kokouu/E+ via Getty Images

The Announcement

Vroom (NASDAQ:VRM) announced yesterday that they will be winding down their used vehicle dealership business. They said they will be halting both buying and selling on Vroom.com and looking to sell their current inventory through wholesale channels. It seems that the reason for this decision was that they no longer could access financing needed to expand and that expansion was necessary to ever reach profitability.

I applaud management for realizing there was no way to get their current operations to profitability and simplifying the business before they get into a bigger hole. Their hand may have been forced, since they obviously were attempting to get further financing and keep scaling up, but couldn’t find enough financing to get it done. In my eyes though, this is the smart move. They became a public company during the pandemic when there was tons of money available for IPOs and they were trying to scale up with used car prices that were sky-rocketing from the pandemic. Reality hit shortly after though- used car prices dropped and getting new inventory stayed expensive since all dealerships were looking for more. There just wasn’t much margin left for a low barrier to enter the market.

Furthermore, I think the used car buying market is just too fragmented. Aside from Vroom and Carvana (CVNA), there are CarMax (KMX), independent old-school dealerships, and many others. There are a lot of competitors, with few offering any real value over the others. This drives it to be a low-margin, low-barrier-to-entry business. With all of the headaches of shipping cars and titles and differing state and federal regulations, the costs mount quickly. In my eyes, it would take a much, much larger scale to operate an ecommerce car business profitably.

What’s Left?

For those who don’t follow Vroom very closely, you might ask, “Isn’t buying and selling cars their entire business?” The short answer is no. While Vroom gets the majority of its revenues from their ecommerce operations, it also owns United Auto Credit Corporation and CarStory.

United Auto Credit Corporation (UACC) is their financing division in a sense. While Vroom will no longer have their own cars to offer captive financing on, they have third-party customers that use UACC and they can continue to finance vehicles that way.

While auto-financing is a pretty straightforward tack-on business for Vroom, I’m a little less sure how they make money from CarStory. In the Vroom wind-down announcement link above, they state that CarStory is, “a leader in AI-powered analytics and digital services for automotive retail.” The name CarStory, to me, also signifies that they keep a history of cars, with accidents and servicing records, similar to CarFax.

However, when I go to Carstory.com, it seems to just be a site that allows you to search for vehicles to buy by location/price/make/model/type/etc. All cars I have tried clicking on, just link to CarFax, so I guess CarStory doesn’t provide their own history. In summary, CarStory to me just seems like a database of used vehicles that uses CarFax to show a history. So it seems that CarStory is mostly a database of used vehicles (owned by many different entities, not just Vroom’s used vehicles) and maybe they leverage the large amounts of data to give insights on pricing, sale velocity, etc.

Valuation

So now with the background knowledge of what Vroom is doing and what pieces will be left, valuing the remaining company basically comes down to how much of their current tangible book value we think they will be able to hold onto while they wind down, and how much value can be attributed to their remaining pieces (UACC and CarStory).

Today, after the ~40% sell-off following the announcement, their market cap is around $42M and their tangible book value was last listed on their Q3 2023 earnings as $119.6M. Put another way, their current share price as of writing this is $0.30 and their tangible book value per share is $0.86. I like to use tangible book value because it takes out any goodwill and other intangibles that get included in classic book value. In these sorts of wind-down or sell-off asset scenarios, there is usually very little or no value in intangibles. These values show that as of the end of Q3 2023, there would be almost triple the value in the assets (after subtracting debt) than the current market cap.

However, assuming that Vroom didn’t suddenly become profitable, we know that they will have lost more money in Q4, as well as continue to lose money during the wind-down period. They lost between $0.40 – $0.50 of tangible book value each of the last few quarters, so there’s a lot of evidence that the tangible book value at the end of Q4 will be pretty close to their current market cap.

