U.S. oil production has touched its highest level on record, and exports of the commodity are on the rise, but a hit to prices from a potential slowdown in demand and a lack of sufficient pipeline capacity may prevent the U.S. from reaching independence any time soon when it comes to oil.

The U.S. is not currently a net exporter of oil, and is not likely to become one within the next five years, wrote Bill Weatherburn, commodities economist at Capital Economics, in a research note dated Wednesday.

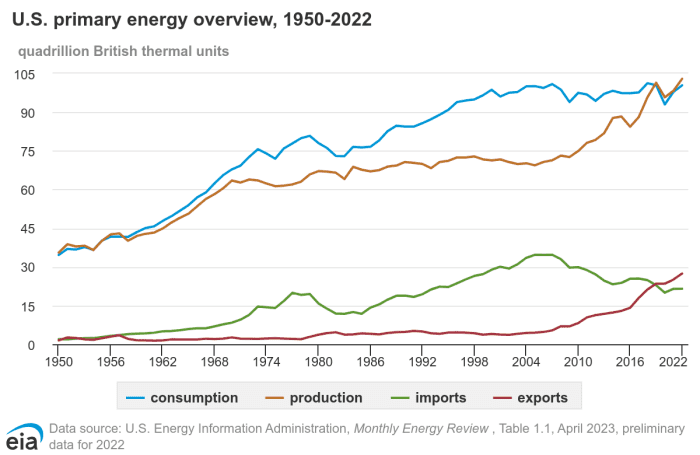

Ideally, oil independence would mean that the U.S. doesn’t import oil to meet its needs, and instead relies on domestic supplies.

In that sense, it would be good to point out that total energy exports — which include crude oil, petroleum products, natural gas, and coal — were the highest on record in 2022, at about 27.41 quadrillion British thermal units (quads), exceeding total energy imports of around 21.47 quads by about 5.94 quads, the largest margin on record, data from the EIA show.

The U.S. has been an annual net total energy exporter since 2019, according to the EIA.

U.S. total energy exports were the highest on record in 2022, according to the EIA.

U.S. Energy Information Administration

Still, Weatherburn said that to be clear, the U.S. is not energy independent, given that oil and natural gas are still imported each year to “overcome a variety of practical constraints that make it uneconomical for domestic consumption to be solely sourced from domestic production.”

Data from the EIA show that the U.S. imports more crude oil than it exports.

For the week ended Jan. 5, the U.S. imported 6.241 million barrels of crude oil per day and exported 3.322 million bpd, according to the EIA. In 2022, the U.S. imported about 6.28 million bpd of crude oil and exported around 3.6 million bpd.

Weatherburn said oil production would need to rise to over 17 million bpd before the U.S. was “reliably a net [oil] exporter.”

He said that post-pandemic trends suggest that for every 1 million bpd increase in oil production, net imports fall by roughly 0.5 million bpd, implying that crude production would need to rise by a further 5 million bpd, to over 17.5 million bpd for the U.S. to become a net oil exporter.

But output is unlikely to reach that level, with oil prices likely to come under “downward pressure from slowing global demand growth and greater supply from producers in the Middle East, said Weatherburn.

Record U.S. oil output looks to pressure prices

At 13.2 million barrels a day for the ended Jan. 5, U.S. oil production already stands near a record. Output climbed to 13.3 million bpd for the week ended Dec. 22 and may continue to climb.

In a monthly report issued Tuesday, the EIA said average oil output is likely to reach 13.2 million bpd in 2024 and more than 13.4 million bpd in 2025, both of which would mark record highs. It attributed its expectations for production growth over the next two years to increases in “well efficiency.”

Also see: EIA expects solar to lead U.S. power generation growth as coal demand drops

“U.S. oil production was rampant last year and is expected to remain strong this year, putting some downward pressure on global oil prices,” said analysts at Oxford Economics, in a recent note.

They expect U.S. benchmark West Texas Intermediate crude-oil prices

CL.1,

to average around $70 a barrel in the fourth quarter of this year, which they pointed out would be down about 15% from the average in the final three months of last year.

On Wednesday, WTI crude for February delivery

CLG24,

settled at $71.37 a barrel on the New York Mercantile Exchange.

Still, “risks to the forecast for oil prices are weighted to the upside,” the Oxford Economics analysts said, even if domestic oil production exceeds expectations because of geopolitical tensions and “potential stricter enforcement/extension of voluntary cuts in daily oil production by OPEC+.”

Read: Record U.S. oil production sparks battle for market share with Saudi Arabia and OPEC+

In the short turn, they said the price needed to “justify production can fluctuate and indications are that oil prices will remain high enough that it should be another solid year for U.S. oil production.”

They said that if their forecast for oil prices is correct, prices will remain above the break-even price for domestic oil producers given that, according to the Dallas Fed, oil prices need to average $62 a barrel for U.S. producers to drill.

Challenges

Still, energy infrastructure issues are set to remain a challenge in the oil sector, said Capital Economics’ Weatherburn.

He pointed out that there are no crude-oil pipelines that link major oilfields in the central U.S. to oil refineries on the east coast, and many U.S. refineries are more efficiently run using heavy grades of crude oil, which the U.S. shale sector does not produce.

Given that, the U.S. is “never likely to be energy independent while fossil fuels are a key part of the energy mix,” said Weatherburn.

Meanwhile, shale companies appear committed to a strategy of returning profits to their shareholders rather than maximizing production growth, he said.

Capital Economics also expects crude-oil prices to decline from 2025 as output from low-cost Middle Eastern producers with plenty of spare capacity expands, and electric vehicle sales gradually weaken global oil demand, said Weatherburn.

“Lower oil prices will reduce investment in new wells and weigh on U.S. production,” though the decline should be “gradual,” he said.

And “without a significant rise in crude production, the U.S. will not become a net exporter of crude oil for any prolonged period of time,” said Weatherburn.

“Instead, we expect U.S. crude production to peak in 2024 and then decline gradually thereafter,” he said.

Q2 2024 Earnings Call Transcript")