Maxxa_Satori

Welltower Inc. (NYSE:WELL) is a healthcare real estate investment trust that fell on hard times during the Covid-19 pandemic. The trust, however, is profiting from a recovery in net operating income as occupancy trends are improving.

Welltower also slashed its dividend payout by 30% in 2020, but I do see potential for the real estate investment trust to grow its dividend moving forward.

Importantly, long-term trends in the healthcare segment on which Welltower is focused, the senior healthcare market, have positive trends, including the aging of the U.S. population and growing healthcare spending.

Welltower is selling for an expensive FFO multiple, but the long-term demand trends and well-covered 3% dividend justify it.

My Rating History

Welltower has done well since my last piece in 2022: The trust continues to profit from a recovery in the senior housing part of its operating portfolio.

Taking into account the solidity of the underlying net operating income and funds from operations drivers, an aging U.S. population, and a long-term upswing in healthcare expenditures, I think that Welltower is a perfect retirement stock for investors who want to produce recurring income.

Portfolio Composition And Recovery Potential

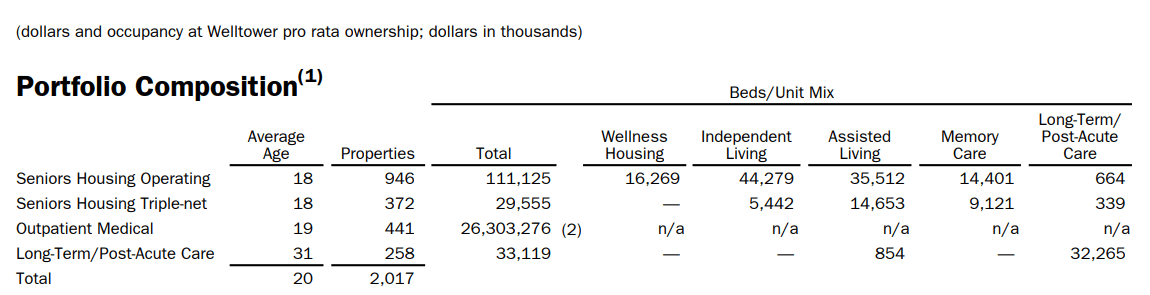

Welltower owns a large portfolio of healthcare properties that serve the needs of, mostly, the senior population. Senior housing is Welltower’s anchor segment and it consists of more than 2,000 properties, mostly Senior Housing facilities that help the elderly live normal lives in their advanced stages of life.

Other facilities include outpatient medical properties as well as long-term/post-acute care facilities which complement Welltower’s Senior Housing focus. The entire portfolio, on a same-store basis, produced $466 million in net operating income in 3Q-23, reflecting 14.1% YoY growth.

The largest portion of this growth came from the Senior Housing Operating portfolio which achieved 26.1% YoY growth and produced same-store net operating income of $239 million.

Portfolio Composition (Welltower)

