chengwaidefeng

Vista Energy, S.A.B de C.V. (NYSE:VIST) looks promising in 2024 as the company has an attractive low valuation with strong double-digit revenue and earnings growth according to consensus estimates. The stable expected price of crude oil in 2024 and 2025 should help the company maintain its high profitability metrics.

Company Background

Vista Energy is a $3.76 billion market cap oil and gas producer based in Mexico. VIST’s main assets are based in Vaca Muerta in the Neuquina basin which is located in Argentina. The company also has assets in Mexico in the Macuspana basin. Vista has total proven and probable reserves of 318.5 MMboe.

The Vaca Muerta is what the company considers its key value driver. The reason for that is because Vista has 1,150 locations under development in Vaca Muerta, which includes 99 wells that are already drilled. The company had 308.4 MMboe of proved reserves in Vaca Muerta as of the end of 2023. The productivity of the wells in Vaca Muerta are considered the best in the basin.

Vista has proved reserves of 10.1 MMboe in the Macuspana basin in Mexico. The company believes that future upside in this basin will come from infrastructure upgrades, field developments, and exploration of untested deeper formations.

Growth Catalysts

Vista Energy has a number of positive catalysts that can drive growth in 2024 and beyond. On a macro level, the price of oil is expected to remain stable according to projections from Eia.gov. The EIA projects that the price of Brent crude oil will average about $82 per barrel in 2024 and $79 in 2025. For context, the price of Brent crude averaged about $82 in 2023. WTI crude is expected to remain a few dollars per barrel below Brent crude. So, what was good for Vista in 2023 in terms of oil prices should carry over into 2024.

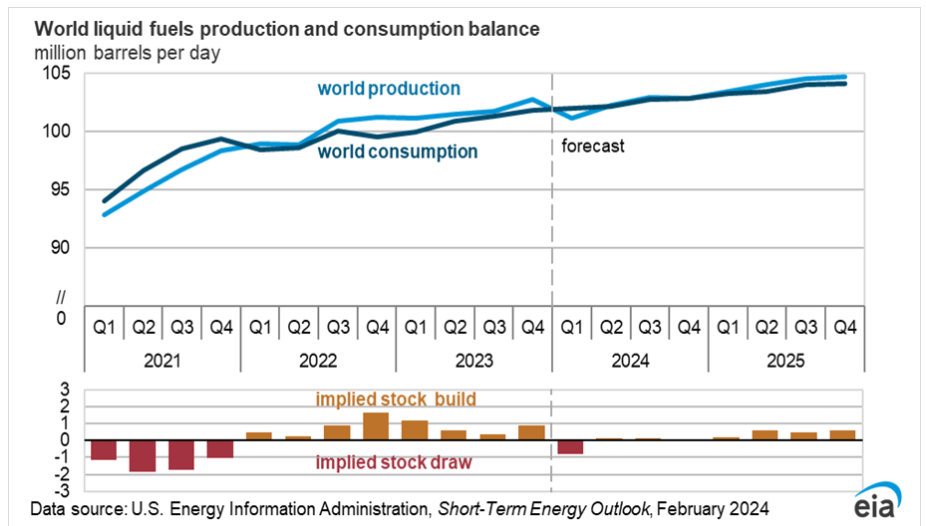

The steady expected price of crude oil is attributed to a balance in the supply and demand of crude oil. Oil production is expected to approximately match the demand (consumption) during the forecast period as illustrated in the chart below.

EIA.gov

If the price of oil does remain steady in 2024, it would allow Vista Energy to maintain its strong profitability metrics. VIST achieved high double-digit margins and returns over the trailing 12 month period. VIST has a gross margin [GM] of 74%, an EBITDA margin of 80%, an ROIC of 24%, ROE of 38%, and an ROA of 15%.

For context, I’ll provide metrics from Vista’s competitors. Northern Oil and Gas (NOG) has a GM of 80%, EBITDA margin of 93%, ROIC of 23%, ROE of 66%, and an ROA of 21%. Enerplus Corporation (ERF) has a GM of 65%, EBIDTA margin of 63%, ROIC of 26%, ROE of 40%, and an ROA of 22%. It is important to note that Enerplus is being acquired by Chord Energy (CHRD). The acquisition should improve Chord’s profitability as Enerplus has higher margins and returns. Chord Energy has a GM of 56%, an EBITDA margin of 54%, ROIC of 16%, ROE of 21%, and an ROA of 15%.

All three companies are solid performers in the industry. They are all benefitting from the stable price of oil as they drive production higher by increasing drilling capacity and utilization. Vista Energy expects to increase production from 68,000 boes per day to 70,000 boes per day in 2024. Vista expects this to result in an EBITDA increase of $1 billion to $1.5 billion based on an oil price of $65 to $70 per barrel. Vista aims to double production to 100,000 boes per day by 2026. This gives Vista a positive long-term outlook as the price of oil is expected to remain stable.

