AzmanJaka

There is a misconception, I believe, when it comes to generating market beating returns. Many people seem to think you need to buy into risky companies and/or firms that are growing rapidly in order to capture strong upside. But from my experience, some of the most boring, low growth companies offer the greatest potential. And this is because of their quality and the fact that the market underestimates them from time to time. A really good example of this can be seen by looking at perhaps one of the most ‘boring’ businesses on the planet. And that is Waste Management (NYSE:WM).

Odds are, you are familiar with Waste Management. And this is because the company is the largest provider of waste disposal services in North America. Well, back in February of 2023, I wrote a bullish article about the company. At the time, I was reviewing financial results for the final quarter of the 2022 fiscal year. And in that article, I acknowledged that the company was still a quality operator and I said that it was still fundamentally attractive. This led me to rate the business a ‘buy’. But even then, I would not have imagined the kind of upside shareholders have seen. With top line and bottom line results continuing to improve year after year, shares of the business have generated upside for investors of 42.4%. That’s almost double the 23.2% rise seen by the S&P 500 over the same window of time. Even after experiencing that upside, I would argue that the stock offers a little bit of additional upside. And given this, I am reiterating the ‘buy’ rating I assigned it previously.

The picture still looks good

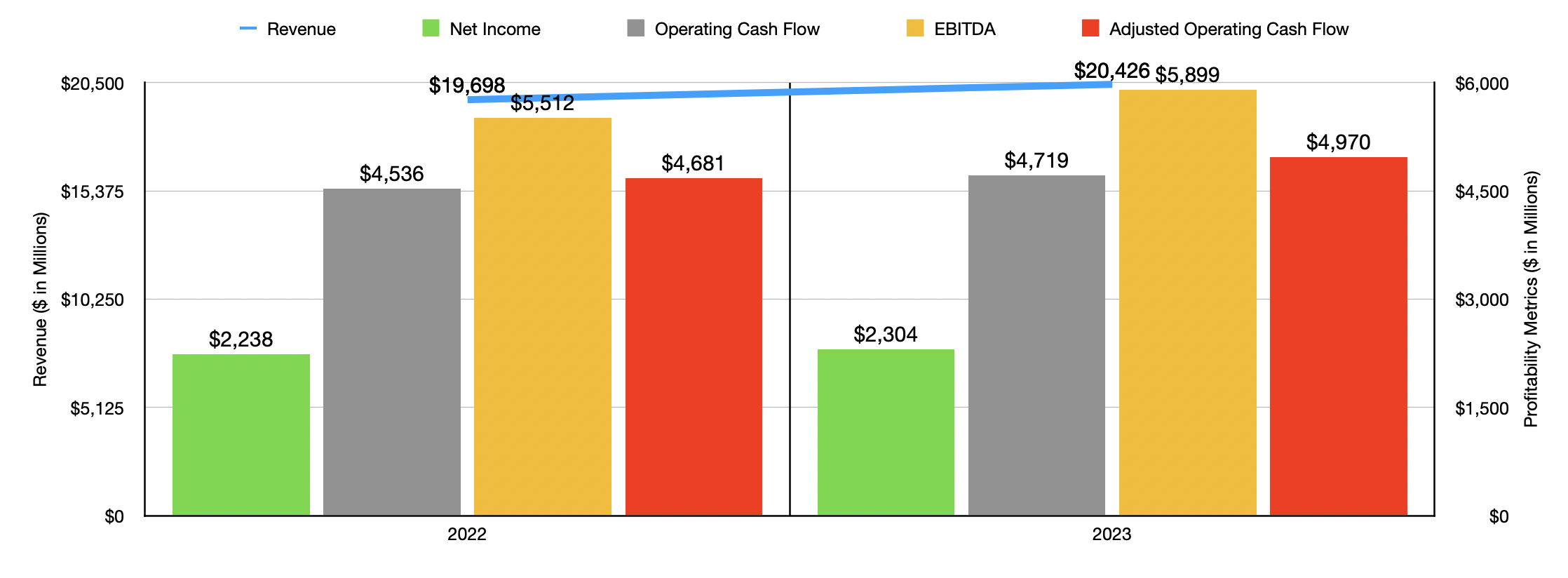

Fundamentally speaking, things are going quite well for Waste Management and its investors. To see what I mean, we need only look at financial results for 2023 relative to 2022. Revenue for that time came in at $20.43 billion. That’s an increase of 3.7% over the $19.70 billion management reported for 2022. There are many working parts for this company. Some of them experienced weakness from 2022 to 2023. But most of them experienced upside. Some of the greatest strength of the business came from its Commercial operations, with revenue spiking 5.1% from $4.86 billion to $5.11 billion. This falls under the collection category of the company and was driven largely by pricing increases. As a whole, the company did experience a rise in volume. But this only pushed sales up by $150 million, or 0.8%, from 2022 to 2023.

Author – SEC EDGAR Data

The rise in revenue allowed net profits to grow by 2.9%. Growth would have been higher had it not been for a corresponding rise in costs. As an example, labor and related benefits increased from 17.5% of sales to 18% because of market wage adjustments. However, higher employee headcount caused by acquisitions, as well as a rise in health and welfare costs and medical care activity all played a role. Maintenance and repair costs grew from 9.3% of sales to 9.7% because of inflationary pressures. And subcontractor costs grew from 10.2% of sales to 10.7%. Just like labor and related benefits, this was driven mostly by wage pressures. Management also booked some other expenses, particularly a $275 million impairment charge that dwarfed the $50 million impairment charge seen one year earlier.