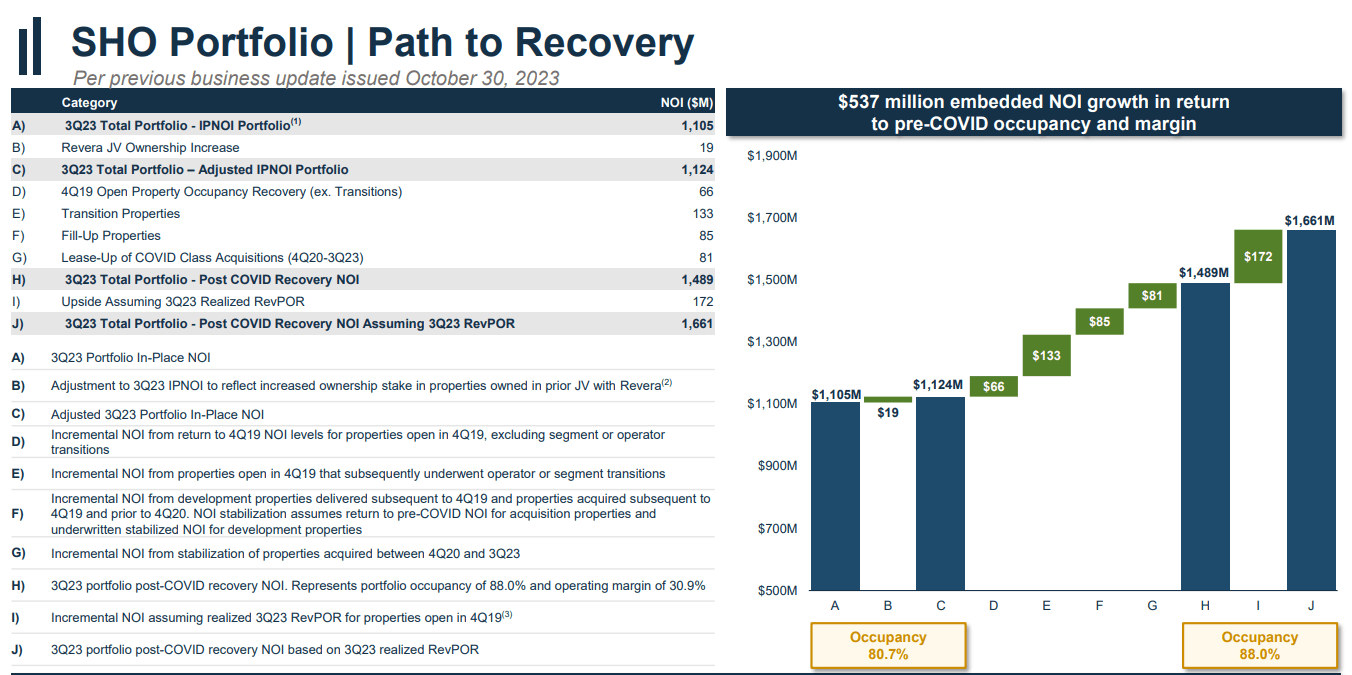

The recovery in the Senior Housing Operating portfolio is an ongoing theme and one that indicates that the healthcare real estate investment trust is poised to capture incremental net operating income upside in 2024.

The main driver of Welltower’s net operating income upside relates to an underlying recovery in occupancy in the Senior Housing segment.

Healthcare trusts have seen a rise in vacancies at the beginning of Covid-19, but occupancy rates have climbed steadily higher since and reached, for Welltower’s Senior Housing Operating portfolio, 88% in 3Q-23.

The trust sees $537 million in net operating income upside in its Senior Housing portfolio moving forward as Welltower recaptures lost gains resulting from the Covid-19 pandemic.

The trust’s forward-looking expectations suggest that passive income investors could profit from this ongoing net operating income recovery through a potential dividend raise. In 2024, the defining theme for Welltower will be to how much incremental net operating income potential the trust can unlock.

Since occupancy trends are generally improving, I think that Welltower has net operating income upside surprise potential.

Path To Recovery (Welltower)