Northern Oil and Gas is guiding to produce 115,000 to 120,000 boe per day in 2024 over the 114,000 boe per day that the company produced in Q4 2023. Northern also has an acquisition strategy that it uses for ongoing growth in addition to its organic growth from existing assets.

Enerplus expects total production in 2024 to average 99,000 boe per day which would be lower than the 100,015 average boe per day that was achieved in 2023. Of course this estimate could change based on the completion of the Chord Energy merger which is expected to be completed in mid-2024.

Chord Energy believes that the combined company would have the best inventory in the Bakken. Chord also expects to benefit from significant synergies from the acquisition. These capital, administrative, and operating synergies are expected to amount to $150 million per year. The total value of the synergies is expected to exceed $750 million.

Vista and its competitors are all likely to perform well in 2024 in my opinion. The stable price of oil and the efforts from these companies to increase production should help drive revenue and earnings growth this year.

What I like about Vista is the strong expected revenue growth of 49% and earnings growth of 51% for 2024 according to consensus estimates. NOG is expected to grow revenue at less than 1% and earnings are expected to decline by 24% in 2024. Enerplus is expected to experience a 2% decline in revenue, but grow earnings at a strong pace of 51%. Chord Energy is expected to grow revenue at 1.5% and earnings at 7.5%. Of course, the merger between Chord and Enerplus could alter these expectations. Overall, Vista has the highest combination of revenue and earnings growth expectations, which makes the stock stand above the others. This could be a strong catalyst for the stock if these expectations are met or exceeded.

Valuation

I am using the forward EV/EBITDA ratio to compare Vista with its competitors since it is the standard valuation metric for oil & gas companies. The EV/EBITDA ratio values companies based on their earnings before interest, taxes, depreciation, and amortization while eliminating debt. The EV/EBITDA ratio is important to value oil companies since they tend to run with a lot of debt and the EV includes the cost of paying it off.

I am also using the EV/2P ratio which values companies based on their total proven and probable reserves. The importance of the EV/2P ratio is to determine how companies are valued in relation to their potential growth since the reserves are likely to be recovered over time. Here’s how the companies compare:

| VIST | NOG | ERF | CHRD | |

| Forward EV/EBITDA | 3.6 | 3.7 | 4.2 | 3.12 |

| EV/2P | 1.27 | 1.35 | 2.9 | 0.82 |

source: Seeking Alpha & SEC filings

The calculations for EV/2P were as follows:

Vista: EV of $4.22 billion/2P of $3.3 billion; NOG: EV of $5.61 billion/2P of $4.156 billion; ERF: EV of $3.85 billion/2P of $1.321; CHRD: EV of $7.02 billion/$8.53

The 2P values were taken from each company’s SEC filings as of the end of 2023. The values were calculated based on U.S. SEC standards.

According to these metrics, Chord Energy has the most attractive valuation. Vista comes in 2nd place with its valuation relatively close to Chord’s. Frankly, all four companies are valued attractively with EV/EBITDA ratios below 5 and EV/2P ratios below 3. Typically EV/EBITDA ratios below 10 are considered healthy for oil and gas companies. For context, the global EV/EBITDA ratio for the energy sector was 12.5 in 2023. I couldn’t find a sector or industry average for the EV/2P ratio. However, we can see that VIST’s EV/2P ratio is attractive among its competitors.

Technical Perspective

Vista Energy (VIST) Weekly Chart with RSI (Tradingview)

Vista’s stock had strong positive momentum over the past three years. The stock has been bouncing in and out of an overbought area on the weekly chart during the past few years. The stock recently re-entered an overbought level. So, investors may want to wait for a pullback before jumping in. The stock does tend to have pullbacks of 10% to 40% while rising in a long-term upward trend. The stock’s attractive valuation and strong growth could keep the stock in this positive upward trajectory.

Vista Energy’s Long-Term Outlook

Vista’s total proven & probable reserves of 318.5 MMboe can last for over a decade (about 12.5 years) if the company produces 70,000 barrels per day or 25.55 million barrels per year. Of course, the company’s reserves can grow over time through continued exploration and through acquisitions.

The company’s low valuation leaves room for the stock to grow. Vista’s strong double-digit revenue and earnings growth should drive the stock higher as the company boosts production. Stable oil prices are likely to help Vista achieve its revenue and earnings expectations.

The biggest risk for Vista would be an unexpected significant drop in oil prices which could negatively impact revenue and earnings. Another risk would be a recession which could decrease demand for Vista’s oil and gas. Potential investors should also be aware that the stock can have sharp frequent pullbacks. So, they may need some tolerance for high stock volatility.

If conditions remain favorable for Vista (stable oil prices & a strong economy) then the stock has a good chance of outperforming the broader market. Above average stock gains are likely due to Vista’s above-average growth and the low valuation.

Q2 2024 Earnings Call Transcript")