jetcityimage

My Thesis

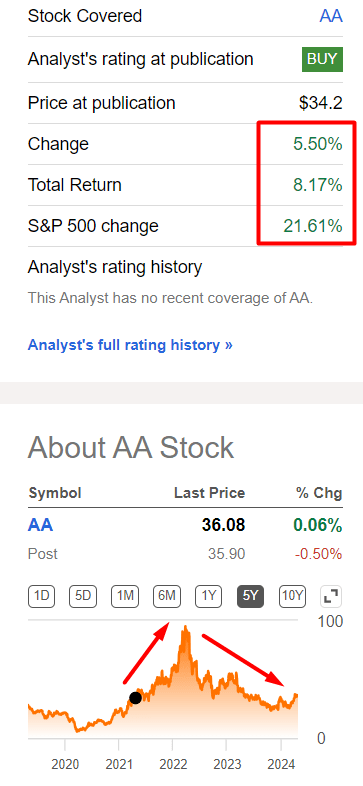

The only time I have written about Alcoa Corporation (NYSE:AA) was in April 2021 – my bullish thesis has aged poorly compared to the return of the S&P 500 Index (SP500), even though a potential investor has had the chance to take a huge profit in AA over the last 2 years.

Seeking Alpha, Oakoff’s notes

Despite the sharp sell-off since 2022, I think the tide is now turning back in AA’s favor. Furthermore, the reason that makes up this catalyst is actually hurting the demand side of the entire aluminum market. But because of some headwinds, I’ve decided to rate AA stock as “Hold” today.

My Reasoning

I don’t think it’s a secret to anyone that a lot has changed in the world since April 2021 – geopolitics has started to play a much bigger role than before. First of all, geopolitics has influenced, I would even say “hit” the aluminum market: After the start of the war between Russia and Ukraine, the pressure of sanctions on the Russian industrial sector has changed the balance of power on the global market.

I don’t want to go through the entire list of sanctions against Russia – the list is too long, and most of it has no relevance to Alcoa. However, what caught my attention was the comments made by people close to its direct global competitor – RUSAL – which, according to a recent Bloomberg article, is at risk of losing up to 36% of its sales due to the sanctions imposed by the UK and the US.

Rusal’s preliminary estimate is that the sanctions could impact at least 1.5 million tons of its annual sales, compared to its production of 3.8 million tons last year and sales of 4.2 million tons last year, the person said, asking not to be identified as they weren’t authorized to speak publicly. As a result, Rusal may be forced to reduce its production, the person said, comparing the situation to the global financial crisis that hit demand sharply in 2008.

As I see it, Rusal faces major challenges as it is losing its position in the EU market, with industrial customers likely to self-sanction and smaller customers expecting further EU sanctions. I think we may see a domino effect here as the EU usually follows US sanctions with some delay – this possibility could result in Rusal losing its market share in the EU by the fall of 2024, resulting in a significant loss of sales of over 1.5 billion in 2023 (based on Rusal’s official filing). While Rusal struggles, Alcoa seems to benefit from the rise in metal exchange prices (Rusal won’t be able to). Just as with capped prices for Russian oil, Rusal will likely have to offer discounts to retain customers, allowing Alcoa, Rio Tinto (RIO), and Norsk Hydro (OTCQX:NHYDY) to attract large customers seeking alternatives to Russian metal sources.

Furthermore, aggressive efforts by the US to coerce third-party nations, such as Turkey and China, into severing ties with Russia, further complicates the landscape, posing a direct threat to Rusal’s supply chain, especially considering the interconnected nature of its global manufacturing networks.

So thinking about possible sanctions applications, the Russian aluminum giant – once the largest company of its kind in the entire world – is now may be gone. Faced with the impossibility of surviving in developed markets and selling its products there, Rusal is finished in its current form – now the company must look for new ways to survive, and that will take time.

