Thai Liang Lim/E+ via Getty Images

As a general rule of thumb, it is foolish to expect a stock to double or more than double in a short window of time. Although fundamentals may be on your side and major decisions could be made by management, timing is often a larger role to play if you can capture that kind of return in a year or less. And usually, after a company does experience such meteoric upside, the natural move is to sell your stock and move on. But one firm that has experienced this kind of move higher that likely does warrant a little additional upside is premium egg producer Vital Farms (NASDAQ:VITL).

Back in October of 2023, I ended up upgrading the company from a ‘hold’ to a ‘buy’. Up to that point, I had been rather neutral on the business. However, I found myself impressed with its continued growth. This included not only revenue, but also profits. When I dug in deeper, I also noticed that the company remained confident in its plan to grow revenue to over $1 billion by 2027. And when I looked at what this would mean for shareholders in the long run, I could not help but to take a more bullish stance on the business than I previously had. So far, that call has proven to be a success. While the S&P 500 is up 26.1% since then, shares of Vital Farms have seen upside of 113.5%. Clearly, the easy money has been made. But I would argue that some additional upside probably exists from here. So because of that, I have decided to keep the company rated a soft ‘buy’ at this time.

The picture keeps improving

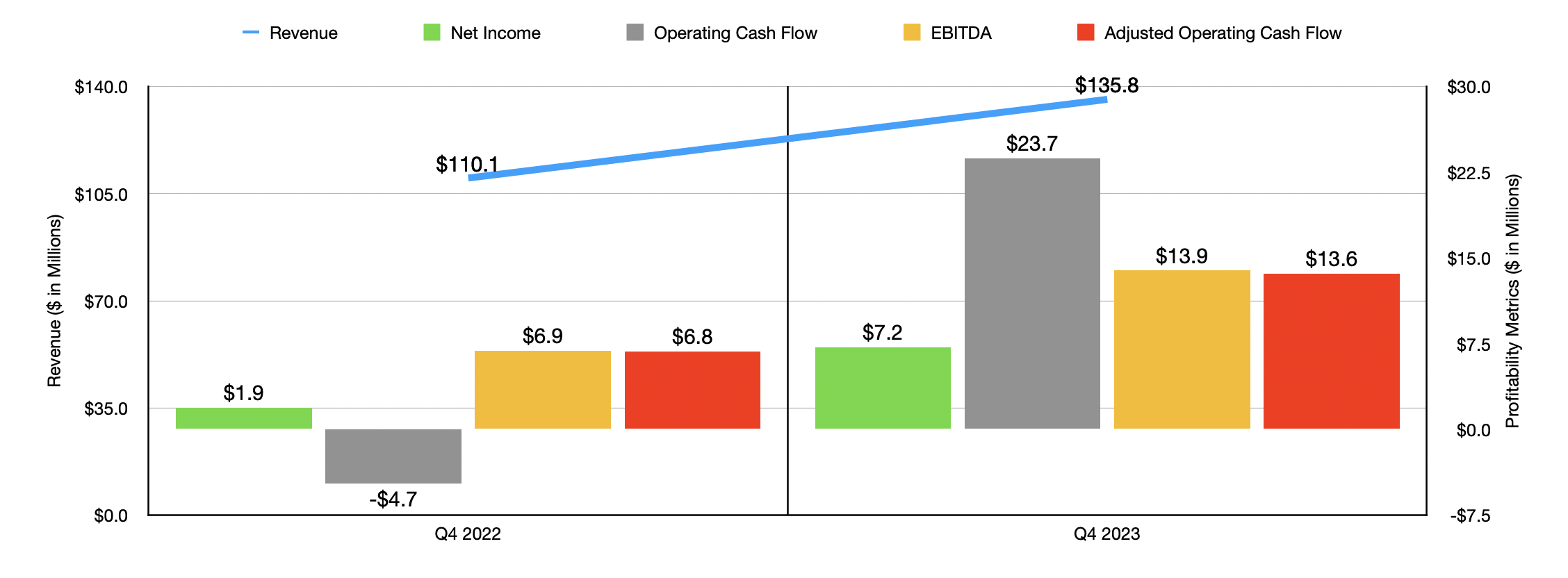

Fundamentally speaking, things are going quite well for Vital Farms and its investors. Take the final quarter of the 2023 fiscal year as an example. During that time, revenue for the business came in at $135.8 million. That’s 23.3% higher than the $110.1 million reported one year earlier. To be clear, some of this upside was driven by an extra operating week that the company had. If we strip this from the equation, revenue still would have risen by 15.7%. Higher prices played a role in this increase. But the bigger contributor was an increase in volume as the company built up its capacity further. That helped to the tune of 11.6% and reflected increased business from not only new firms, but also existing retail customers.

Author – SEC EDGAR Data

On the bottom line, Vital Farms performed really well. Net income spiked from $1.9 million to $7.2 million. And operating cash flow improved from negative $4.7 million to positive $23.7 million. If we adjust for changes in working capital, we get exactly a doubling in the metric from $6.8 million to $13.6 million. And lastly, EBITDA for the company managed to grow from $6.9 million to $13.9 million. Even though the firm suffered from higher marketing costs aimed at supporting brand development, as well as an increase in employee related expenses because of higher headcount, the firm benefited not only from the increase in revenue, but also from better profit margins when it came to cost of goods sold.

