TERADAT SANTIVIVUT

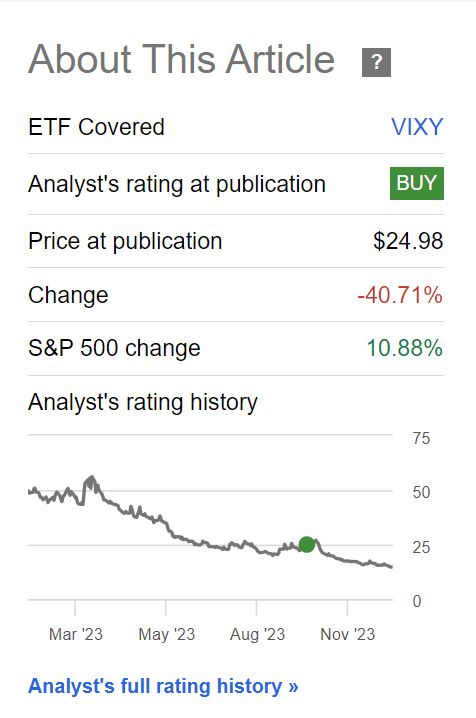

A few months ago, I reviewed the ProShares VIX Short-Term Futures ETF (BATS:VIXY), rating it a speculative buy as a short-term hedge against an escalating conflict in the Middle East.

Frustratingly, despite real-world events realizing the risks that I warned, could occur: Israel invaded Gaza in a ground offensive; Houthi rebels escalated the war into a regional conflict by attacking shipping vessels in the Red Sea; and most recently, Iranian surrogates seized an oil tanker off the coast of Oman, stock markets seemingly do not care about these tinderbox risks and have surged to near all-time highs. The VIXY ETF, in contrast, has plunged by over 40% since my article (Figure 1).

Figure 1 – VIXY had performed poorly since October (Seeking Alpha)

What happened and is VIXY still a good hedge?

Brief Fund Overview

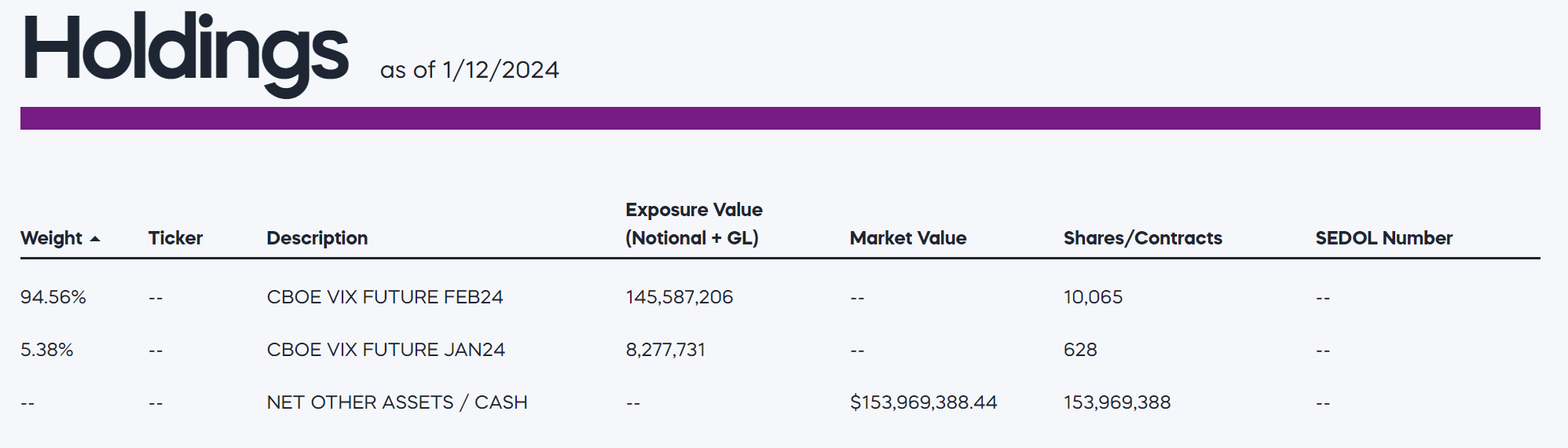

The ProShares VIX Short-Term Futures ETF provides long exposure to short-term VIX futures. The VIXY ETF owns a portfolio of front-month VIX futures with a weighted average maturity of 1 month to expiration (Figure 2).