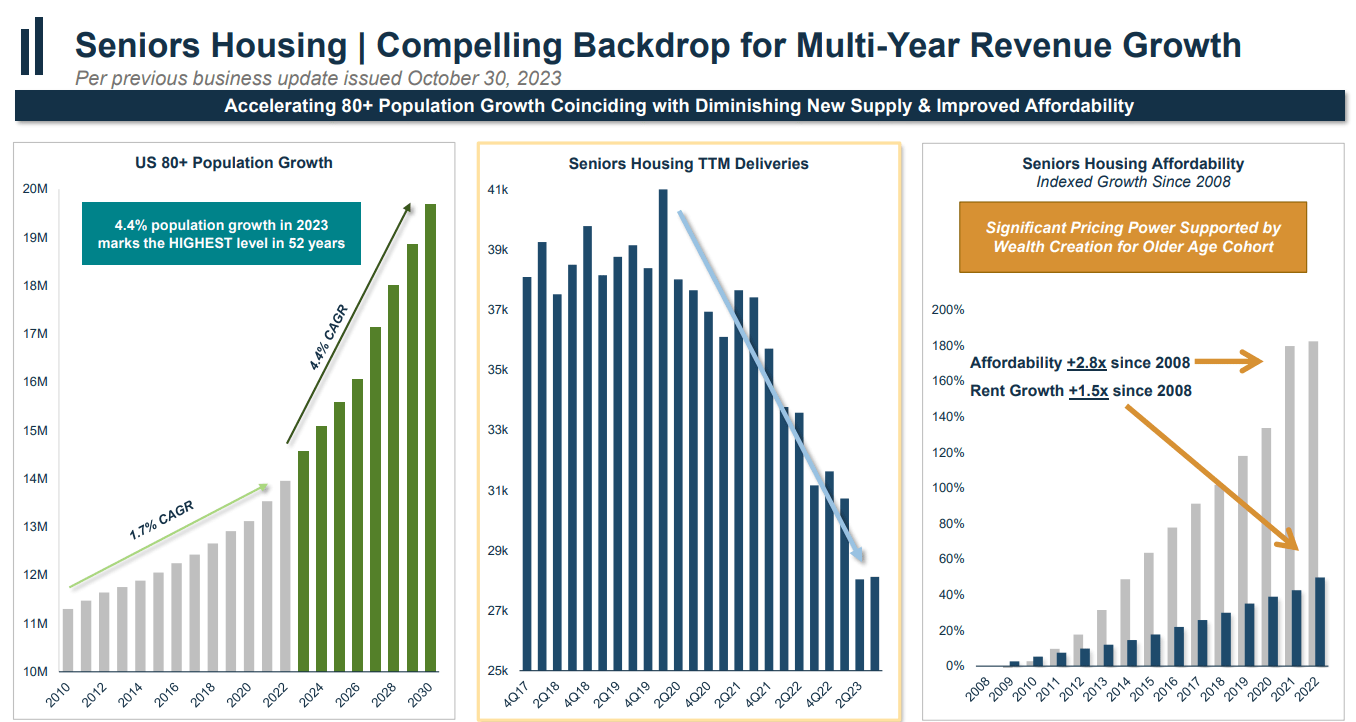

Two Long-Term Growth Trends

There are two long-term growth trends that will drive Welltower’s net operating income and funds from operations long-term.

One is the rise in the elderly population which is widely understood, I think, and relates back to growing demand for healthcare facilities that can accommodate the elderly. The 80+ population particularly is growing quickly, creating demand upside for Welltower’s Senior Housing real estate assets.

Backdrop For Multi-Year Revenue Growth (Welltower)

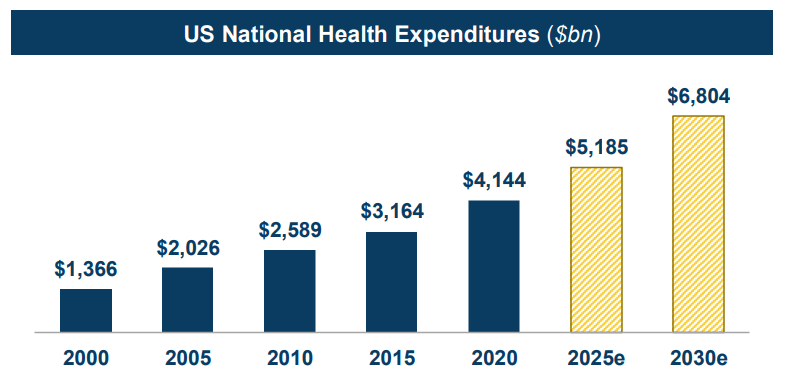

The second trend is the growth in health expenditures which are projected to soar together with the rise in the elderly population which makes intuitively sense: The older people get, the more money they tend to spend on healthcare, therefore creating a big upswing in the cost curve in the coming decades. U.S. Health Expenditures are set to rise to almost $7 trillion by 2030, reflecting a 65% jump compared to the 2020 base year.

U.S. National Health Expenditure (Physicians Realty Trust)

Acquisitions As A Catalyst For FFO Growth

I anticipate that the REIT will also look more towards incremental net operating income and funds from operations growth through new acquisitions in 2024 that could add to Welltower’s funds from operations and improve its ability to pay a higher dividend.

