Tom Werner/DigitalVision via Getty Images

I have covered Weave (NYSE:WEAV) on three previous occasions, each of which were ‘Buy’ recommendations:

As part of these analyses, I highlighted several reasons to be bullish on Weave, including their transition to positive free cash flow, their position on the cusp of GAAP-profitability, and their modest valuation, among others.

In this article, I will discuss my main takeaways from Weave’s Q1 2024 earnings report, provide an updated intrinsic valuation, and reiterate my ‘Buy’ rating for the stock.

Gross Margin Expansion

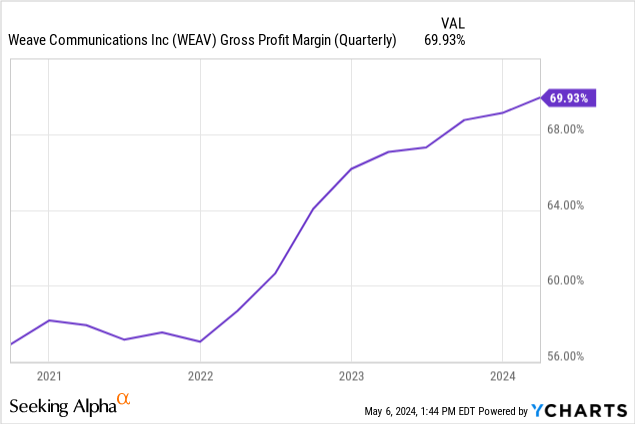

Weave continues to make considerable progress on expanding their gross margin. Their Q1 2024 gross margin was 69.9%, representing their ninth consecutive quarter of gross margin expansion. Weave has certainly come a long way since their IPO in 2021, when their gross margin was just 57%.

Management attributes much of this margin expansion to their transition to higher margin upsells, such as their payments service. To see Weave’s margin expand by almost 1300 basis points in just a couple of years is reassuring for investors and reflects positively on management’s ability to drive greater profitability.

In their earnings call, management doubled down on the idea that they see Weave in the long-term as a 75-80% gross margin company. They noted that the payments portion of their business will continue to help drive their margin upward. Additionally, management mentioned that they have raised overall prices slightly over the last year and have had little to no pushback from customers. This indicates that they have pricing power with their customers and are providing ample value through their products. Couple these two things together–higher margin services and pricing power–and management’s goal for 75-80% gross margins appears achievable.

Raising 2024 Revenue Guidance

After exceeding their top-end revenue guidance for the ninth consecutive quarter, management announced that they are also raising their 2024 revenue guidance. Weave management now anticipates 2024 revenue to be between $197 million and $200 million. The company finished 2023 with just over $170 million of revenue.

If they were to hit the top end of their revenue guidance once again, it would represent ~17% year-over-year revenue growth. Considering that Weave’s year-over-year revenue growth rates in 2022 and 2023 were 22.7% and 20%, this seems more than achievable. Furthermore, management’s consistent ability to over-deliver instills confidence in their ambitious goals for the future.

Growth In Net Revenue Retention

Weave saw net revenue retention increase slightly from 95% to 96%. Once again, this growth was fueled by their payments service. Many software companies have attractive net revenue retention rates due to their usage of seat-based pricing models. However, the goal of Weave’s software is to limit, and even eliminate, the number of employees that are required by their customers. Therefore, Weave can’t benefit from seat-based pricing.

Due to this predicament, Weave has to rely on other ways to increase their revenue from existing customers. Thus far, Weave has relied on expanding their product offering and upselling customers to increase net revenue retention. This has worked well for them up to this point and appears to be management’s mindset for continuing to improve net revenue retention moving forward.

Cash Flow Fluctuation

As part of their Q1 earnings, Weave reported a loss in cash from operations of $19.7 million. This is down significantly from their Q4 total of $3.7 million of cash generated from operations. However, management made clear on their earnings call that this steep loss was due to a one-time event. Alan Taylor, Weave’s CFO, explained the situation:

We successfully implemented a new billing system in Q1 that necessitated deferring March subscription billings into April. This resulted in a one-time increase in our accounts receivable balance as of the end of March and a corresponding decrease in free cash flow of approximately $15 million.

Since the vast majority of our billings are done via credit card, cash is received within a few days of billing and our accounts receivable balance will be back to normal levels in Q2. There will be an associated positive impact on Q2 free cash flow of approximately $15 million.

Also, as I mentioned last quarter, we paid out our 2023 annual employee bonuses in Q1 of this year, which amounted to approximately $7 million. In prior years, annual bonuses were paid out in Q2. Excluding the impact of both the delay in billing and the timing difference of the bonus payout, free cash flow would have been positive for Q1.