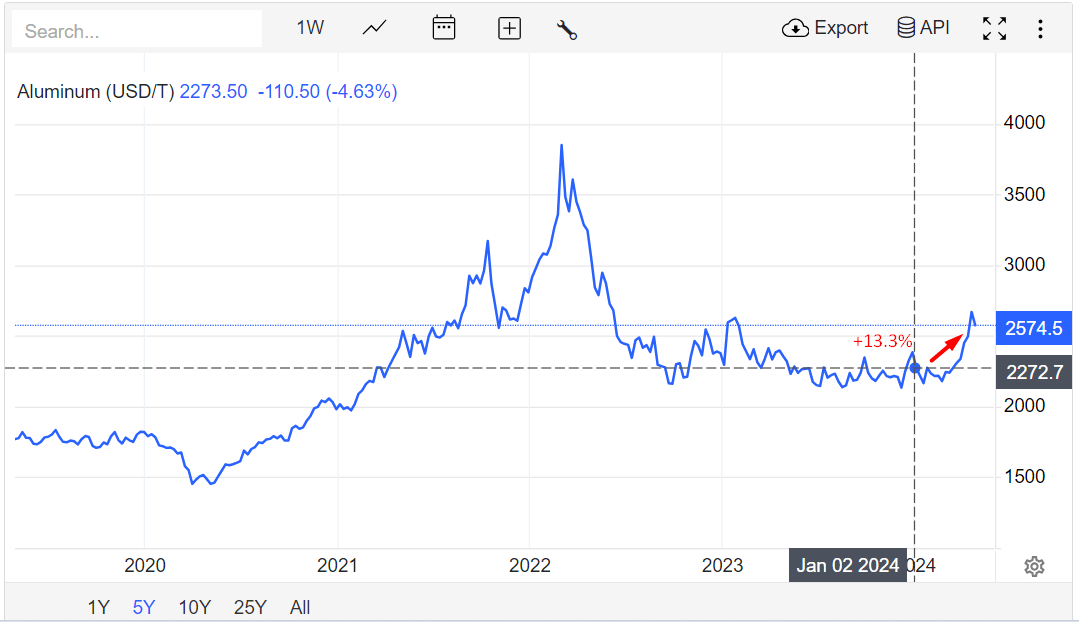

In light of the ban on Russian aluminum deliveries to the LME and additional operational risks, Rusal may prepare for a potential reduction in physical production volumes reminiscent of the downturn experienced in 2008 during the global financial crisis. Given the risk of the supply cut, aluminum prices have already risen by more than 13% YTD.

TradingEconomics, Oakoff’s notes

Most likely, the whole situation will continue to have a strong tailwind for aluminum prices because from the point of view of fundamental factors – primarily deficit – everything indicates that there will be a shortage of this important industrial metal in the world for the next few years. Here’s how Goldman Sachs’ commodities research team looks at this situation (proprietary source):

… as the volatility generated by these LME rule changes ultimately dissipates, we continue to see a significant global primary metal deficit developing over the next 12 months which underpins an eventual sustained path higher, reflected in our $2700/t 12M price targets and $2850/t 2025 price average.

Goldman Sachs [proprietary source]![Goldman Sachs [proprietary source]](https://static.seekingalpha.com/uploads/2024/4/25/53838465-17140207255568404_origin.png)

In my opinion, the artificial environment created by the new sanctions is damaging the demand side of the market. According to TradingEconomics, the US Manufacturing PMI has fallen for the second consecutive month to its lowest level (49.9) in 4 months. This means that demand in the country’s manufacturing sector is not the strongest right now, and the rising prices for one of the most widely used metals in manufacturing don’t help to reverse that. The situation in Europe seems way more bleaker:

Also, manufacturing input prices continued to fall, helped by improved supply conditions. Otherwise, the picture remains rather bleak, with new business continuing to decline rapidly, along with order backlogs. Weak demand for industrial products was also evident in the sharp decrease in the volume of purchased inputs and the absence of a turnaround in the inventory cycle.

On the other hand, it cannot be said that demand on the global market is now at a depressed level or threatens to fall to such a level in the foreseeable future. This is the impression conveyed by Alcoa’s latest financial results: despite declining sales in Q1 2024, the company’s adjusted EBITDA increased by 48% QoQ as the adjusted EBITDA margin rose from 3.4% in Q4 2023 to 5.1% in the most recent quarter. The company’s net loss is also actively shrinking, improving from -$1.30 per share in 1Q 2023 to -$0.81 per share in Q1 2024 (though it missed the consensus estimate). In addition, the latest guidance also indicates relative stability in demand as far as I see it. According to the recent earnings call, Alcoa’s projected aluminum shipments are expected to range between 12.7-12.9 million metric tons, aligning closely with 2023 figures but slightly lower than 2022. Within the aluminum segment, shipments are forecasted to remain consistent at 2.5-2.6 million metric tons, mirroring levels seen in both 2023 and 2022. Production forecasts stand at 9.8-10.0 million metric tons for aluminum and 2.2-2.3 million metric tons for aluminum.

So if we try to draw an intermediate conclusion from all this data and the latest news, I think it is most logical to conclude that demand in the market should theoretically take a hit due to rising prices (and the threat of continued growth). The big “but” here is that manufacturers seem to be accepting the new reality relatively easily and are overpaying as demand remains fairly strong despite the recent price increase.

Thus, I think that Alcoa’s production numbers may be even higher shortly than currently anticipated by the market. It’s not just Rusal facing risks of reduced production and supply chain disruptions. The sanctions fundamentally undermines their business and reduces competitiveness. Though it’s likely bad for consumers in the long run, it’s very beneficial for Alcoa in the medium term. Alcoa could capitalize on this situation by capturing additional market share, particularly in segments such as semi-finished and value-added products where Rusal has a significant presence.

Being one of the largest producers in the world, I believe Alcoa’s ability to maintain stable supply chains and traceable product origins could enhance its appeal to customers seeking alternatives to Rusal amidst geopolitical tensions and regulatory uncertainties. In the face of shrinking competition, Alcoa now appears to have bargaining power with counterparts when it comes to material prices – so the management’s actions to improve profitability could bear even more fruit.