Author – SEC EDGAR Data

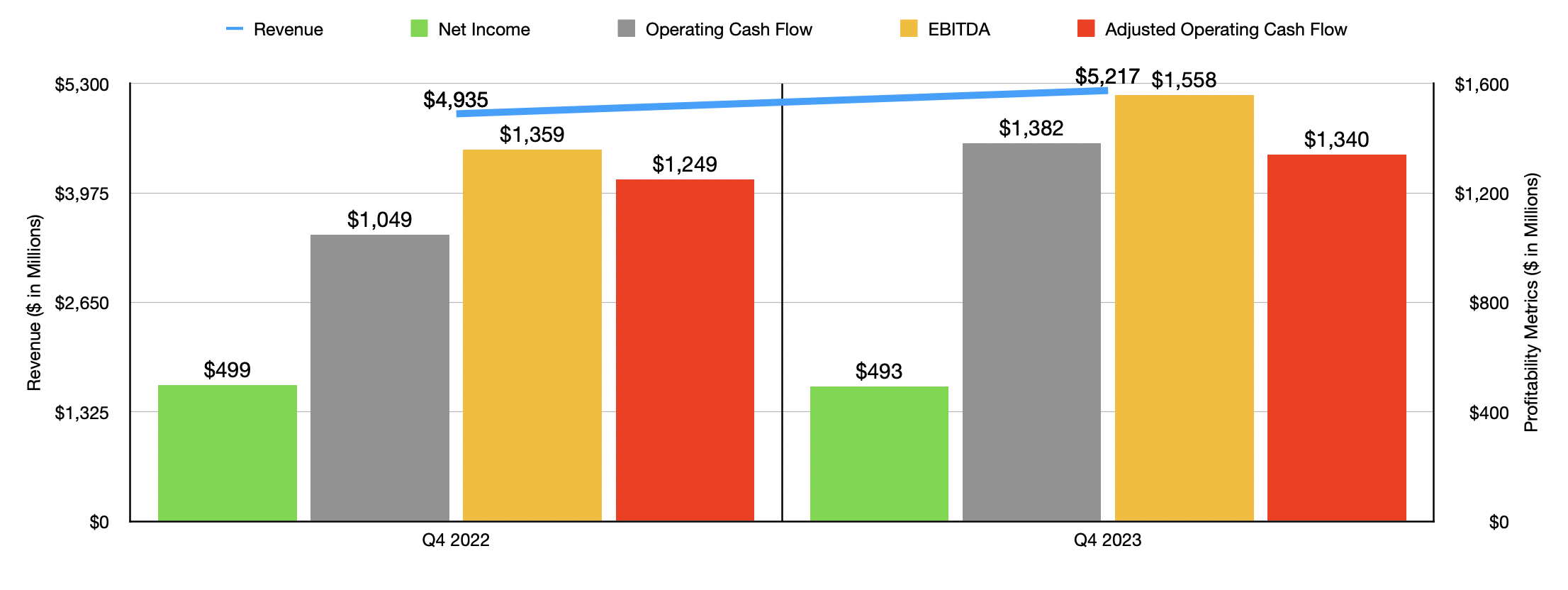

Other profitability metrics also managed to improve year over year. Operating cash flow, as an example, grew from $4.54 billion to $4.72 billion. If we adjust for changes in working capital, the rise was from $4.68 billion to $4.97 billion. Even more impressive was EBITDA. It managed to shoot up by 7% from $5.51 billion to $5.89 billion. In the next chart above, you can see results for the most recent quarter for which data is available. That’s the final quarter of 2023. Just as was the case with 2023 in its entirety, revenue and cash flows increased nicely on a year over year basis. The only weakness was in net profits. But even that was mild, with income ticking down slightly from $499 million to $493 million.

When it comes to the 2024 fiscal year, management has some pretty high hopes. They anticipate revenue climbing by between 6% and 7%. This should be driven by core price increases of between 6% and 6.5%. Also aiding the increase should be a 1% rise in volume associated with the company’s Collection and Disposal activities. Naturally, this is a space that Is asset intensive. The company has a massive fleet of trucks, plus 258 solid waste landfills, five secure hazardous waste landfills, 237 sites that it owns or manages that are centered around remedial activities, 332 transfer stations that consolidate, compact, and transport waste, and a slew of other assets. It would be crazy to think that the company doesn’t need to spend a lot of money to keep all of this operational. That’s why, for 2024, management is forecasting capital expenditures centered around existing operations of between $2.2 billion and $2.3 billion. On top of this, however, the company is going to be spending between $850 million and $900 million on capital expenditures centered around high growth initiatives.

This growth oriented spending is part of the company’s plan to allocate between $2.8 billion and $2.9 billion toward growth investments in areas like recycling and renewable energy between 2022 and 2026. Last year and the year before, the company had already spent, collectively, just under $1.33 billion on these efforts. Its spending includes $350 million that is an increase over its prior plan for new recycling growth projects that are expected to deliver high returns. Of course, management isn’t doing this for any reason other than increasing shareholder value. They believe that, by the end of 2026, around $800 million worth of additional operating EBITDA will be captured from these investments. $510 million of that is expected to come from renewable natural gas projects, while $290 million will come from recycling projects.

This doesn’t mean that the company will not be returning capital to shareholders. The firm should have plenty. In fact, this year, management is forecasting EBITDA of between $6.275 billion and $6.425 billion. Operating cash flow should be between $4.95 billion and $5.25 billion. And if profits rise at the same rate, we are looking at net income of about $2.36 billion. This should allow the business to quickly accomplish the $1.5 billion renewed share buyback program that management announced in December of last year. And on top of this, the firm increased its annual dividend by 7.1%, marking the 21st year in a row in which the dividend was raised.