Figure 2 – VIXY holdings (proshares.com)

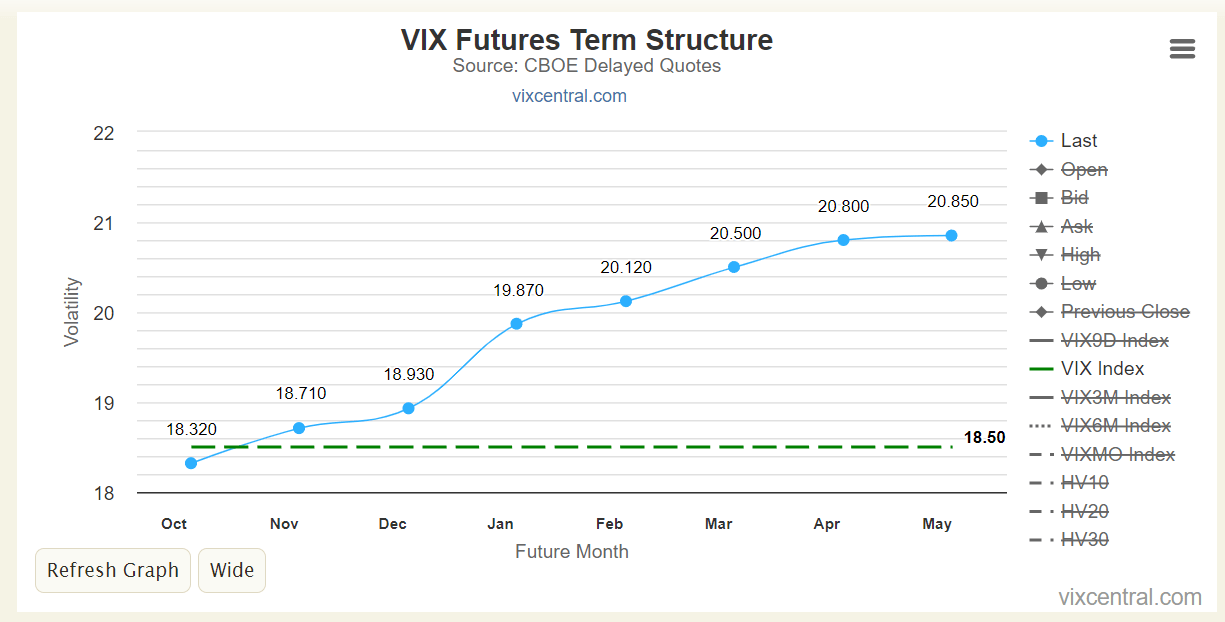

As a futures-based fund, the VIXY ETF suffers from contango decay. For example, the VIX futures curve is normally in contango where futures further out in maturity are higher in price (Figure 3).

Figure 3 – Illustrative VIX futures curve (vixcentral.com)

As time passes and VIX futures get closer to maturity, the VIXY ETF will have to sell maturing futures at a lower price and buy next month’s futures at a higher price, in order to maintain its weighted average 1-month maturity.