Furthermore, my technical analysis suggests that AA stock could still rise by more than 10% before meeting its first major resistance level. The medium-term target is $53-54 per share, suggesting ~48% upside potential in the mid-range if the company really manages to increase its market share relatively quickly.

TrendSpider Software, Oakoff’s notes

However, I have certain concerns about the realism of my calculations above.

One potential headwind for Alcoa is the operational challenges and financial implications associated with the acquisition of the joint venture with Alumina Limited. This move should improve vertical integration and control over aluminum and aluminum production, but on the other hand, it involves significant upfront costs and regulatory approvals. Also, as another SA analyst Michael Del Monte wrote recently, Alcoa’s San Ciprian complex is proving unprofitable and poses cash flow issues without government support or energy price relief – the need to find a buyer for this facility in light of operational challenges could result in an impairment or discounted sale, which may further impair the company’s financials. These operational risks, in my opinion, should put pressure on the stock going forward.

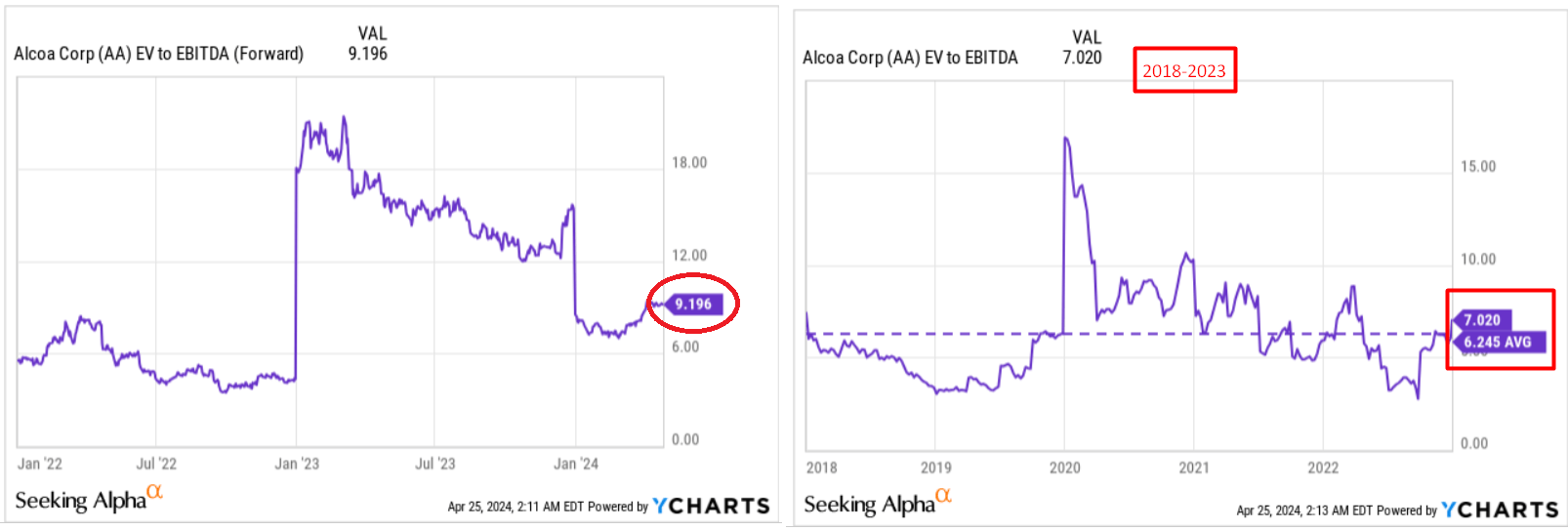

The second worrying moment is today’s valuation of AA. Right now, Alcoa is trading at an FWD EV/EBITDA ratio of ~9.2x, which is 40-50% above historical normal. This means that even if we assume that Alcoa’s actual EBITDA figure next year will be 50% higher than today’s consensus expects, the company only appears fairly valued in this bullish scenario and not undervalued.

YCharts, Oakoff’s notes

To obtain the “bargain Buy” status, the company’s EBITDA must grow 2-3x in the foreseeable future – this is possible, but the abundance of risks does not allow us to make such an assumption. I therefore rate AA as a “Hold” today, but admit that the development prospects now look very positive given the reduced competition.

Your Takeaway

The potential impact of sanctions on Rusal should definitely lead to supply chain disruptions and opportunities for Alcoa to gain market share, in my view.

Rising prices in the aluminum market related to the recent events surrounding the sanctions should theoretically reduce demand – the heaviest blow, in my opinion, is likely to be in Europe. But overall, global demand appears to remain relatively stable. Market fundamentals suggest a continued rise in aluminum prices – Alcoa should benefit amid its reiterated production guidance.

However, the operational risks are quite high – as are the current multiples such as EV/EBITDA. Alcoa’s EBITDA should be well above consensus growth, which I am not yet convinced of. I have therefore decided to rate Alcoa as a “Hold” today.

Good luck with your investments!

Q2 2024 Earnings Call Transcript")