Author – SEC EDGAR Data

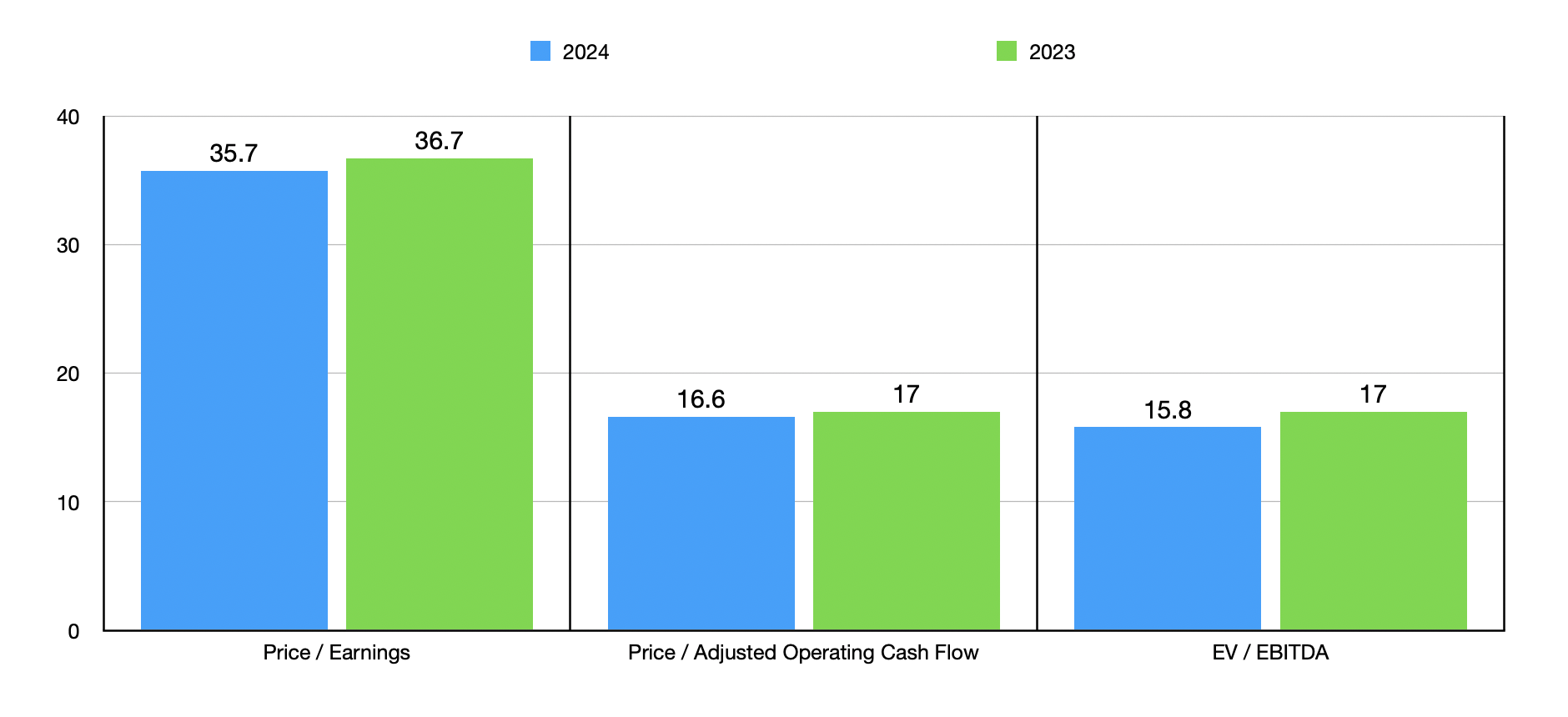

Such a high quality company cannot be expected to be cheap. In the chart above, you can see how shares are priced on an absolute basis using historical results from 2023 and estimates for 2024. The stock looks particularly pricey relative to earnings. But from a cash flow perspective, the picture isn’t that bad. In the table below, I compared the enterprise to three similar firms. When it came to the price to earnings approach and the price to operating cash flow approach, I found that one of the companies was cheaper than it. This number increases to two of them when using the EV to EBITDA approach.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Waste Management | 36.7 | 17.0 | 17.0 |