Essentially, Weave took a hit to their free cash flow this quarter due to a billing system change, as well as paying out employee bonuses earlier than they have been paid in the past. However, Weave will experience a bump in free cash flow of approximately $15 million in Q2 as their accounts receivable balance normalizes.

Market’s Reaction

To recap, Weave’s earnings report highlighted robust gross margin expansion, revenue exceeding guidance, raising 2024 revenue guidance, and growth in net revenue retention. The only negative from their earnings release was their one-time cash flow fluctuation that will be made right in Q2.

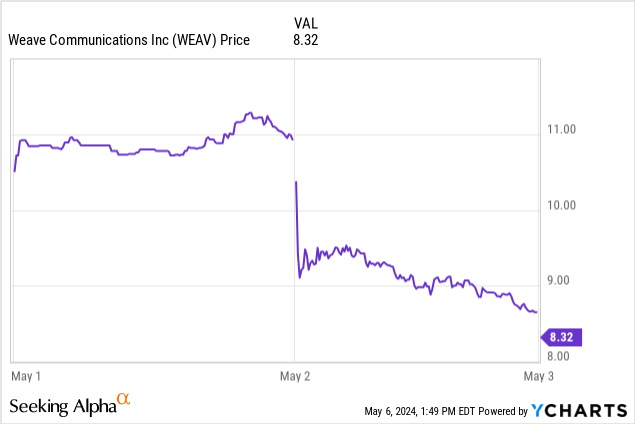

So, how did markets react? Not well. In fact, Weave’s stock, which was trading for around $11.20 per share prior to the earnings release, was down over 20%. Today, shares are trading for around $8.40.

It appears to me that the market overreacted to Weave’s sizable loss in cash from operations due to their billing system change. However, this fluctuation will be made right in Q2, making me believe that it doesn’t merit a 20% drop in their stock price.

Overall, Weave’s Q4 earnings report was quite positive. The company continued to exhibit their strong fundamentals and raised their outlook for the future. And despite all this, their share price plummeted. I believe this dip can offer long-term investors an attractive buying opportunity.

Updated Intrinsic Valuation

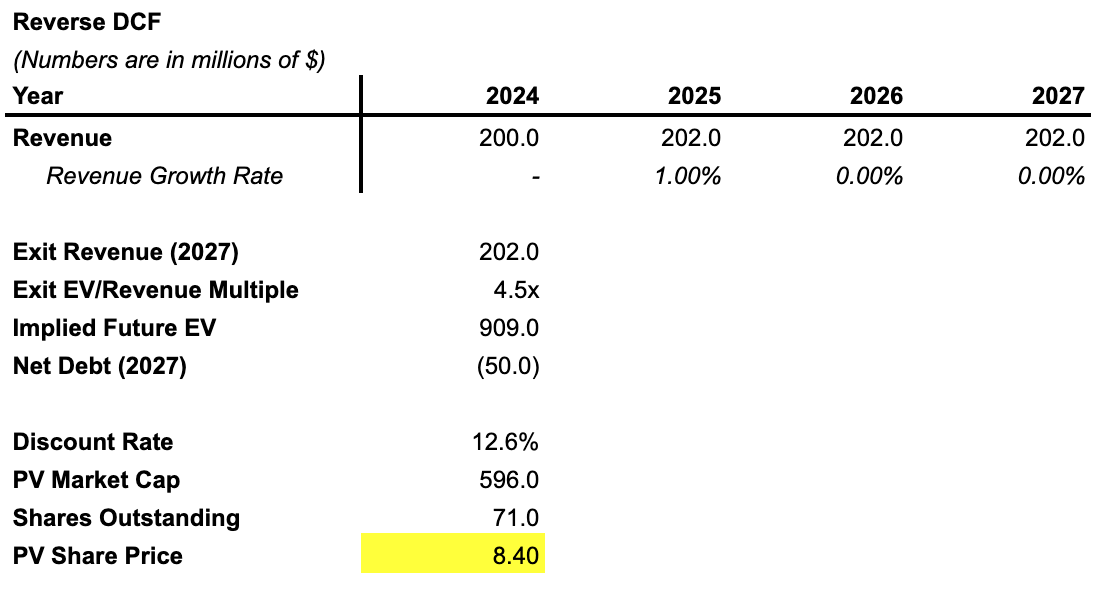

In my prior analysis, I created a simple DCF to estimate Weave’s intrinsic value based on their future revenue. Additionally, I created a reverse DCF to estimate the assumptions the market has priced into their stock. Upon updating the model based on management’s latest guidance, I continue to believe that Weave is significantly undervalued, especially following their post-earnings selloff.

For my valuation, I forecasted Weave’s revenues through 2027 and selected revenue as the primary metric for Weave’s valuation. This aligns with industry standards, as unprofitable software companies are generally valued on an EV/Revenue basis.