Author – SEC EDGAR Data

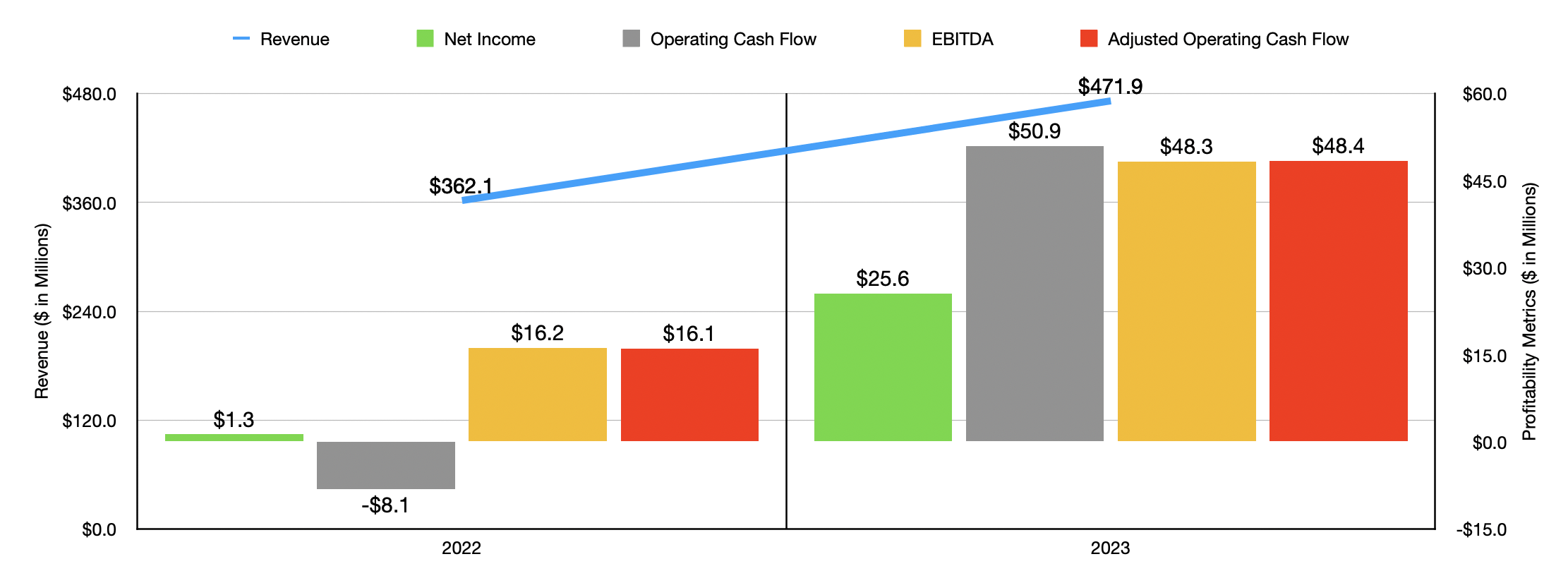

When it comes to the 2023 fiscal year and its entirety, the picture for the business was quite positive. Revenue of $471.9 million dwarfed the $362.1 million reported in 2022. Higher prices and a volume gain of 13.9% were largely responsible for this improvement. Naturally, the company’s bottom line expanded as well. As you can see in the chart above, net profits skyrocketed from $1.3 million to $25.6 million. Operating cash flow and adjusted operating cash flow both improved markedly. And EBITDA for the company expanded from $16.2 million to $48.3 million.