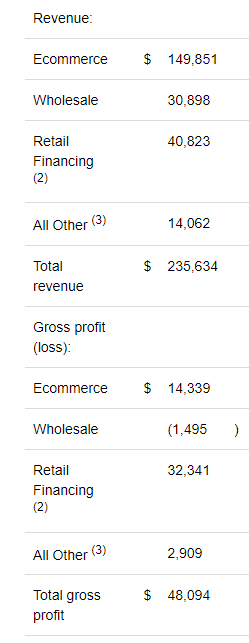

I also want to point out that they announced they will be selling their vehicles wholesale, which usually loses money, even at the gross profit level (excluding operational costs). Basically, I take this to mean that while selling cars through ecommerce is more profitable on a unit level, they are choosing to stop selling that way immediately because it still costs so much more to run from an operations perspective. Put another way, they think they will lose less money by selling in bulk wholesale, even while selling individual vehicles at a loss because they can wind down operations faster and lay off more workforce immediately. Here’s a breakdown of Vroom’s latest quarter for revenues and gross profits:

Q3 2023 Earnings Results (Q3 2023 Earnings Results)

With some quick calculations, we can see that the gross profit margin on Ecommerce was ~10% in Q3, Wholesale was negative, Retail Financing was ~80%, and All Other (which includes CarStory) was ~20%. One big positive from this info is that Retail Financing is by far their most profitable segment on a gross profit basis (I didn’t see any break out of administrative costs by segment) and they are of course keeping that segment. One big negative is that we see just how bad of a deal they get when they have to sell cars through their Wholesale segment. Since they said they will be selling all remaining inventory this way, I have to assume they will be taking a loss on those assets and not getting the full value out of them that is currently listed on the balance sheet.

All of the above bodes even worse for their tangible book value as it likely means they won’t even get as much out of their assets as is listed on their balance sheet. Between their assets likely needing a haircut, the associated costs of laying off a workforce (severance packages and such), and the fact that they’ll still have to keep enough personnel on to run their other businesses and everything associated with being a public company, I expect their tangible book value to actually be negative after all that is taken into account.

But now back to the valuation of the remaining pieces. Vroom announced they were buying UACC for $300M back toward the end of 2021 and finished the acquisition in early 2022. I expect there is still value left in UACC, but I also doubt it is worth as much as they paid for it. Since public companies almost always pay a premium when buying another business, I would think they would only be able to sell UACC for around half, though I admit that’s a total guess. Perhaps it’s worth even less or perhaps they expanded the business and it’s now worth more than they bought it for.

Vroom also bought CarStory for $120M back at the end of 2020. For the same reasons, I assume it is worth less than they paid for it, but it’s a big question mark as well. The fact that they claim they have an AI offering probably helps their valuation right now, but to me, it’s still basically just a car sale database. In total, I’m going to be assigning around $200M for UACC and CarStory in total.

After subtracting out the negative tangible book value I expect from winding down operations and adding this assigned value very roughly estimated at $200M for UACC and CarStory, that could leave as much as $150-$200M in tangible value left. That may seem like a lot compared to their current market cap of $42M, but since they don’t plan on selling off UACC or CarStory as part of this wind-down, I’d like to see the operating margins of what remains of the company before deciding if it’s a stock worth holding. As with any holding, it’s only worth what you can sell it for and since Vroom doesn’t plan on selling off UACC or CarStory, it doesn’t really matter what their value is until they do or until we can see how much profit they can generate alone.

Conclusion

I went into this article to see if the sell-off was too large and if there was any meat left on the bone, so to speak. However, it seems to me that there is likely a negative value left in the remaining car assets after accounting for the debt left on the balance sheet and the continued costs of winding down operations.

There is a decent chance that UACC and CarStory can end up being worth more than the deficit I expect they’ll be in after selling off their car inventory assets. We know that UACC is their most profitable segment on a gross profit basis, but that is usually true with financing. While financing is very profitable and there’s a reason so many banks exist, it takes carrying a lot of loans on the balance sheet and is riskier from a credit perspective. It also remains to be seen how many general and administrative costs they’ll have after winding down the ecommerce segment.

Even if there is some value left in the remaining businesses after winding down their car dealership business and accounting for debt left, it is a risk with somewhat limited upside and a lot of unknowns. Following this analysis, I think there is a decent chance that UACC and CarStory will be worth more than what they’ll lose in winding down, but I personally do not plan on doing any speculative buying on the remaining pieces, until I get more information on their operational efficiencies further into the process.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")