For the reverse DCF, I used an EV/Revenue exit multiple of 4.5x, which is in line with where Weave has traded historically. Furthermore, I estimated that they would reach $200 million of revenue in 2024 and that their WACC is approximately 12.6%.

Mountainside Research

Using these assumptions, the market is currently pricing in almost zero revenue growth for Weave through 2027. Considering that Weave is expected to grow at about 17% this year, it seems incredibly unlikely that their revenue growth would immediately come to a halt in the following years.

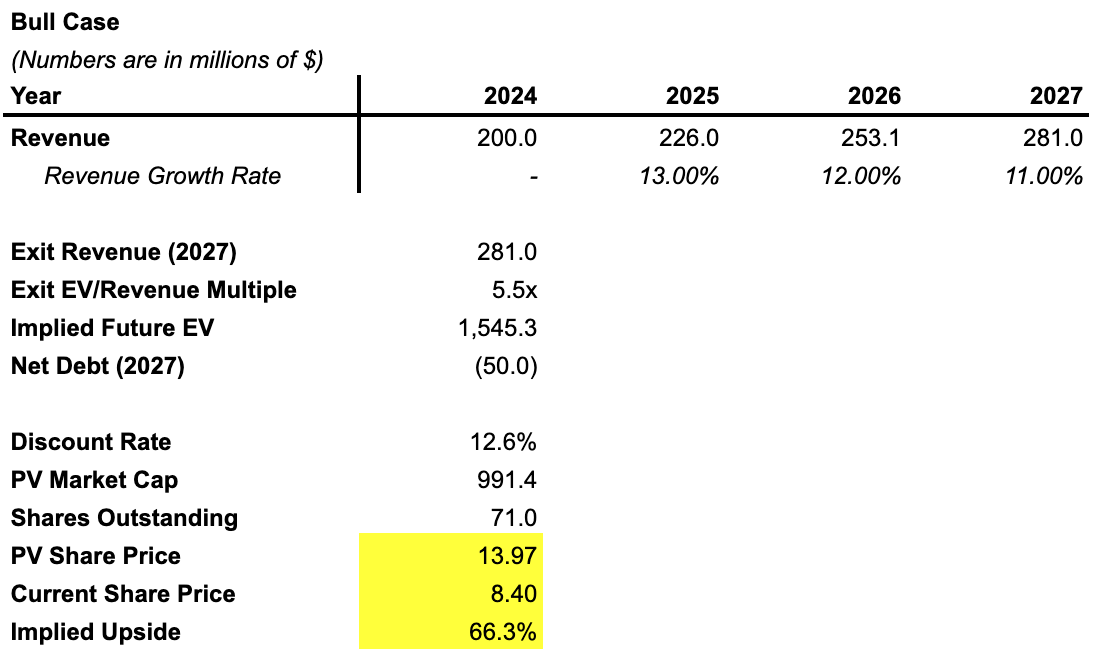

In my bull case DCF, I estimated that Weave could grow revenue by 13%, 12%, and 11% from 2025-2027. Additionally, I assumed an EV/Revenue exit multiple of 5.5x. I justified this multiple expansion to Weave’s increase in size (from revenue of $200 million to $281 million), as well as their transition to profitability in the coming years. Using these conservative assumptions, I estimated an intrinsic value share price of $13.97. This intrinsic value implies an upside of 66.3% on the stock.

Mountainside Research

Even if these assumptions are optimistic, the large delta between the current share price and the intrinsic value share price indicates that there is a large margin of safety for long-term investors. For these reasons, I remain bullish on Weave.

Risks

Churn continues to be a relevant risk for Weave. Although they boast best-in-class levels of retention for SMB software, churn will always be a real risk for any company that has sub-100% levels of net revenue retention. Luckily, churn has been trending in the right direction for Weave. As discussed earlier, their net revenue retention increased this past quarter. Additionally, management noted in their earnings call that gross retention was 92%, the same as the prior quarter. With this in mind, churn doesn’t appear to be a pressing risk for Weave. However, it’s something that investors should continue to keep a close eye on as it can be a leading indicator for their stock’s prospects.

Conclusion

Overall, Weave’s Q1 earnings reaffirmed my belief in the company. Their fundamentals remain strong, their future appears bright, and their valuation is cheap. I believe that the market may have overreacted following their one-time cash flow fluctuation—offering long-term investors an attractive entry point. Furthermore, I wouldn’t be surprised if Weave’s stock sees a healthy jump following their Q2 earnings release when they get the positive benefit of the cash flow fluctuation. For these reasons, I reaffirm my ‘Buy’ rating on Weave for long-term investors.

Q2 2024 Earnings Call Transcript")