Dilok Klaisataporn

Introduction

It’s been over three months since I’ve written about a gold mining company and today, I want to talk about Vox Royalty (NASDAQ:VOXR) (TSX:VOXR:CA). It’s a small royalty and streaming firm focused on Australia that has several producing assets already. With gold prices stabilizing just above $2,000 per ounce, I think there is a decent buying opportunity here and my rating on the stock is a speculative buy. Let’s review.

Overview of the business and financials

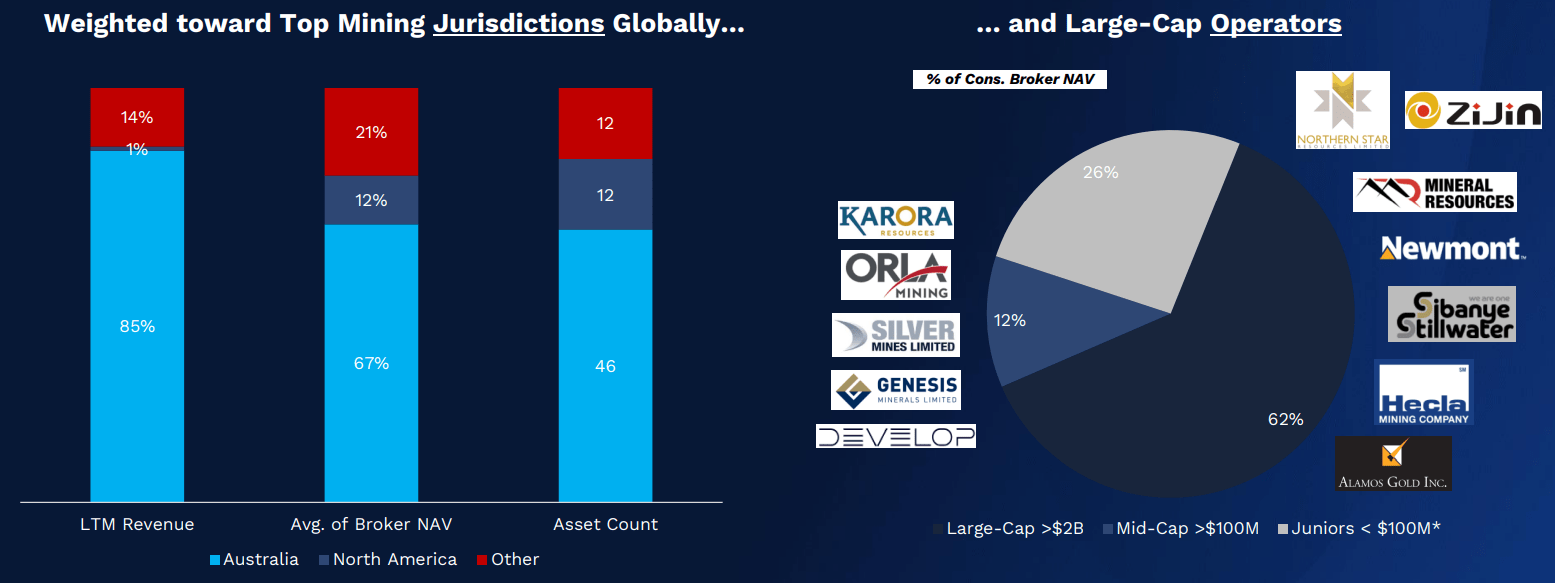

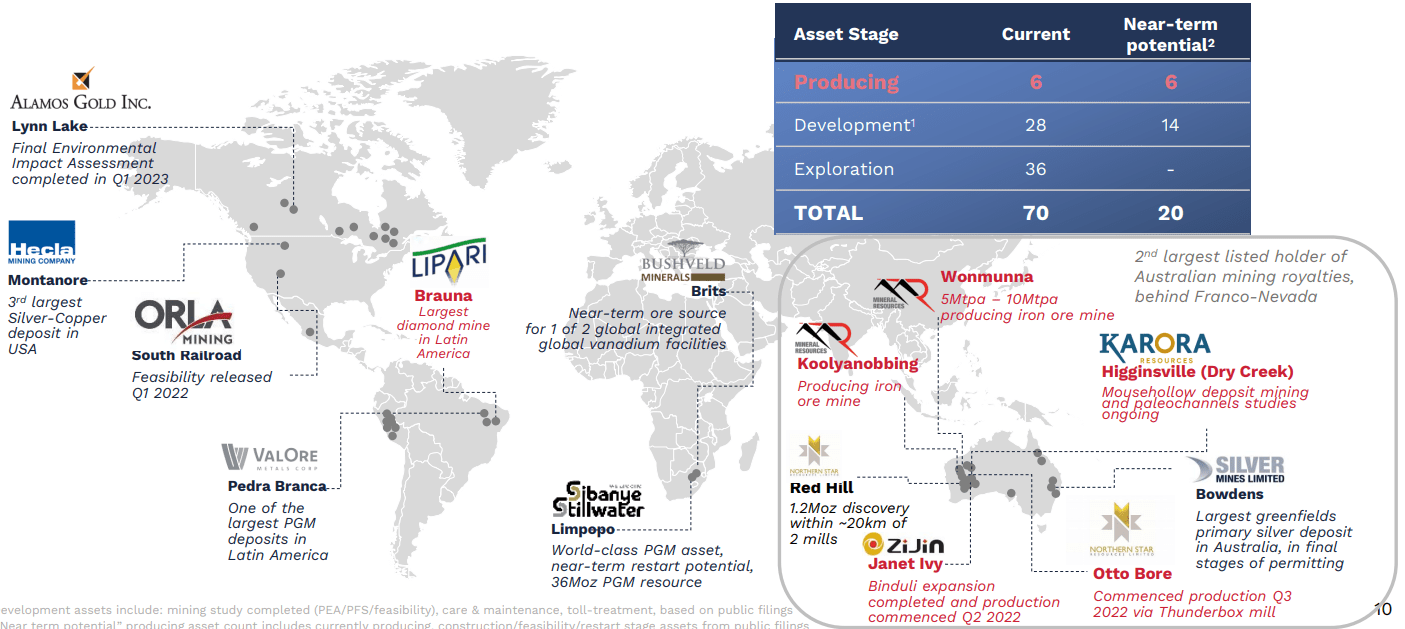

What I like about royalty and streaming companies in the mining industry is that they provide an exposure to the underlying commodities and CAPEX needs are low. In this regard, they are similar to tailings retreatment firms. They also offer exploration and mine expansion upside at no additional cost and there is no exposure to rising variable costs due to inflation. Small royalty and streaming companies in the gold space that have producing assets and positive cash flow from operations are rare. Vox Royalty was established in 2014 and it has built a portfolio of more than 60 royalties and streams across 8 jurisdictions. Most of them are located in Australia and are operated by major global gold miners such as Newmont (NEM) (NGT:CA), Zijin Mining (OTCPK:ZIJMF) (OTCPK:ZIJMY), and Alamos Gold (AGI).