Vital Farms

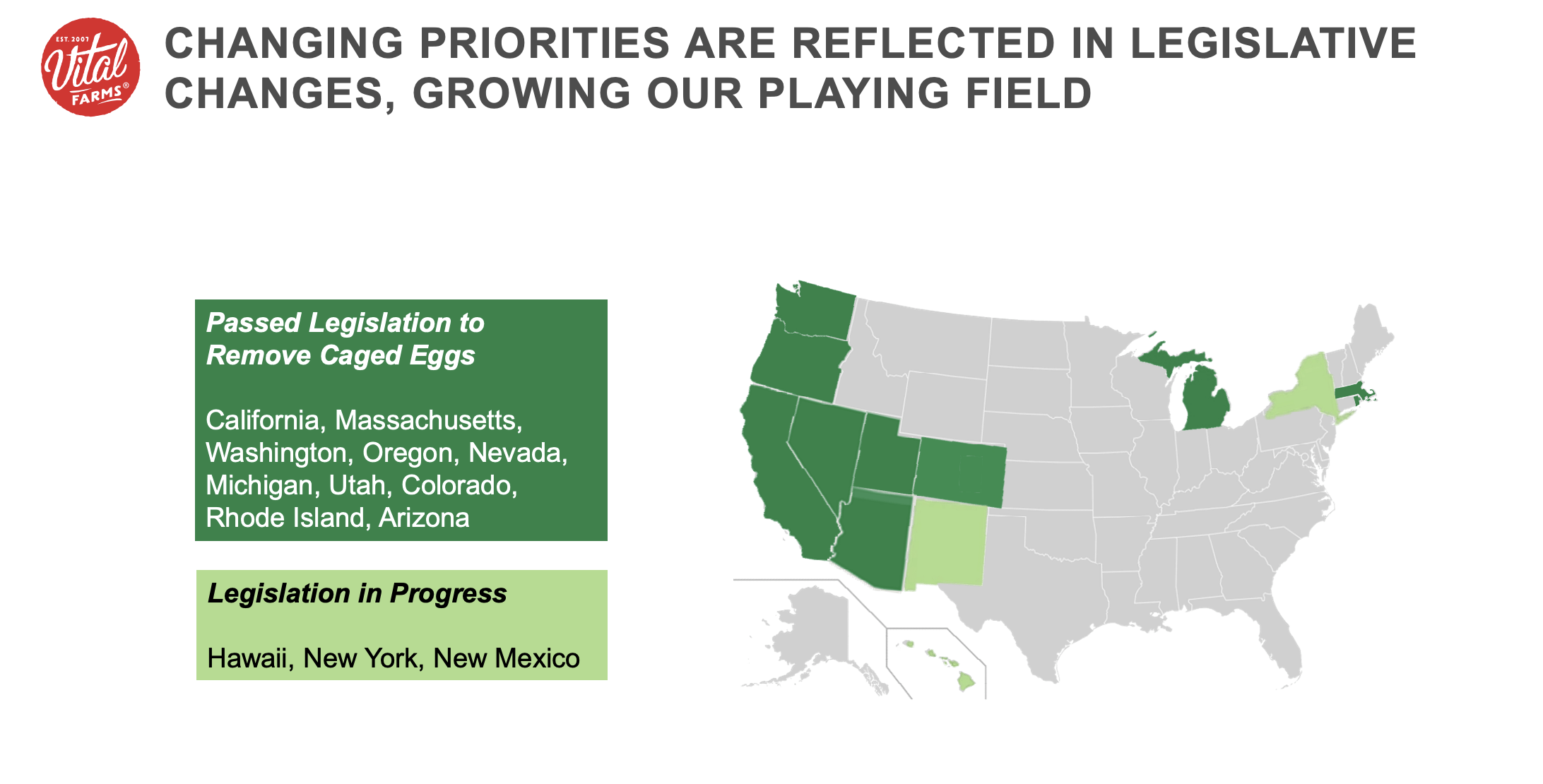

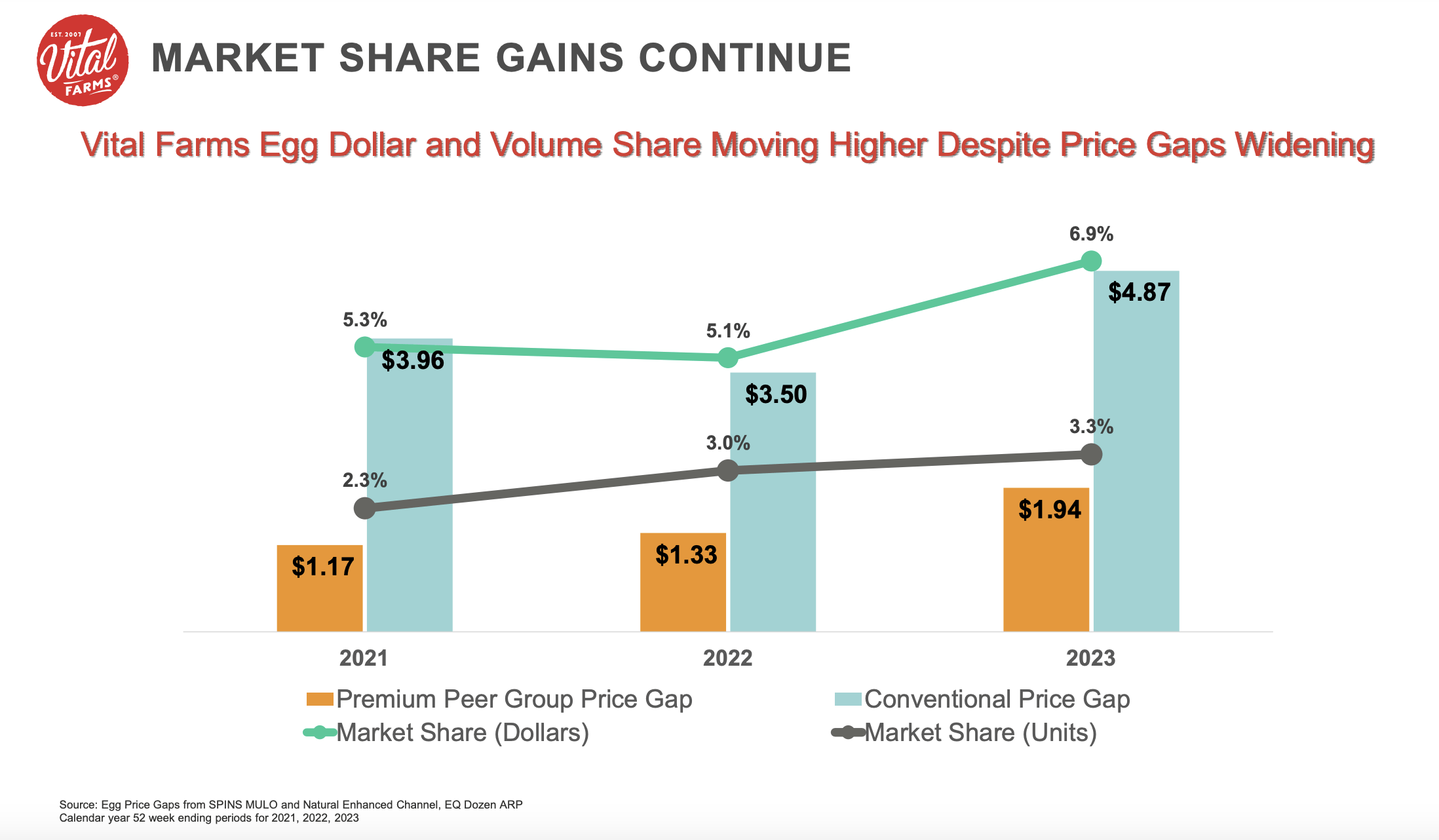

The really exciting thing for shareholders is that management expects growth for the enterprise to continue. For starters, according to management, several states, including California, Massachusetts, Oregon, and others, have all passed legislation to remove caged eggs from their markets. Other states like Hawaii, New York, and New Mexico, are considering doing the same. This will increase the demand for the cage free eggs promoted by Vital Farms. In fact, the company boasts that the average hen has an open air, 108 square foot space. In addition to becoming more popular because of regulatory changes, consumers are snatching up its eggs. When it comes to shell eggs, the company boasted a 23.7% share of wallet spend in 2023. That’s up from 18.6% back in 2020. And as you can see in the chart below, the company’s dollar and volume share in the egg space continues to improve.

Vital Farms

Management believes that continued investment, including between $35 million and $45 million on capital expenditures this year, that will help it grow capacity to the point where revenue should be $1 billion or higher by 2027. Of course, the company has to get there one step at a time. For 2024, revenue is expected to be in excess of $552 million. And EBITDA it’s forecasted to be above $57 million. If the company can hit its targets for 2027, then EBITDA would climb to around $130 million. That brings with it nearly 300 basis points in margin expansion that will be driven by price increases and, for the most part, increased volume.