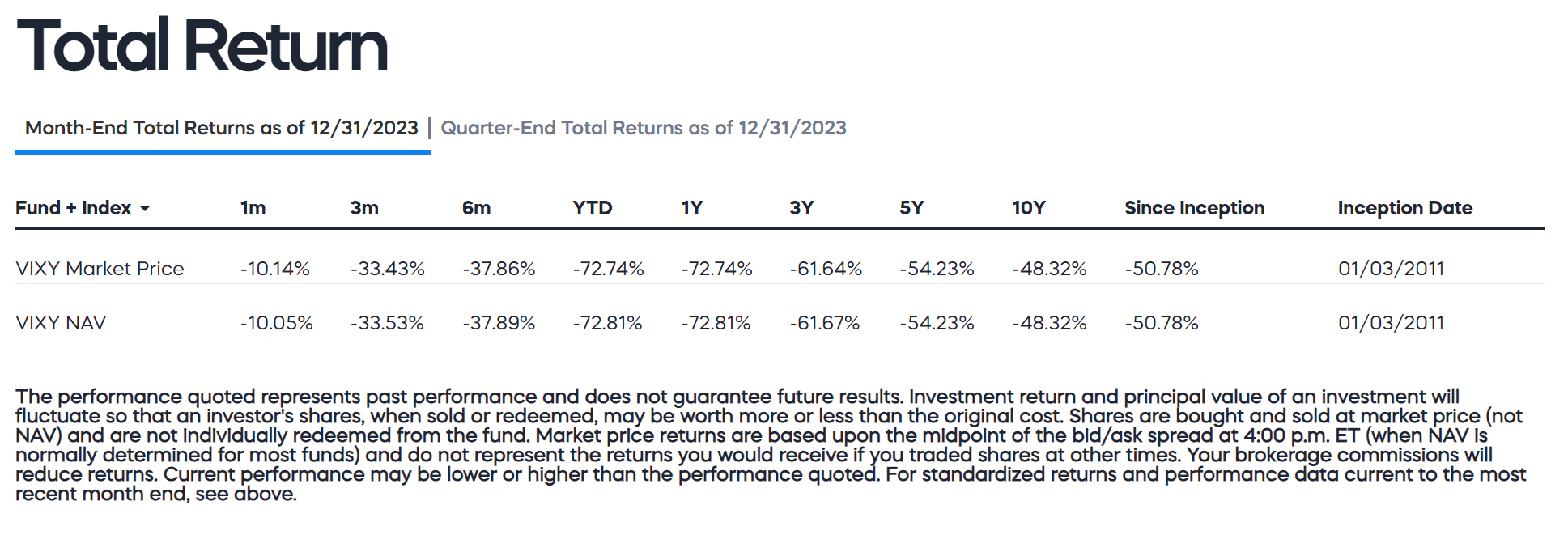

This constant rolling of positions is the main reason why the VIXY ETF has horrible long-term returns of -50.8% since inception (Figure 4). The VIXY ETF should not be held for the long term.

Figure 4 – VIXY has poor long-term returns (proshares.com)

Fed Pivot Torched Hedges

First, what happened to the markets was that in November and December, the Federal Reserve began to signal a pivot in its positioning away from ‘higher for longer’ interest rates to a ‘soft landing’, opening the door to policy rate cuts in 2024. At the time, consensus had been expecting the Fed to keep interest rates elevated for most of 2024, in order to tame inflation.