| Republic Services (RSG) | 34.1 | 16.3 | 16.6 |

| Waste Connections (WCN) | 57.2 | 20.5 | 22.3 |

| GFL Environmental (GFL) | N/A | 17.8 | 11.8 |

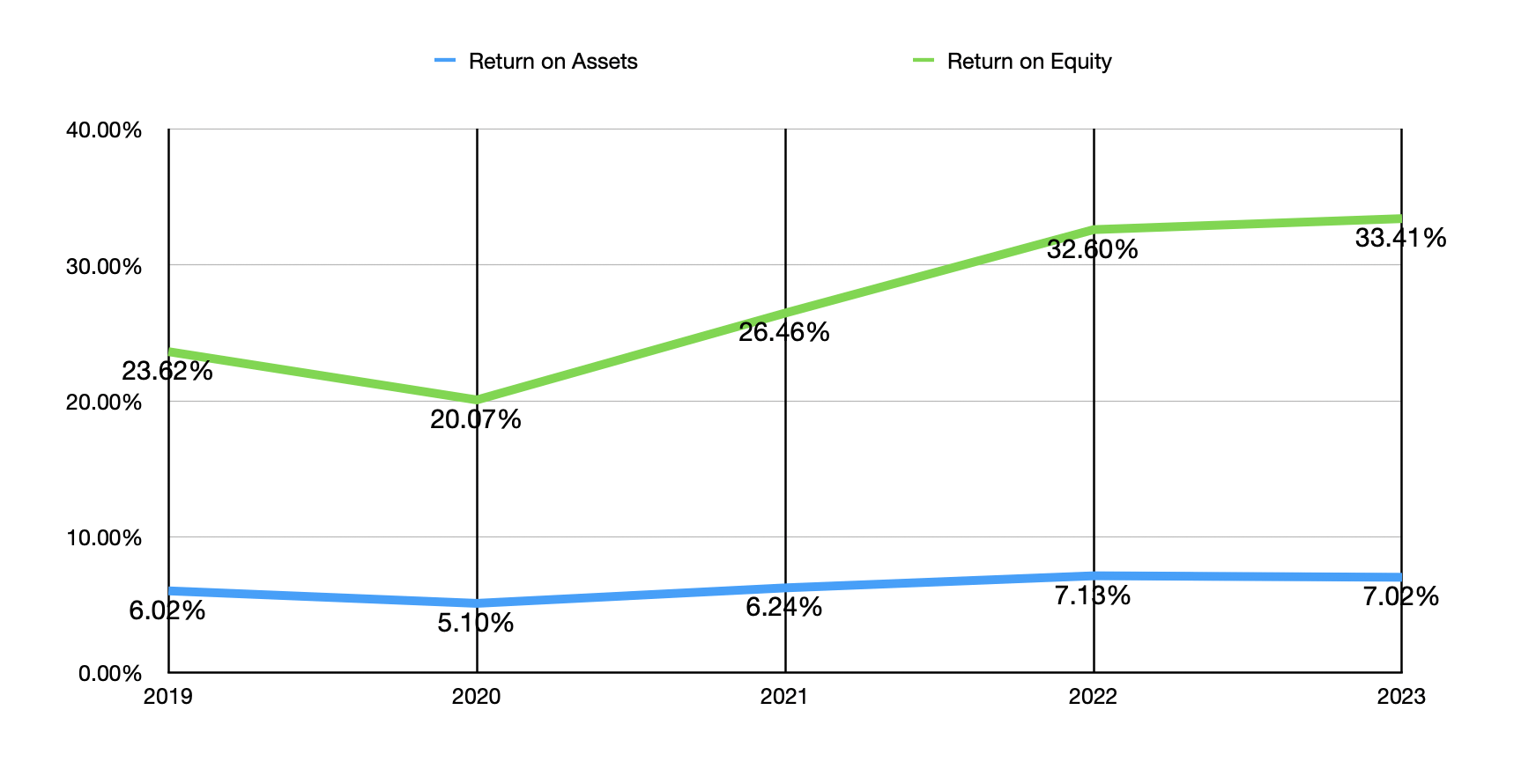

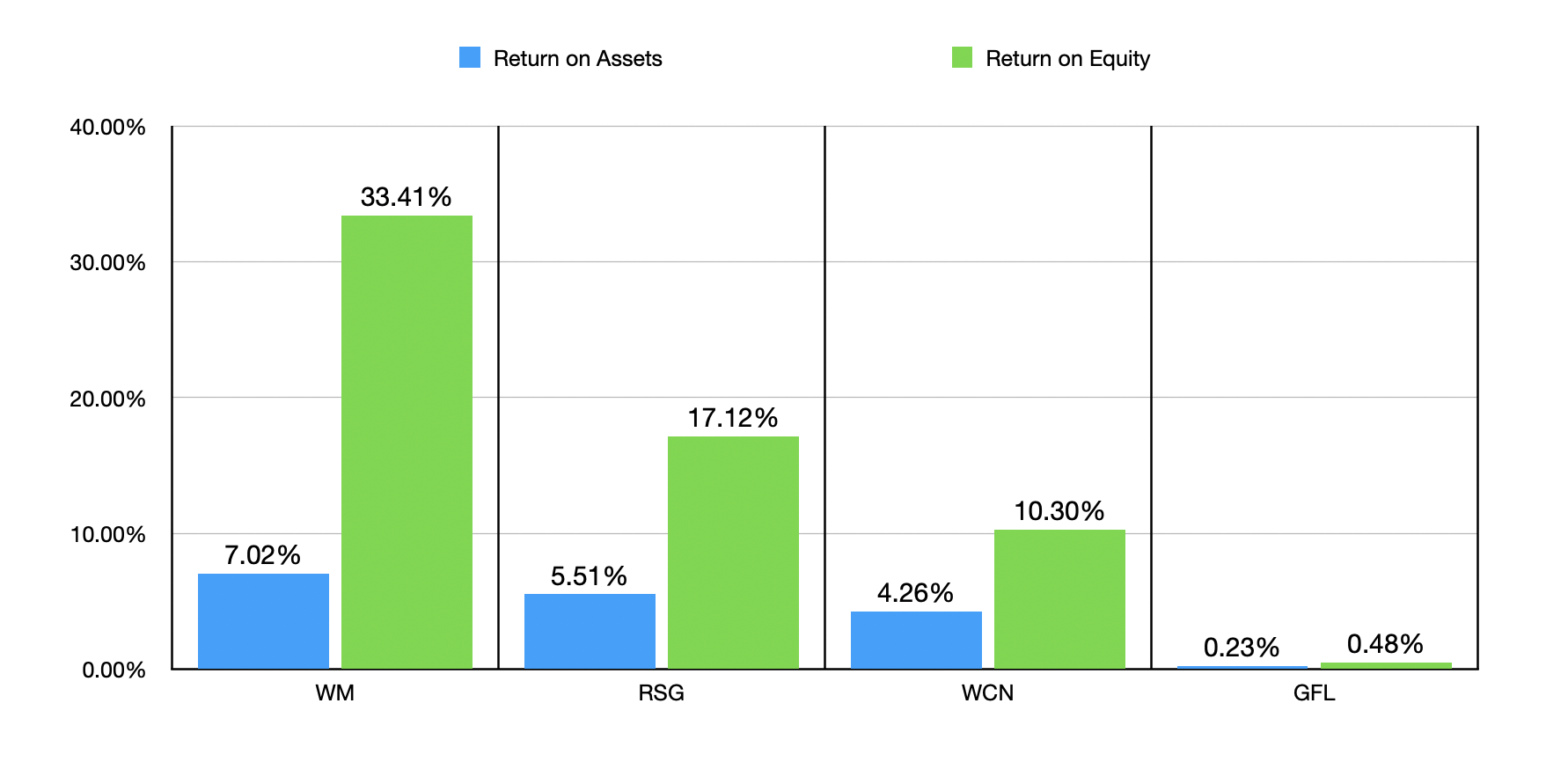

Pricing is important. But we should also be looking at the overall quality of the institution. The first way to do this is to look at the health of the business from a return on assets perspective. In the first chart below, you can see both return on assets and return on equity for the business over the last five fiscal years. Although return on assets did dip slightly from 2022 to 2023, the overall trend there is positive. Meanwhile, return on equity looks particularly robust and shows no signs of abating. In the subsequent chart below, you can then see how the stock looks relative to the same three firms I compared it to previously. This includes both a return on assets approach and a return on equity approach. In both cases, Waste Management dwarfs the competition.

Author – SEC EDGAR Data Author – SEC EDGAR Data

Takeaway

For people looking for a very cheap company, Waste Management should not even be in the running. But value investing is not always about picking up the cheapest firms. Sometimes, it’s about buying the companies that are high quality and that are trading at a decent price. That’s the way Warren Buffett has evolved as an investor in recent decades. It might mean that your returns are not as robust as you would like. But as the share price of Waste Management has demonstrated over the past year or so, that’s not always the case either. Clearly, this is a high-quality business that is creating significant value for its investors. Because of this, I believe that investors would be wise to consider this a ‘buy’ candidate.

Q2 2024 Earnings Call Transcript")