Vox Royalty Vox Royalty

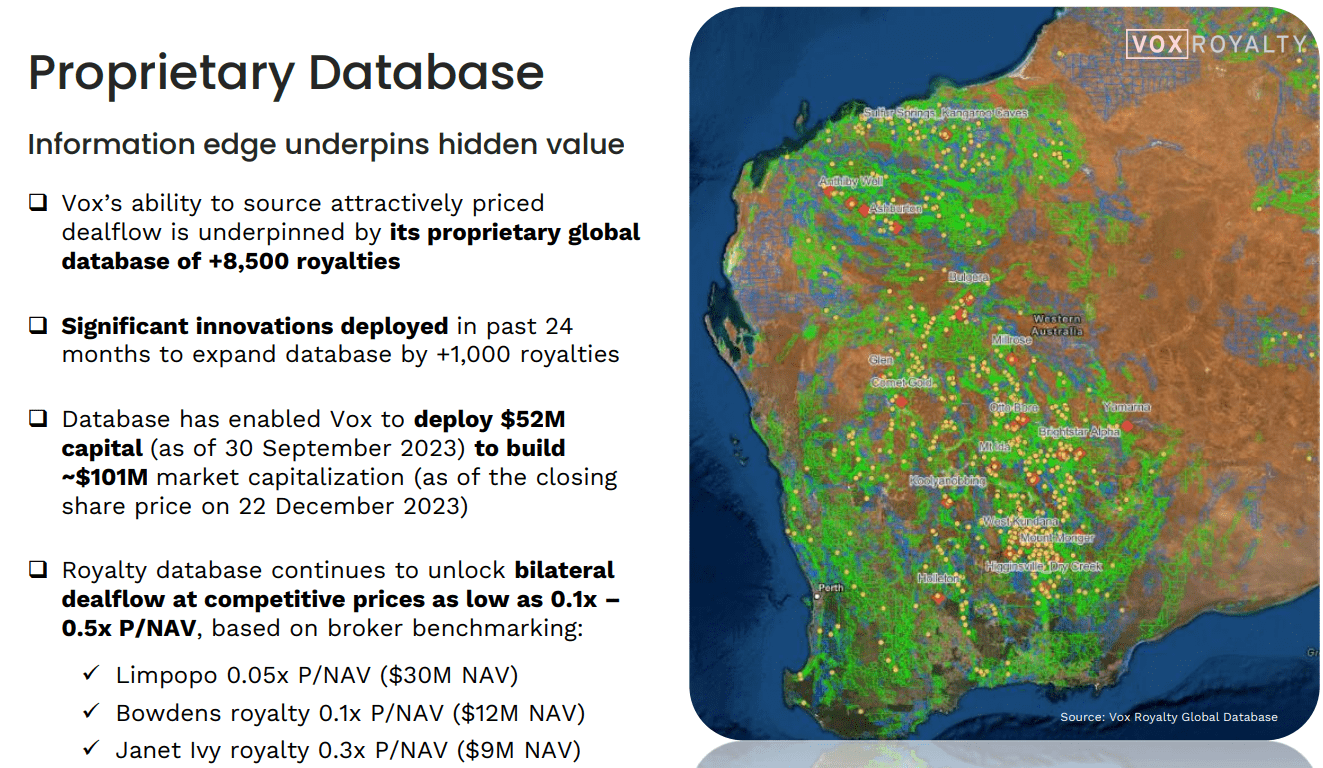

Over 50 of the royalties and streams have been acquired since 2020 and what sets the company apart from its competitors is a proprietary database of over 8,000 global royalties. This should give it a small edge when selecting royalties to acquire. Vox Royalty also has a technical team made up of mining engineers and geologists that evaluates the merits of each asset it acquires. About 50% of the company is owned by management and family offices (see slide 3 here).

Vox Royalty

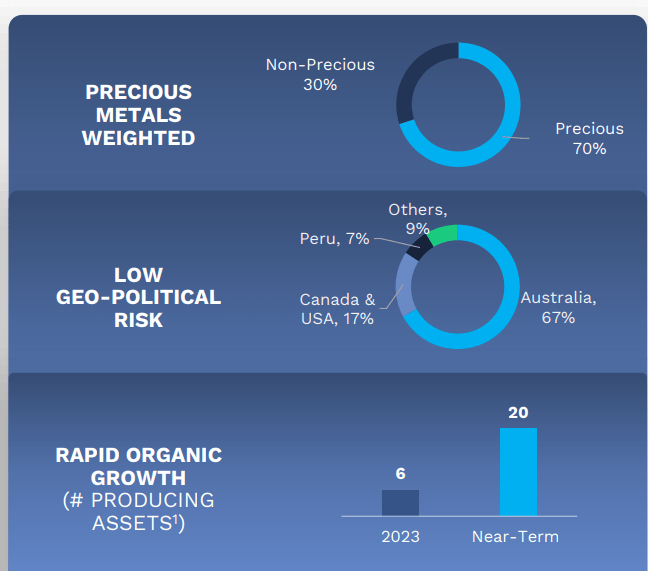

Looking deeper into the royalty portfolio of the Vox Royalty, we can see that all but one of the producing assets are location in Western Australia. It’s the second largest listed owner of Australian mining royalties, behind only Franco-Nevada (FNV) (FNV:CA). Vox Royalty currently has royalties on projects producing gold, iron ore, and diamonds.