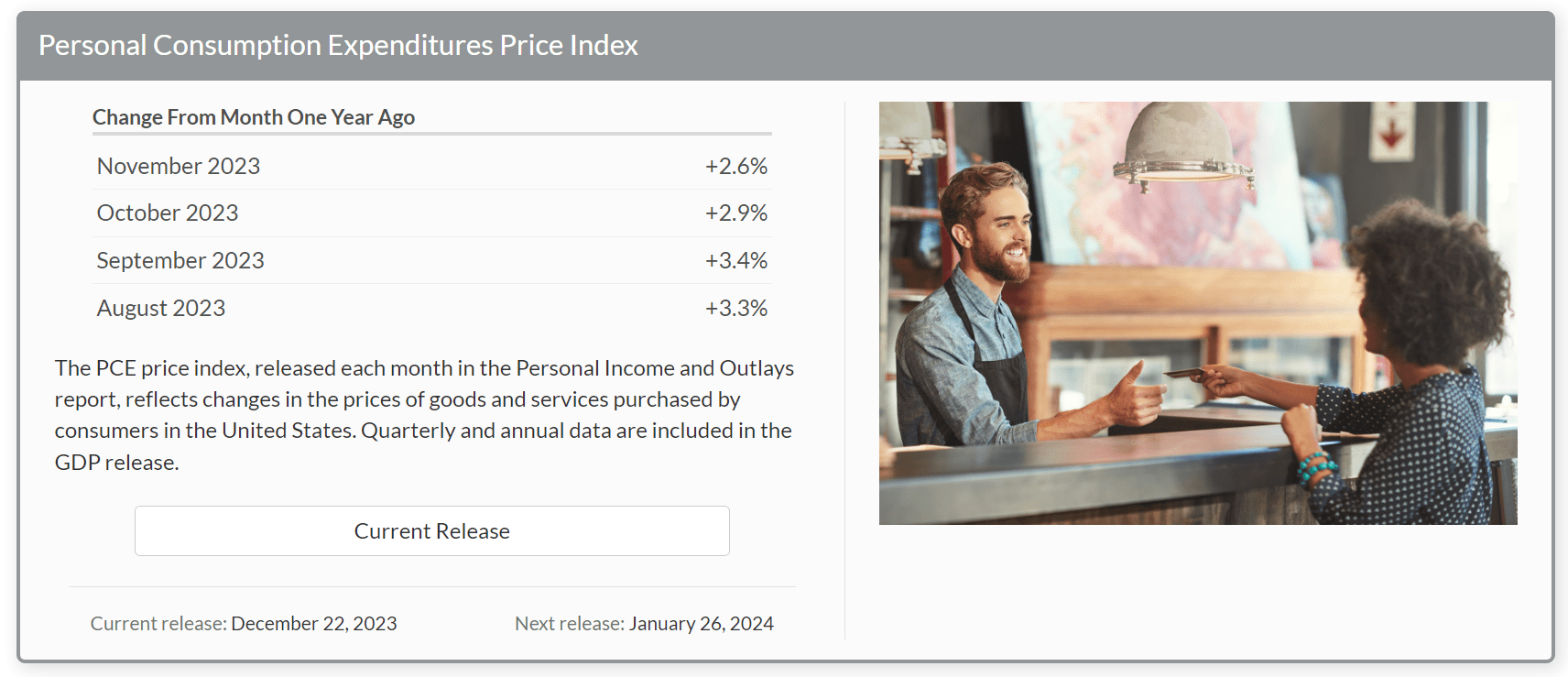

However, with the inflation battle seemingly won, the Personal Consumption Expenditures Index (“PCE”, the Fed’s preferred inflation gauge) had slowed to sub-3% in October, the Federal Reserve felt it was time to signal an end to high policy rates and potential rate cuts if inflation continues to decline (Figure 5).

Figure 5 – PCE inflation has declined to sub-3% (bea.gov)

According to Fed governor Chris Waller, the status quo was untenable because if inflation continued to decline toward 2% while policy rates were held steady, that would in effect be tightening monetary policy, since declining inflation meant that real interest rates would rise if nominal interest rates were held constant.

This shift in Fed policy stance caught many institutional investors by surprise and ignited a breathtaking squeeze in risk assets, as investors rushed to reposition their portfolios for loosening monetary policies in 2024. Investors’ massive purchase of bonds, to front run the Fed, boosted asset prices across the board and slammed the value of hedges like the VIXY ETF.