The trust broadly profits from recovery trends in its Senior Housing segment so I can see management doubling down on this opportunity to become more active in terms of acquisitions in 2024.

The combination of organic net operating income growth in Senior Housing and acquisition-driven funds from operations growth might also be an opportunity for passive income investors to profit from the potential upside related to the company’s busy acquisition schedule.

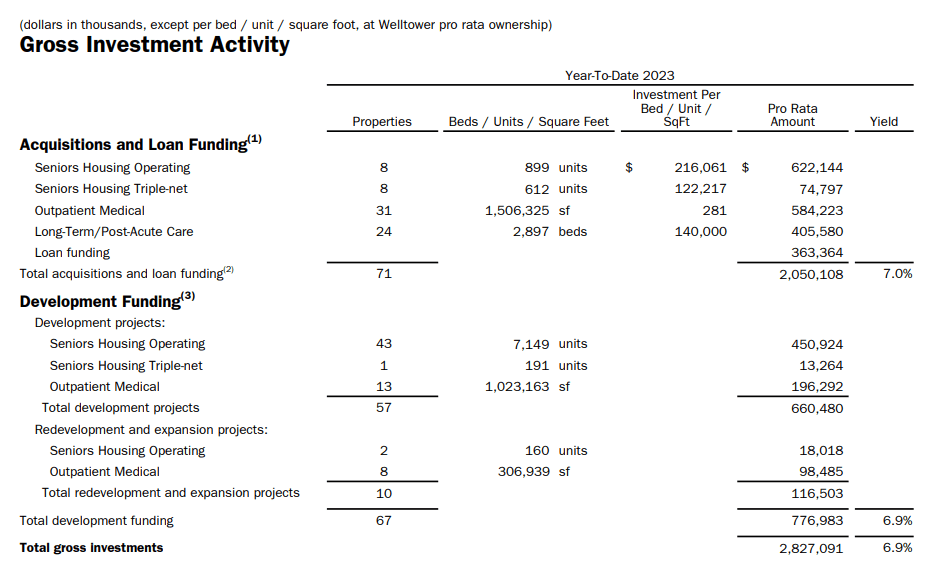

Welltower had an active year in terms of acquisitions in 2023, one of the most active years in its history in fact, as the company continued to go full-steam in on deploying its investment capital.

Welltower made gross investments, acquisitions and developments, totaling $2.8 billion in the first three quarters of 2023 while at the same time disposing of $850.1 million, leading us to a net investment of $2.0 billion.

In its business update from January, the trust said that it completed investments (pro rate) of $2.8 billion in 4Q-23, so the trust is heading into 2024 with a lot of acquisition momentum. Welltower invested particularly heavily in outpatient senior housing units as well as long-term/post-acute care facilities.

Gross Investment Activity (Welltower)

Pay-Out Ratio, Potential For Dividend Growth, FFO Multiple

Welltower, due to the Covid emergency in 2020, slashed its dividend by 30% and the dividend has since settled at $0.61 per share per quarter. However, I think that Welltower has considerable potential to grow its dividend as the trust’s net operating income and funds from operations recovery continue.

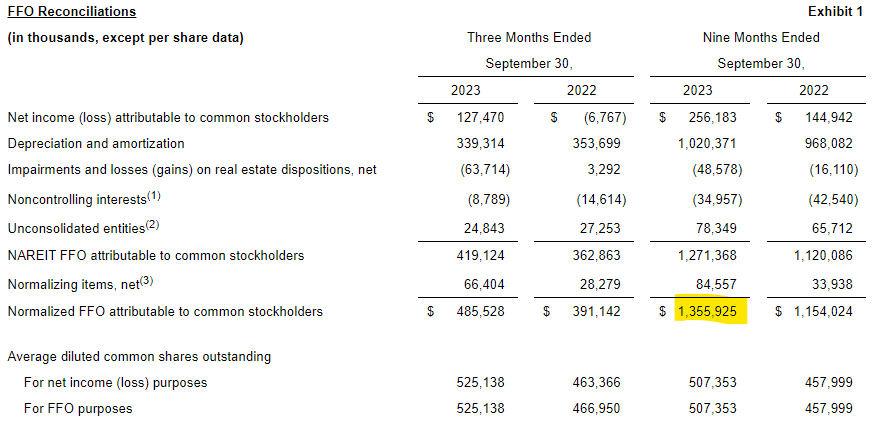

Welltower’s FFO (normalized) was $1.36 billion in the first three quarters of 2023, reflecting 17% YoY growth. Using the outstanding number of shares as of September 30, 2023, 507K, yields a normalized FFO of $2.67 per share.

