooner rather than later.

A recent report by the estate agent Savills suggests that the number of downsizers active in the housing market increased by 53 per cent last year.

Bittersweet: Robert Dance is sorry to leave his £1.7million Surrey home, also pictured inset, but now needs a more practical location

Harry Gladwin, at The Buying Solution, says: ‘When it comes to downsizing, 60s are the new 70s. With higher interest rates and inflation on house maintenance, power, heating and wage costs, people are finding more and more reasons to move a decade earlier.’

Your 60s are the ideal time, agrees Jennie Hancock, of Property Acquisitions, a property finder in West Sussex.

‘When the children have left home, it’s time to start thinking about it. People often put it off, saying they will wait until after a wedding or a 21st, and then something else – but 70 to 75 is a serious cut-off point.

‘People will have the energy to embrace an exciting new chapter rather than settling for a rubbish old bungalow.’

Our children left home, so we downsized early

Claudine Frost, 55, and her partner Daniel, 47, are ahead of the curve – and are certainly not bungalow-bound.

Last July, they moved into an Art Deco apartment with co-working spaces and arts centre in a classic building, Hornsey Town Hall, in North London.

Freeing up cash and keeping living costs down persuaded them to move from their five-bedroom Victorian home in nearby Highgate.

‘When the children [aged 25, 20 and 18] left home, it seemed too large without them. I felt a bit lost and aware of the expense of maintaining a large Victorian house,’ says accounts assistant Claudine.

‘We loved the area but wanted an energy-efficient, new-build home with much lower running costs. This move has given us a new zest for life. It feels like a new beginning, rather than giving up something which ‘downsizing’ implies.’

When you stop using the space is a good time and reason to downsize, says Paul Cosgrove, of estate agent Finlay Brewer, adding: ‘But most people need something to happen to galvanise them – or being presented with a suitable alternative.

‘If they don’t have this, the lack of a plan can freeze them into inactivity.’

I don’t want to leave it too late

One of his sellers is very keen not to leave it too late – and risk being a burden on her family.

At 64, Emily Fletcher has put her four-bedroom townhouse in Brook Green, West London, on the market and wants a cosy two-bedroom cottage close to the Thames in Barnes.

‘After many happy years here, and the children now in their 30s, it’s time to allow another family to enjoy the house,’ says the former school secretary, who retired a year ago.

Putting in a stairlift (or three) up to her fourth-floor bedroom would not have been practical either, but some people do prefer to adapt their homes rather than move.

Only 91 per cent of UK homes are accessible to all, and the number of stairlifts being installed has increased tenfold over the past 20 years.

In cities, where many older homes are more than three or four storeys, it’s not always practical either.

Asset-rich but cash-poor retirees

‘A lot of retired people are asset-rich but cash-poor, so spending thousands on adapting their home is not an option,’ says Marc Schneiderman, of Arlington Residential. Weighing up the cost of adapting versus the cost (and upheaval) of moving is something to consider.

With the cost of installing a stairlift £3,000 to £10,000, and the expense of adapting a downstairs bathroom or installing a wet room being a similar amount, it can be less than the cost of moving when legal fees, estate agent fees, stamp duty and removal expenses are combined.

‘These are relatively simple adaptations that prolong people’s independence in their own home, but it doesn’t release larger houses into the market that are desperately needed for young families,’ says Mark Manning, of estate agent Manning Stainton in Yorkshire, on the wider implications.

‘Enquiries to us about downsizing have reduced in recent years as people are frustrated by the lack of alternatives.

‘Over the past year, we have had 1,700 buyers asking to buy a bungalow, yet in 2023 only 1,295 bungalows went to market in the Leeds-Wakefield area.

‘Homeowners say there’s no point in moving if they can’t find what they want.’

The amount of stamp duty to pay is another obstacle – especially on homes above the £925,000 threshold when the 10 per cent rate kicks in.

‘I have sellers moving from a £2 million house who only downsize by £500,000,’ adds Hancock. ‘For some, paying £90,000 in stamp duty is a deterrent.’

Empty nest to nest egg: Claudine Frost and partner Daniel sold a five-bedroom house to free up cash

Owner-occupiers aged 65-plus own homes worth as much as £2.735 trillion, and most of them are mortgage-free, according to Savills Research.