Investors Now Too Complacent

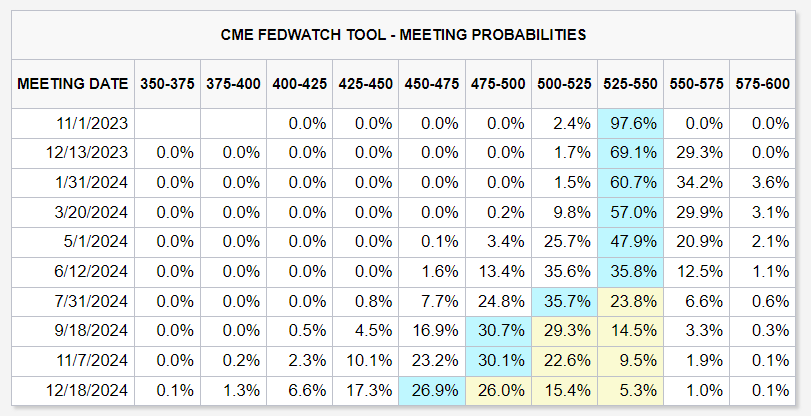

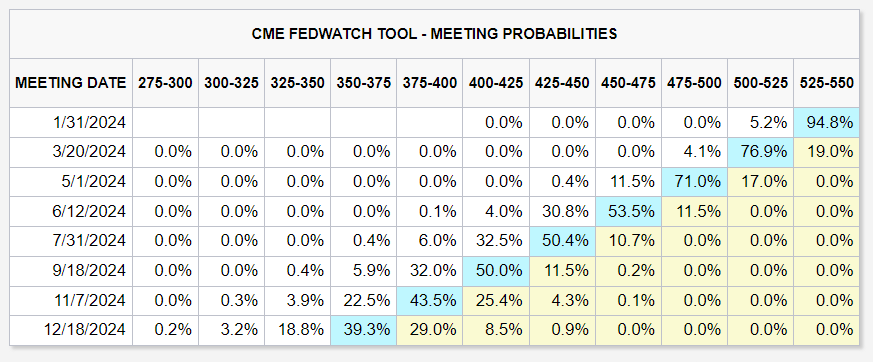

However, precisely because asset prices have screamed higher in the past 2 months, downside risks are actually far higher now. Bond investors have gone from expecting the Fed to hold policy rates steady until July 2024 (Figure 6, snapshot from October 2023) to expecting seven consecutive policy rate cuts beginning in March (Figure 7, snapshot on January 12, 2023).

Figure 6 – Fed funds future probability, October 2023 (CME) Figure 7 – Fed funds future probability, January 2024 (CME)

Simply put, the pendulum has swung too far to the dovish side, and any negative surprise may cause equities to re-rate lower.

Latest Inflation Reading Surprise To The Upside

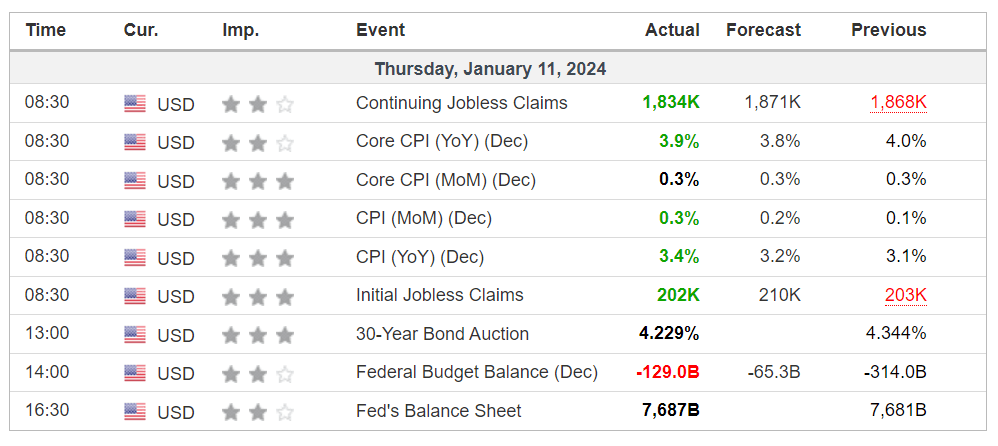

One such negative surprise occurred recently on January 11th, when the latest CPI inflation report came in at 3.4% YoY, higher than the 3.2% consensus expectations (Figure 5). Core CPI was 3.9% YoY vs. 3.8% expected.

Figure 8 – Latest CPI inflation reading came in hot (investing.com)

While this is just one inflation reading, it does suggest investors may be far too optimistic to expect the Fed to start cutting policy rates 7 consecutive times beginning at the March FOMC meeting.

Middle East Tension Could Reignite Inflation Worries

Looking farther out, worsening geopolitical tensions in the Middle East could cause inflation to reignite. For example, when recent news broke of Iran seizing the St Nicholas oil tanker off the coast of Oman, oil prices briefly rallied higher by a few percent.