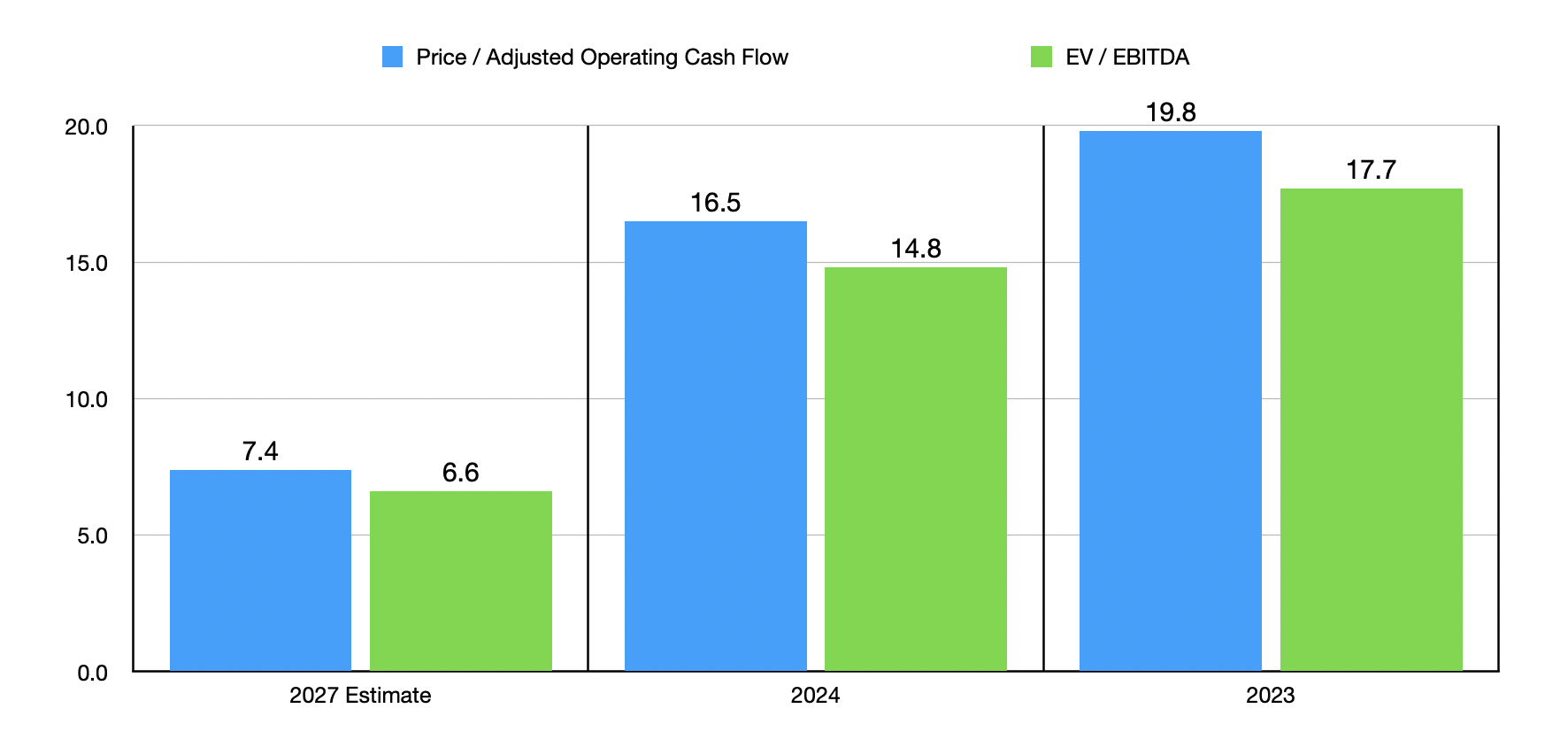

Author – SEC EDGAR Data

Normally, I am skeptical about guidance, particularly when we are talking multiple years into the future. But management has remained confident in this target for some time. Furthermore, the company’s growth has been quite impressive as of late. Using the estimates provided by management, I was able to value the company as shown in the chart above. It shows historical results for 2023, as well as projected results for both 2024 and 2027. Using even the 2024 estimates, I would say that the stock is more or less fairly valued. It might not even be that far off from being overvalued. But when you project out to 2027, shares seem to have some rather meaningful upside. For instance, if we use the price to adjusted operating cash flow multiple for the business and assume that, once it hits its target in 2027, an appropriate value for the business would be a multiple of 12, that would imply upside of around 13% per annum between now and then. That’s a bit better than the roughly 11% or so that the S&P 500 averages over time. I then compared the company to five similar firms as shown in the table below. On a price to operating cash flow basis, even using the 2023 figures, three of the five companies ended up being cheaper than it. This number does rise to four of the five when using the EV to EBITDA approach.

| Company | Price / Operating Cash Flow | EV / EBITDA |

| Vital Farms | 19.8 | 17.7 |

| SunOpta (STKL) | 51.6 | 25.3 |

| The Hain Celestial Group (HAIN) | 6.9 | 16.1 |

| B&G Foods (BGS) | 3.4 | 16.7 |

| Mission Produce (AVO) | 20.8 | 15.1 |

| Adecoagro (AGRO) | 2.4 | 3.0 |

Takeaway

Fundamentally speaking, Vital Farms is doing really well for itself. The company continues to demonstrate attractive growth, and I would say that it will probably achieve its target by 2027. Of course, anything can change. But so far, you can count me as one of those that are impressed. The easy money has been made and, relative to similar firms, shares are looking rather pricey. But when we factor in future growth, upside seems to be appealing enough to warrant a bit more optimism. If shares rise another 10% to 20%, I would probably consider it a good candidate for a modest downgrade. But as things stand, a soft ‘buy’ rating is still logical.

Q2 2024 Earnings Call Transcript")