Welltower paid a stable $0.61 per share dividend in each quarter in 2023 which implies a 69% dividend pay-out ratio. In the same period a year ago, Welltower paid out 73% of its normalized FFO, reflecting a small improvement in the pay-out ratio in 2023.

FFO Reconciliations (Welltower)

Both the growth in funds from operations, which is a direct result of a net operating income recovery in the Senior Housing portfolio and the low pay-out ratio suggest that Welltower could afford to hike its dividend.

Welltower is a well-managed healthcare trust and seems to be optimistic about its property performance in 2023. A few months ago the trust revised its normalized funds from operations outlook from $3.51-$3.60 per share to $3.59-$3.63 per share. The outlook reflects a YoY growth rate of 8%.

Playing with a 5% YoY growth rate in funds from operations for 2024, Welltower could be on track to earn $3.80 per share in normalized funds from operations this year which in turn reflects back to us a 23.4x FFO multiple. The high multiple probably reflects Welltower’s improved net operating income potential after Covid-19 and it is a premium multiple for sure.

With that being said, the dividend is also very well-covered and should rise moving forward.

Ventas, Inc. (VTR) is another healthcare trust with large investments in the senior housing market. The trust sees $2.96 – $2.99 in normalized FFO in 2023 which comes out to a 16.0x FFO multiple.

Ventas profits, like Welltower from a recovering senior housing market and I own both trusts in my passive income portfolio.

I do like Welltower due to its organic growth opportunity in the senior housing core market, its net operating income recovery, and the potential to do more acquisitions and grow its dividend moving forward.

Why I Think A Premium Multiple Is Justified

Ventas is obviously the cheaper choice for a relatively similar operating portfolio, but that is not to say that Welltower does not reflect value for passive income investors.

Welltower is about twice the size of Ventas and also has a much higher property count in its portfolio: 2,017 compared to 1,381, which is preferable from a diversification point of view.

In the senior housing portfolio, Welltower is seeing stronger same-store net operating income growth on a YoY basis: Welltower reported 26.1% net operating income growth in 3Q-23 whereas Ventas’ shop segment produced ‘only’ 18.2% growth. The outlook for 2023 implies 23-26% growth in same-store net operating income for Welltower and 17-19% for Ventas’ Shop segment (Senior Housing).

I think this stronger recovery in the senior housing segment as well as Welltower’s aggressive stance with respect to acquisitions, make Welltower a more promising bet on a growing dividend.

Ventas also slashed its dividend at a higher percentage than Welltower in 2020, 43%, which probably can help give an explanation as to why Ventas is cheaper than Welltower.

Why The Investment Thesis Might Be Wrong

I don’t think that the underlying drivers discussed in this article are hard to argue with. The U.S. population is aging and demand for senior housing facilities is only going to increase in future decades. The degree to which Welltower can profit from this growth depends on how prudently the trust’s management can grow its portfolio.

If the trust grows too quickly and another Covid-like pandemic strikes, then Welltower may have to deal with a 2020-like scenario again that destroys its occupancy and net operating income recovery.

My Conclusion

Welltower is poised to profit from two major secular growth trends in the United States:

- An aging population; and

- Rising health expenditures.

Both trends fundamentally support an investment in Welltower which has positioned itself to profit from these trends through its investments, mainly, in Senior Housing facilities.

As a consequence, Welltower is seeing a solid net operating income upside and though the stock is not cheap, it pays a healthy 3% dividend yield.

I think that Welltower is a perfect retirement stock for investors who seek to produce long-term dividend income from a well-managed senior healthcare-focused REIT.

Q2 2024 Earnings Call Transcript")