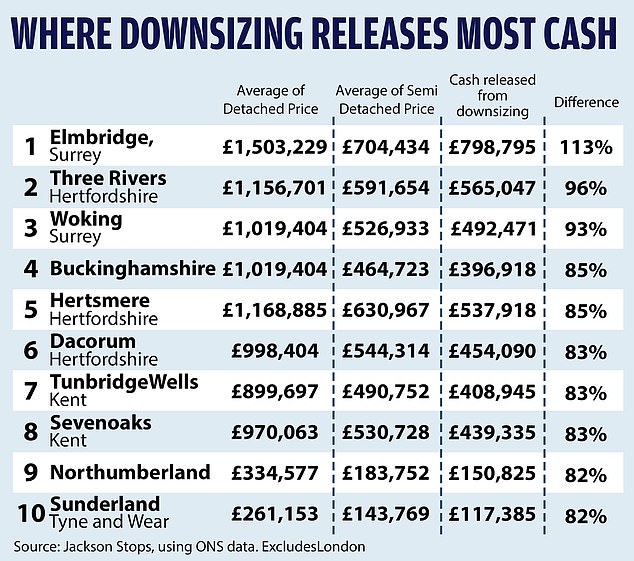

Meanwhile, in Jackson Stops’ annual research on the ‘downsizer gap’ – the money left over when moving from a detached house to a semi-detached house in England and Wales – the estate agent reports that the amount of released equity has increased by £5,467 to £209,215 between 2022 and 2023.

With the average deposit paid by a UK first-time buyer for a three-bedroom home last year at £34,500, according to Zoopla, many homeowners are desperately keen to release equity to help children or grandchildren on to the housing ladder.

This – or to fund retirement activities such as cruises – is the top priority for one in five downsizers and empty-nesters surveyed by Savills at the end of last year. The agent estimated that 164,000 first-time buyers received family assistance in getting their mortgage in 2023.

We moved to a retirement development at 60

Making the most of their early retirement with cruises and foreign holidays was perfect for Mandy and David Cobbs, yet it threw up worries about the security and the impact of extreme weather on their five-bedroom home in Oxfordshire when they were away.

So at the relatively young age of 60, they made the choice to move to a retirement development – Audley Cooper’s Hill, in Englefield Green, Surrey.

‘We spend a lot of time in California, where one of our children lives and considered retiring there as ‘lifestyle’ developments for over-55s have much younger populations than the ones here in the UK,’ says David, who used to work for Deloitte. ‘But we love the onsite gym and restaurant and enjoy much more freedom now.’

Moving to a more practical location is another incentive. Downsizers can be more flexible in their search compared with a few years earlier in their lives when they needed to be in a school catchment area or near a train station for commuting – but proximity to healthcare facilities becomes more crucial.

The best locations to retire to for this are Exeter, Worcester and Cheltenham, alongside the London suburbs of Merton, Richmond and Epsom, according to Savills.

I’m moving into London from the countryside

Robert Dance, 74, is making the move to London for such reasons, but an emotional attachment to the family home – an 18th Century farmhouse on nine acres in Hindhead, Surrey – makes the move bittersweet.

‘We moved here because my wife loved horses and wanted stables. When she died ten years ago, I wanted to stay here and keep her dream alive,’ he says.

‘Now I’m suddenly aware that time is ticking, and I’ve decided to move to Battersea to be closer to my partner and my son. I am ready for more hustle and bustle – and one last adventure!’

He doesn’t want to leave it too late and be unable to maintain his home – for sale at £1.7 million through Winkworth – especially with building costs higher than ever.

Carol Peett, of West Wales Property Finders, says: ‘I come across far too many people who are struggling to manage the house and garden, with the property becoming run down.

‘By that stage, they do not achieve the full price they would have done when at its prime, leaving them less money for their onward purchase and to live off.’

Lindsay Heydon, 62, moved last week when her seven-bedroom multi-generational family home on an acre of land became too ‘overwhelming’ to manage.

The family’s new five-bedroom home near Fishguard, in Pembrokeshire, Wales, needs a little work so she wouldn’t have left it any later. ‘It took months to find the home, deal with conveyancing issues and then physically move. I would not want to deal with that at 70.’

Charlie Wells, of buying agency Prime Purchase, likens the decision to downsize to selling shares. ‘Stop trying to work out when the top of the market is because you might miss it; far better to sell when it’s best for you.

‘Whatever you want to do, it is vital to avoid a forced sale because your health has deteriorated quickly. Not being in control of the timings is not a great place to be – make the move five years before you actually need to.’

In fact, today’s slower property market could be a good time to do it – despite higher mortgage rates and election uncertainty.

‘A couple of years ago when the property market was abnormal and frantic, it was more challenging for sensitive moves, such as an older couple downsizing,’ says Simon Roberts, at Strutt & Parker.

‘Today’s less competitive market is easier to navigate.’

Some links in this article may be affiliate links. If you click on them we may earn a small commission. That helps us fund This Is Money, and keep it free to use. We do not write articles to promote products. We do not allow any commercial relationship to affect our editorial independence.

Q2 2024 Earnings Call Transcript")