Vox Royalty

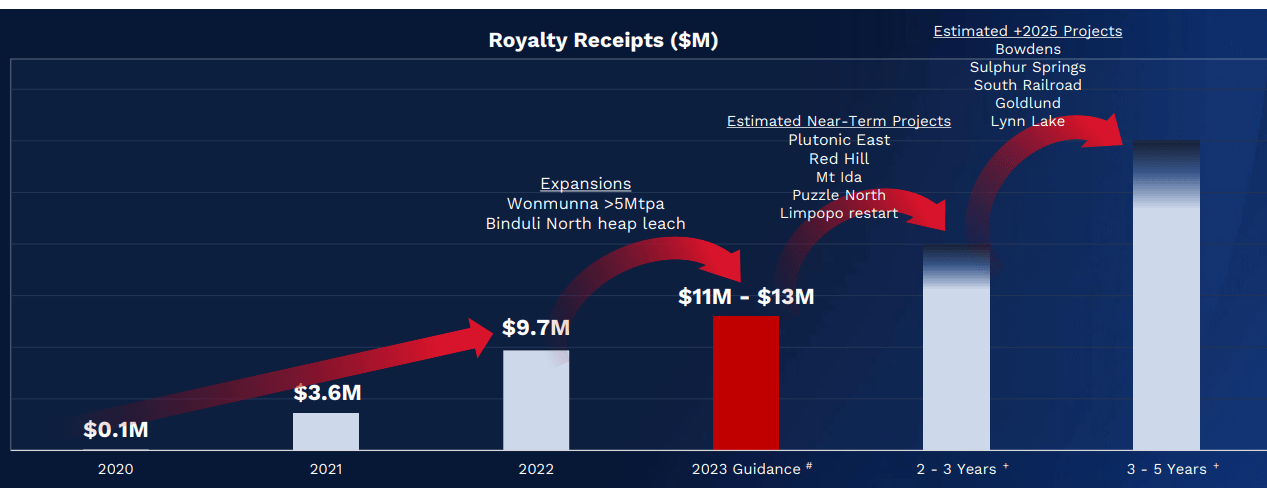

The company focuses on the purchase of royalties on projects that are set to begin production within 3 to 36 months. With such a strategy, it’s no surprise that the revenues of Vox Royalty have been growing exponentially over the past few years – from just $0.1 million in 2020 to $9.7 million in 2022. In addition, the company boosted its quarterly dividend by 10% to $0.011 per share in May 2023.

