Marcus Lindstrom

On March 28th, 2023, I issued a detailed article elaborating on the various aspects of Vonovia SE (OTCPK:VONOY) (OTCPK:VNNVF) that, in my opinion, warranted a clear sell.

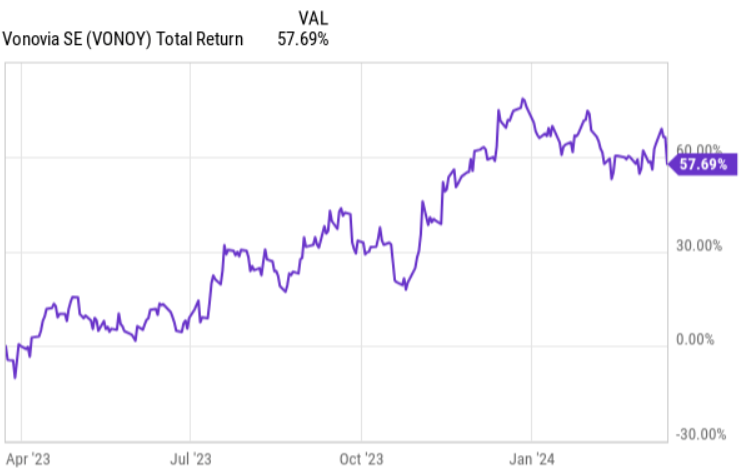

Since then, the performance has been like this:

YCharts

Just recently Vonovia published its Q4 earnings report and annual aggregate figures for the whole 2023. In the day of earnings release, the Stock is down by ~7%, but obviously this does not change the overall result.

I will now provide a quick synthesis of my core thesis, explain why Vonovia has went ballistic since March, 2023 and give you a color on what I think of Vonovia’s financial performance going forward.

Synthesis of my sell thesis

While more details can be extracted from my previous articles on the Company, let’s still go through the key drivers (on a high-level) that formed my sell thesis.

- Yield compression. Before the ECB started to hike the interest rates in a coordinated fashion with the FED, Vonovia’s ERPA net yield stood at less than 3%, which at that time was around 150 basis points above the cost of debt. The only way how Vonovia can get the net yield higher is through organic growth, which is capped by the German law. In other words, the process of cost of financing converging to market level interest rates and thus surpassing the ERPA net yield before the ERPA component reaches above EURIBOR level was one of my biggest concerns.

- Aggressive fair value assumptions. As of March, 2023, Vonovia had made minimal fair value corrections despite the cost of financing going from 0% to ~ 5%. So, in my opinion, it was inevitable that the Management will start reflecting more “market aligned” valuations in the Company’s books as Vonovia is subject to IFRS accounting rules that require carrying assets on a fair value basis. The thesis was that tangible write-downs would introduce an additional pressure on the covenants and leverage metrics, thus weakening Vonovia’s credit profile even further.

- Unfavorable repricing of debt. When issuing the sell thesis, Vonovia’s average cost of debt stood at ~ 1.5% and at the same time there were many debt maturities remaining in 2023 and 2024. Against the backdrop of spiking cost of financing, Vonovia’s insufficient internal cash generation to organically pay down the debt, and the massive indebtedness (net debt to EBITDA of 16x) it was clear that sooner or later these borrowing proceeds would be reset to weigh more higher interest rates.

- Other. Then besides the aforementioned items, Vonovia started to already experience notable struggles in the non-core segments, which imposed some downward pressure on the FFO generation, when the Management was in dire need to shield it as much as possible. Plus, the underlying details of Sudewo portfolio were indicating that Vonovia is taking rather exotic and aggressive measures just to capture any extra capital that could be used to handle near-term maturities. For the long-term shareholders these were not the right signals.

On top of all this, it was still unclear how far the interest rate would go and for how long they would remain elevated. So, when circulating this short idea, it was made clear that if the interest rates plunge back into an accommodative territory, Vonovia would skyrocket.

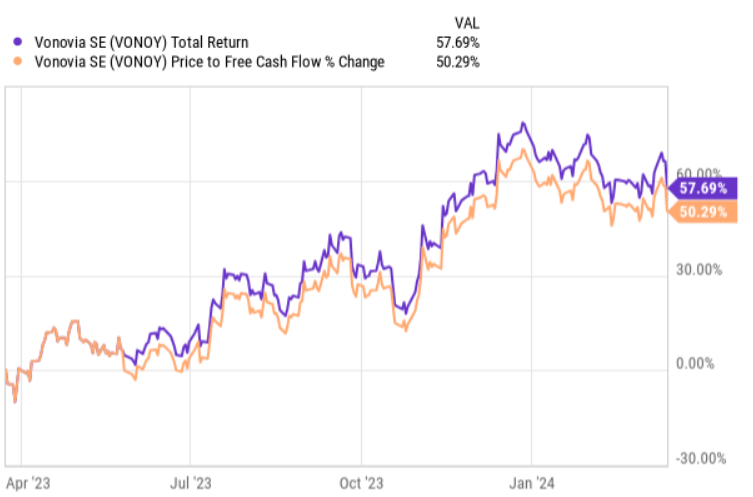

Reasons why Vonovia has performed so well

The simple answer is multiple expansion.

YCharts

Almost the entire amount of gains could be linked to an increase in Vonovia’s valuation multiples. Moreover, if we adjust for the negative performance at the FFO and portfolio valuation levels, the gain from the multiple expansion has been so strong that is has not only sent the Stock price higher by ~50%, but also it has compensated the drop in earnings.