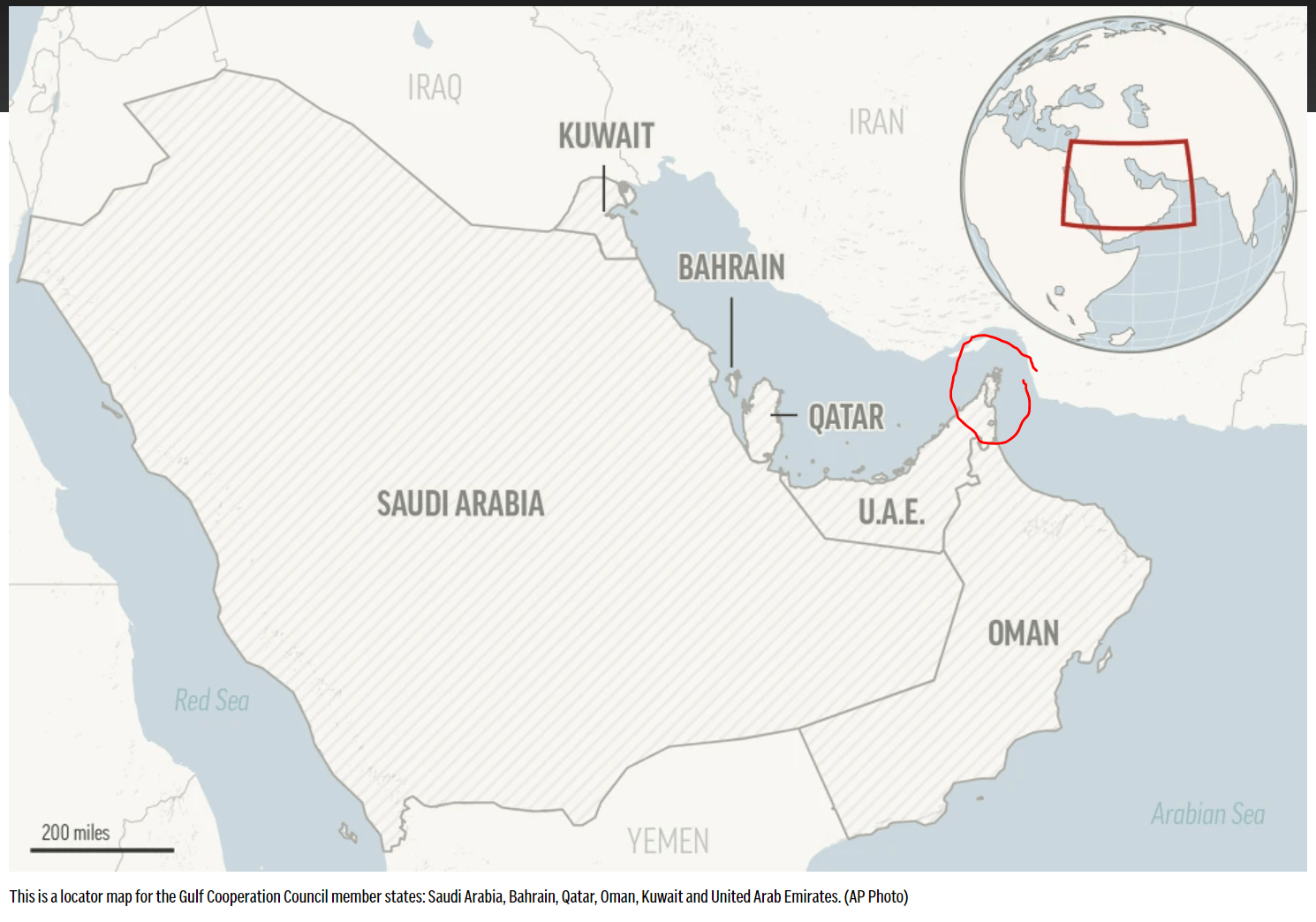

It is not hard to imagine oil prices surging higher if a major player like Iran were to officially enter the Israel/Gaza conflict. As a reminder, approximately 25% of the world’s oil transits through the Strait of Hormuz, right in the middle of the current hot zone (Figure 9).

Figure 9 – The Strait of Hormuz is an oil bottleneck (apnews.com)

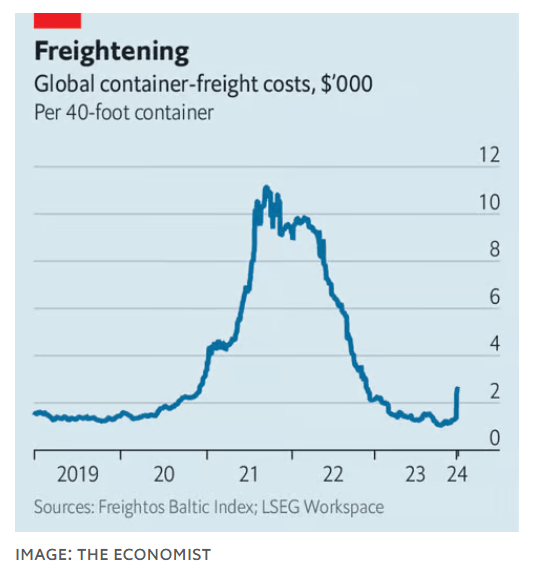

Already, Houthi attacks in the Red Sea have caused container shipping rates to surge higher, as ships must divert away from the Suez Canal and take a much longer route around South Africa to reach Europe (Figure 10).