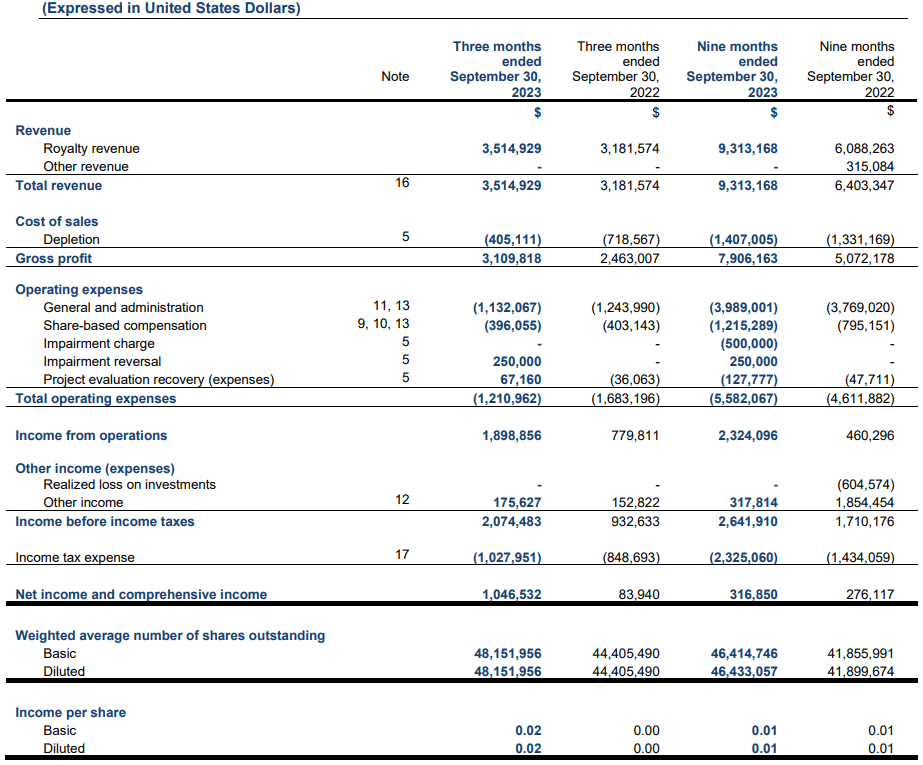

Looking at the latest available financial report of Vox Royalty, we can see that royalty revenue grew by 10.5% year on year to $3.51 million in Q3 2023. In my view, general and administration expenses are somewhat low for a mining company of this caliber and adjusted operating income came in at $1.58 million for the quarter. For example, a gold mining company that I’m following named Collective Mining (OTCQX:CNLMF) (CNL:CA) has a market capitalization of $187.6 million as of the time of writing and its Q3 2023 general and administration expenses were $1.27 million (see page 2 here).

Vox Royalty

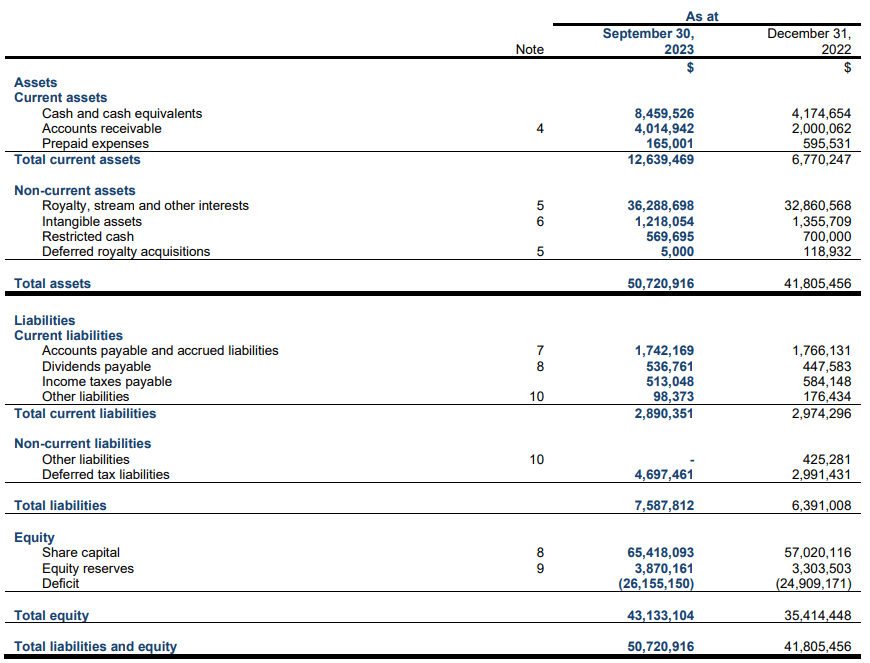

The cash flows from operating activities of Vox Royalty came in at $1.36 million for Q3 and $2.93 million for the first nine months of the year (see page 4 here) and I think the balance sheet looked strong at the end of September. Cash and cash equivalents stood at $8.46 million, which should enable the company to acquire several more royalties before tapping into equity markets. Investments in the acquisition of royalties were $4.49 million for the first nine months of 2023 and Vox Royalty has no debts.