Here is how the actual performance of Vonovia in 2023 looks like (a non-exhaustive list of key metrics based on a y-o-y comparison):

- Group FFO is down by 9.3%.

- Interest expense is higher by 25% despite the fact that the embedded cost of financing still sits at considerably depressed level of ~1.7%.

- Due to partial JV and minority holding sales, the actual FFO adjusted for non-controlling interest is even lower.

- The fair value corrections have finally started to occur with a total gross fair value adjustment of ~21% since the peak valuations in mid-2022.

- Even after the fair value adjustments and strong rental growth, the portfolio net yield still sits at unsustainable 3.3% level.

- Despite the massive divestitures, Vonovia has roughly EUR 10 billion to handle, where organically retiring these debt maturities is clearly not an option given the remaining cash flows after dividends.

- After all of the successful and sizeable divestitures during 2023, the net debt to EBITDA metrics has decreased only by 0.4x (from 15.7x as of year-end 2022 to 15.3x at year-end 2023). Namely, leverage remains elevated.

I could go on and on with this list, but more important question here is what has caused Vonovia’s multiples to expand. Clearly, it is not the fundamentals.

There are three key drivers, which in my view explain the lion’s share of the performance.

First, the interest rates have reached a ceiling and the market has started to calibrate decreasing EURIBOR to relatively accommodative levels. For Vonovia this is massive considering not only the direct implications (e.g., lower cost of financing from incremental debt rollovers) but also the indirect ones such as more fluid M&A and debt market as the investors and lenders enjoy increased visibility for the deal pricing. Improving M&A and financing conditions are vital for Vonovia to continue executing on its divestiture strategy that is the only realistic avenue for sourcing capital to keep the refinancing in check. The more divestitures, the higher portions of maturing borrowings could be repaid, which in turn helps keep down the growing interest expense component.

Second, Vonovia has made solid job on the divestiture front. While I was explicit on the unfavorable terms and conditions how most of these financing have been attracted, the real thing what matters is that the Company has successfully obtained fresh capital to purchase back at a discount most of the near-term bonds. During 2023, Vonovia sourced EUR 4 billion from divestitures, which also shielded the existing covenants from a continued deterioration.

Third, at the time of issuance of my sell thesis, Vonovia traded at significantly depressed valuations – P/FCF of around 7.5x, which is more than 3x below the peak in 2021. Whenever a company trades at so low and historically cheap multiples, each assumption / result change in the positive direction is per definition set to provide a huge boost to the share price.

Well, in this case we had a low multiple and two critical items becoming clearer (i.e., interest rate path and Vonovia’s ability to divest) that together warranted a strong rebound.

My stance on Vonovia and the bottom line

In a nutshell, my bearish stance on Vonovia has not changed. I still think that Vonovia is a bad investment for long-term investors. What has changed though is my recommendation on Vonovia – from sell to hold.

Why it is not a sell anymore?

Fundamentally I think that Vonovia will continue to register worsening performance over the foreseeable future. Namely, I am bearish on Vonovia’s fundamentals (see comments below).

Yet, if we sum the following items together, I think that there is still a risk (or potential) out there that short sellers would get burned just as I did:

- EURIBOR has peaked and set to decline already this year. Once the actual decisions are made at the ECB, it is highly likely that the market will reprice the interest rate sensitive assets like Vonovia accordingly. Also, if more positive news emerge from ECB, Vonovia could shoot materially higher from the current levels.

- The current P/FCF multiple is still ~2.5x below the peak level and also low from the absolute perspective (i.e., P/FCF of ~ 9.7x). Hence, Vonovia is extremely sensitive to any positive news, which is not what prudent short sellers want to see.

- Vonovia is very likely to succeed in divestitures given the constrained supply of residential buildings in Germany and other old European markets. While prices will most probably be lower, it will do the thing for Vonovia by strengthening the liquidity profile for optimal management of forthcoming debt maturities.

Why I am still bearish (via hold rating)?

Look, let me first reemphasize some facts.

Vonovia’s net debt to EBITDA stands at ~15.3x, while the most indebted residential REIT in the U.S. carries a debt to EBITDA of 12.8x with the sector average being at ~5.7x. Such differences were sustainable when the interest rates were significantly different between the FED and ECB territories. Now both the interest rates have gone up and the spreads have decreased, which implies that Vonovia’s ~ 15.3x net debt to EBITDA metric is out of whack.

Vonovia will take all the necessary measures to avoid rolling ~1.7% yielding debt forward at much higher interest rates. Hence, we will see further divestitures taking place that will in the long-run reduce Vonovia’s cash generation due to smaller portfolio size. This also means that on a go forward basis, the absolute amount of FFO generation will shrink.

As of now, Vonovia’s interest expenses would have to increase 121% to ca. €1.5bn for the ICR to fall below 1.8x (i.e., the current covenant). Given that the current average cost of debt is only 1.7%, an increase of more than 121% is not unrealistic. This year alone we saw ~25% increase in FFO interest expense, while the average cost of debt moved higher only by 20 basis points (from 1.5%). If Vonovia struggles with divestitures, the Stock could go very south.

Finally, we have to appreciate the fact that we do not know for sure whether the interest rates will actually go down over the foreseeable future. There is also a reasonable probability that the current EURIBOR levels remain this high for longer period of time, thereby rendering Vonovia’s divestitures less attractive and keeping the refinancing risk high.

Vonovia is a hold for me

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")