Figure 10 – Container shipping rates have surged higher in recent days (economist.com)

Disruptions in energy supplies and goods can cause inflation to reignite higher in the coming months in the U.S. and other Western countries.

Seasonality Coming Into Play

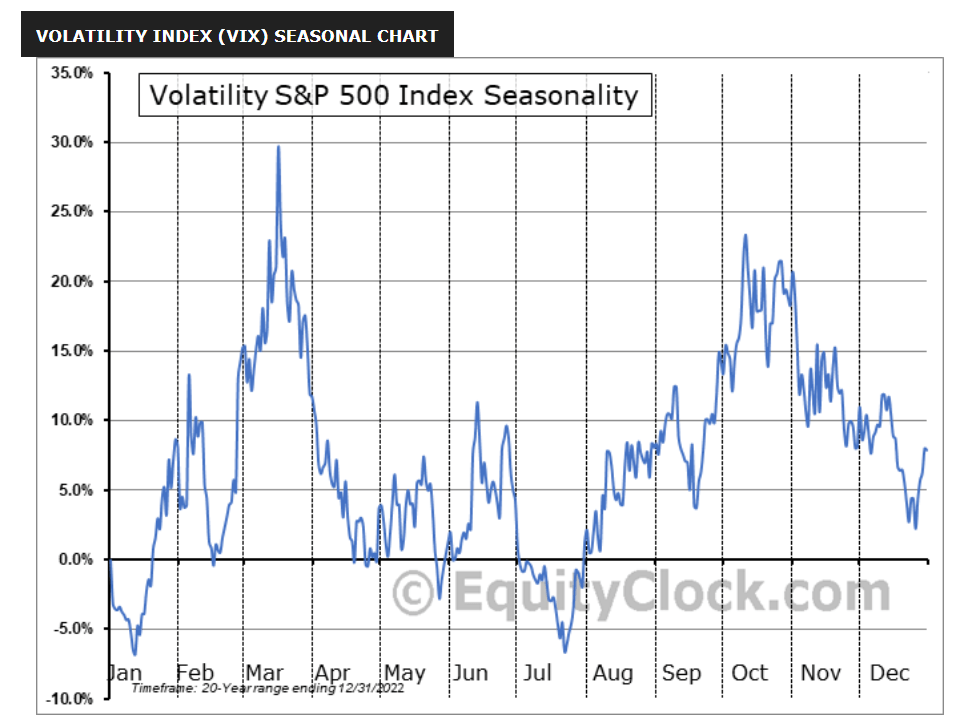

In my prior article, I warned that one of the headwinds facing the VIXY ETF was that volatility, as measured by the VIX Index, tends to have very pronounced year-end declines (Figure 11).

Figure 11 – VIX Index seasonality (equityclock.com)

By the same measure, seasonality is coming into play for the VIX Index, as volatility tends to rise into the Spring.

Conclusion

The ProShares VIX Short-Term Futures ETF provides exposure to short-term VIX futures. The VIXY ETF has not performed well in the past few months as a Fed pivot caused a massive squeeze in risk assets. However, with investor sentiment far too optimistic on the timing and pace of policy rate cuts, significant equity downside could develop if data surprises to the downside.

One potential surprise is inflation, which is showing signs of not declining as quickly as expected to the Fed’s target. The worsening geopolitical tensions in the Middle East could easily spread and cause global inflation to reignite in the coming months.

I still believe a small allocation to short-term volatility products like the VIXY ETF can help investors mitigate drawdowns in their portfolios. I continue to rate the VIXY ETF as a speculative short-term buy.

Q2 2024 Earnings Call Transcript")