Vox Royalty

Looking at what to expect for the future, I think revenues for 2024 could surpass $15 million thanks to several new producing properties coming online. The guidance for 2023 included royalty receipts of $11 million to $13 million and I think it looked easily achievable. Vox Royalty should release its financial results for the year around the middle of March.

Vox Royalty

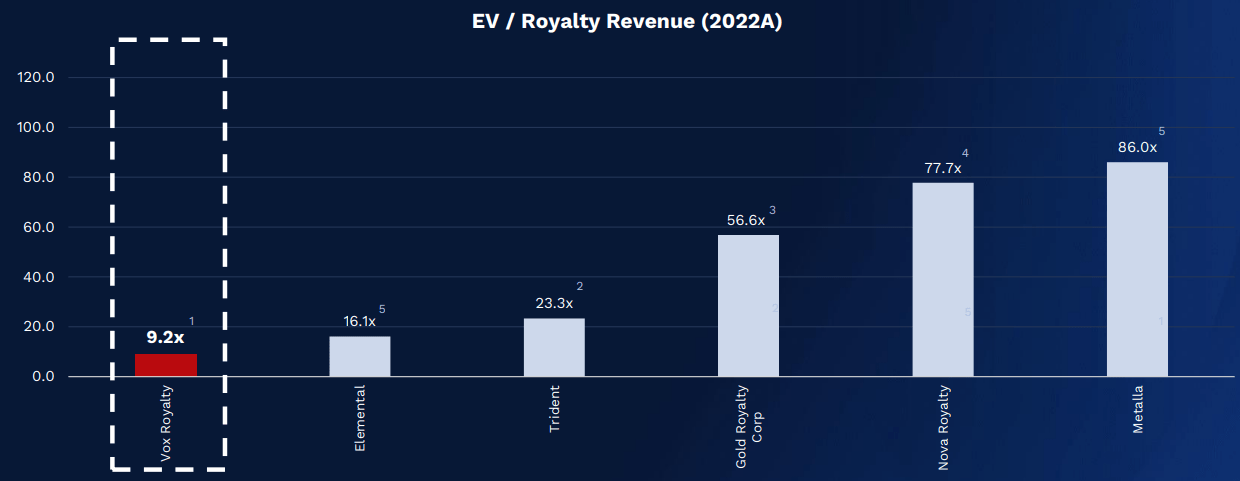

Overall, I think that Vox Royalty has a disciplined capital deployment strategy that is yielding compelling results so far thanks to economies of scale and strict cost control and I’m optimistic that both revenues and operating margins will continue to expand at a rapid pace over the coming years. The balance sheet is solid, and I think there is a lot of room for growth in the quarterly dividend payments if the company continues to execute its strategy well. At the moment, the annualized dividend yield is 2.18% and Vox Royalty has an enterprise value of $92.9 million. In my view, it looks significantly undervalued compared to other small mining royalty companies when measured through EV/royalty revenue and I wouldn’t be surprised if the share price doubles by the end of 2024.

Vox Royalty

That being said, there are several major downside risks here. First, gold prices are difficult to predict and a decline over the coming months could result in a significant decrease in revenues as well as the delay of several projects on which Vox Royalty has royalties. Second, the company is also vulnerable to a slowdown in the global economy, particularly in China, as it holds royalties on two producing iron ore mines. Third, it’s possible that general and administration expenses will start to grow in the future or that Vox Royalty will find it more challenging to grow its royalty revenue at a high pace over the coming years if investment opportunities dry up.

Investor takeaway

Vox Royalty is a rapidly growing mining royalty company with a diversified portfolio of assets in safe jurisdictions like Australia, Canada, and the USA. I think its proprietary database provides it with an edge and its valuation seems low compared to competitors. In my view, revenues are likely to surpass $15 million in 2024 and operating income could increase significantly thanks to economies of scale. In addition, the balance sheet is strong and the stock dilution risk in the short term is low. Yet, it could be best for risk-averse investors to avoid Vox Royalty stock as major slumps in gold or iron ore prices are likely to severely impact revenues and margins.

Q2 2024 Earnings Call Transcript")